Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:6857

Advantest (TSE:6857) Margin Surge Reinforces Bull Case, But Valuation Premium Faces Scrutiny

Simply Wall St

Reviewed by Simply Wall St

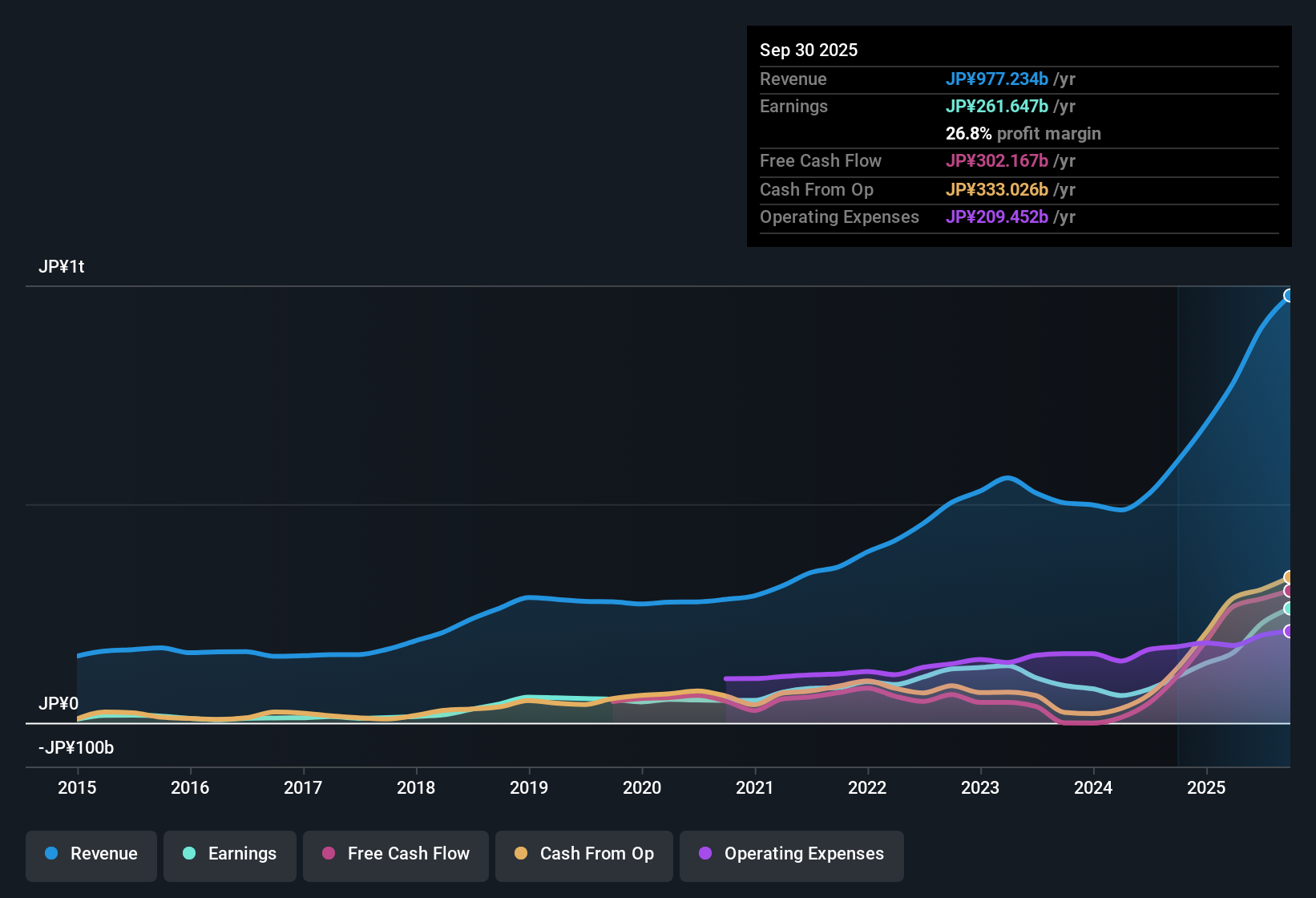

Advantest (TSE:6857) reported net profit margins of 26.8%, up from last year’s 17.7%, driven by significant profit growth. EPS surged 147.5% this year, topping the already-strong five-year annual earnings growth rate of 21.9%. Revenue and earnings are forecast to outpace the Japanese market, giving investors plenty to consider as the company sustains its momentum with high-quality margins and robust growth projections.

See our full analysis for Advantest.Next up, let’s see how these headline results stack against the market’s ongoing narratives and community views. Some talking points will be affirmed, while others may face new scrutiny.

See what the community is saying about Advantest

AI Demand Powers Revenue Outlook

- Revenue is forecast to grow 6% per year, outpacing Japan's broader market forecast of 4.5% annual growth and reflecting persistent strength in end-market demand for advanced chip testing solutions.

- Consensus narrative notes that surging AI applications and the complexity of next-generation semiconductors are fueling sustained, above-industry sales growth for Advantest.

- Double-digit market growth for advanced SoC and memory testers through FY2026 is expected to directly support Advantest's revenue momentum, as highlighted in consensus projections.

- Advantest's move into adjacent areas like system-level testing and device interfaces is seen as a strategy to diversify revenue streams and strengthen long-term profitability.

- Consensus narrative underscores how these latest numbers reinforce analysts’ positive long-term view. See how this trend shapes the rest of the company story in the consensus community take. 📊 Read the full Advantest Consensus Narrative.

Capacity Expansion Lifts Margins

- Operating margin improvements are tied to a planned 60 to 70% boost in production capacity by the end of 2026 compared to 2025, enabling increased operating leverage if AI-driven demand persists.

- Consensus narrative highlights disciplined cost management and automation as key factors behind record operating margins, while warning that margin gains may prove difficult to maintain if any one-off benefits fade.

- Advantest’s recent record Q1 was boosted by favorable product mix and the absence of one-off losses, which may not repeat, raising some caution on margin stability.

- Still, ongoing investments in automation and higher-margin products are expected to build in more resilience for future margin trends.

Valuation Premium Drives Debate

- Advantest’s price-to-earnings ratio stands at 61.5x, far higher than the Japanese semiconductor industry average of 18.6x and peer average of 28.9x, and well above the DCF fair value of ¥6,873.80, raising questions about how much future growth is already priced in.

- Consensus narrative points to the share price premium as both recognition of strong recent growth and a reason for caution, since high multiples could expose the stock to volatility if growth expectations are not met.

- Recent analyst consensus price target is ¥14,609.47, while the current share price is even higher at ¥22,120.00, suggesting some market exuberance compared to analysts' baseline.

- Bears highlight that while Advantest’s underlying earnings momentum remains strong, persistent price instability over the past three months means investors may face increased volatility at current levels.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Advantest on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a unique take on the data? In just a few minutes, you can shape your own narrative and share a fresh perspective: Do it your way

A great starting point for your Advantest research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Despite Advantest’s impressive growth, the stock trades at a hefty premium. This exposes investors to potential downside if lofty expectations are not met.

For those who want better value and less volatility risk, check out these 855 undervalued stocks based on cash flows to discover companies priced more attractively based on their cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6857

Advantest

Manufactures and sells semiconductors, component test systems, and mechatronics-related products in Japan, rest of Asia, the Americas, and Europe.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor