Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:6857

Advantest (TSE:6857) Announces Share Buyback and Dividend Increase to Enhance Shareholder Value

Simply Wall St

Reviewed by Simply Wall St

Advantest (TSE:6857) is making headlines with its recent announcement of a share buyback program, aiming to repurchase up to 9 million shares to enhance shareholder returns and capital efficiency. This move aligns with the company's growth prospects, underscored by a projected 18% annual earnings increase and a strong return on equity forecast. However, challenges such as a high P/E ratio and cost management issues could impact profitability, making it crucial for Advantest to navigate these hurdles while leveraging opportunities in the semiconductor industry.

Navigate through the intricacies of Advantest with our comprehensive report here.

Competitive Advantages That Elevate Advantest

With earnings projected to grow at 18% annually, Advantest is outpacing the broader Japanese market. This growth trajectory is supported by a return on equity forecasted at 28.3% in three years, underscoring the company's financial health. The recent announcement of a share buyback program, repurchasing up to 9 million shares, reflects a commitment to shareholder returns and capital efficiency. This strategic move complements their improved profit margins, now at 17.7%, and a strong cash position that exceeds total debt. The leadership's focus on R&D, as highlighted by CEO Douglas Lefever, ensures that Advantest remains at the forefront of innovation, driving both market share and customer loyalty.

Challenges Constraining Advantest's Potential

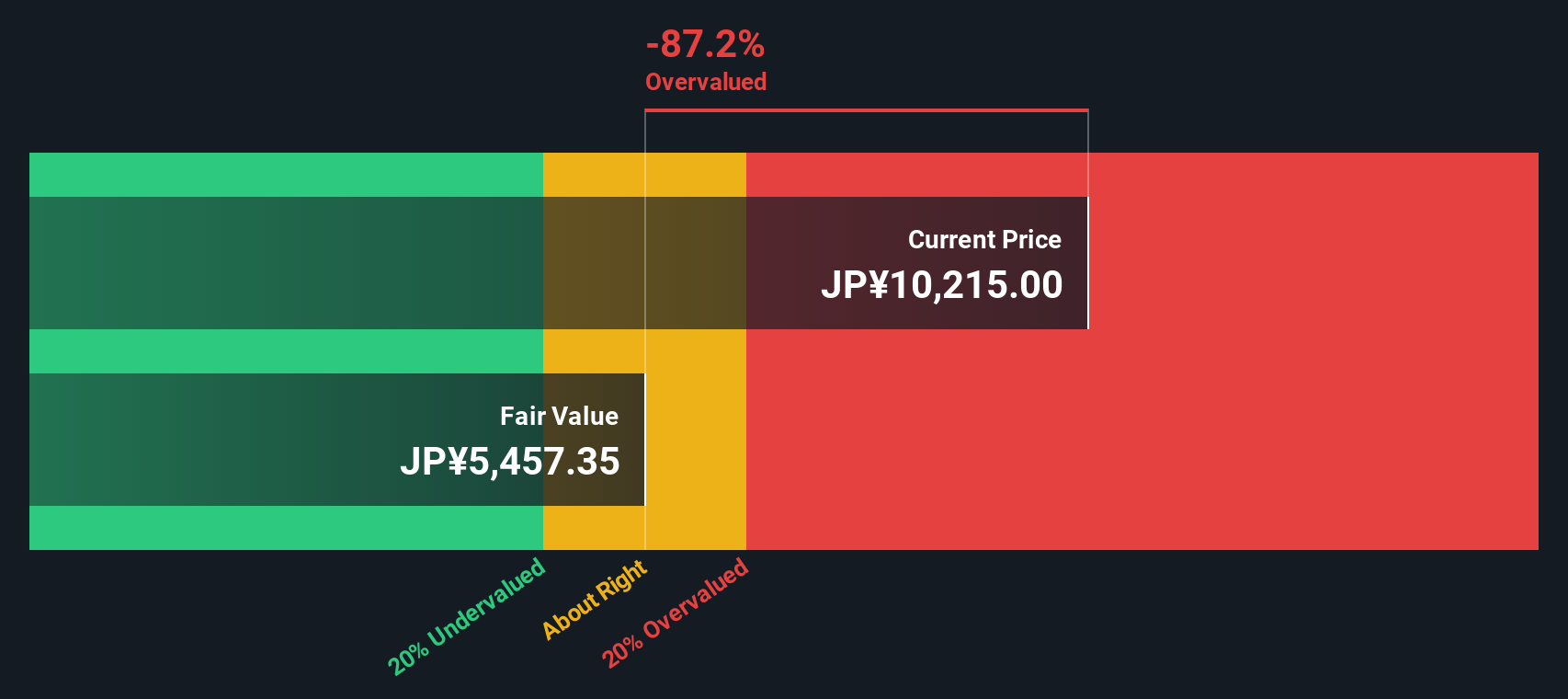

However, Advantest's valuation presents a challenge, with a P/E ratio of 62.2x, significantly higher than industry averages. This high valuation could deter potential investors despite the company's strong performance. Additionally, the slower-than-expected growth in certain segments, as acknowledged by the management, necessitates a reassessment of growth targets. Cost management remains a concern, with CFO Shuhei Nakamura noting its impact on margins. These financial challenges could potentially erode profitability if not addressed effectively.

Potential Strategies for Leveraging Growth and Competitive Advantage

In light of these challenges, Advantest has opportunities to capitalize on the growing demand in the semiconductor industry. The company's strategic alliances and product innovations, highlighted during the SEMICON Taiwan 2024 presentation, position it to expand its market share. The board's decision to increase interim dividends to JPY 19.00 per share further signals confidence in sustained growth. These initiatives could enhance Advantest's competitive positioning and leverage emerging market opportunities.

External Factors Threatening Advantest

Nonetheless, Advantest faces external pressures, including economic headwinds and competitive forces. The volatile share price over recent months might deter investors, while increased competition requires agility and innovation to maintain market leadership. Supply chain disruptions remain a concern, as noted by the management, potentially impacting production and delivery. Addressing these threats is crucial for sustaining Advantest's growth trajectory.

Conclusion

Advantest's impressive growth trajectory, supported by strong financial health and strategic initiatives like share buybacks and increased dividends, positions it well in the competitive semiconductor industry. However, the company's high Price-To-Earnings Ratio of 62.2x, compared to industry and peer averages, suggests that its stock may be perceived as expensive, potentially deterring new investors despite its solid performance. To sustain its growth and competitive advantage, Advantest must address internal challenges such as cost management and slower growth in certain segments while navigating external pressures like economic headwinds and supply chain disruptions. By leveraging its innovative R&D efforts and strategic alliances, Advantest can enhance its market share and capitalize on emerging opportunities, ensuring continued shareholder value despite current valuation concerns.

Make It Happen

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSE:6857

Advantest

Manufactures and sells semiconductors, component test system products, and mechatronics related products in Japan, the Americas, Europe, and Asia.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.2% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.5% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.8% undervalued

AG

Community Contributor