Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:4369

Tri Chemical Labs (TSE:4369) Net Margin Climbs to 24.2%, Supporting Bullish Value Narrative

Simply Wall St

Reviewed by Simply Wall St

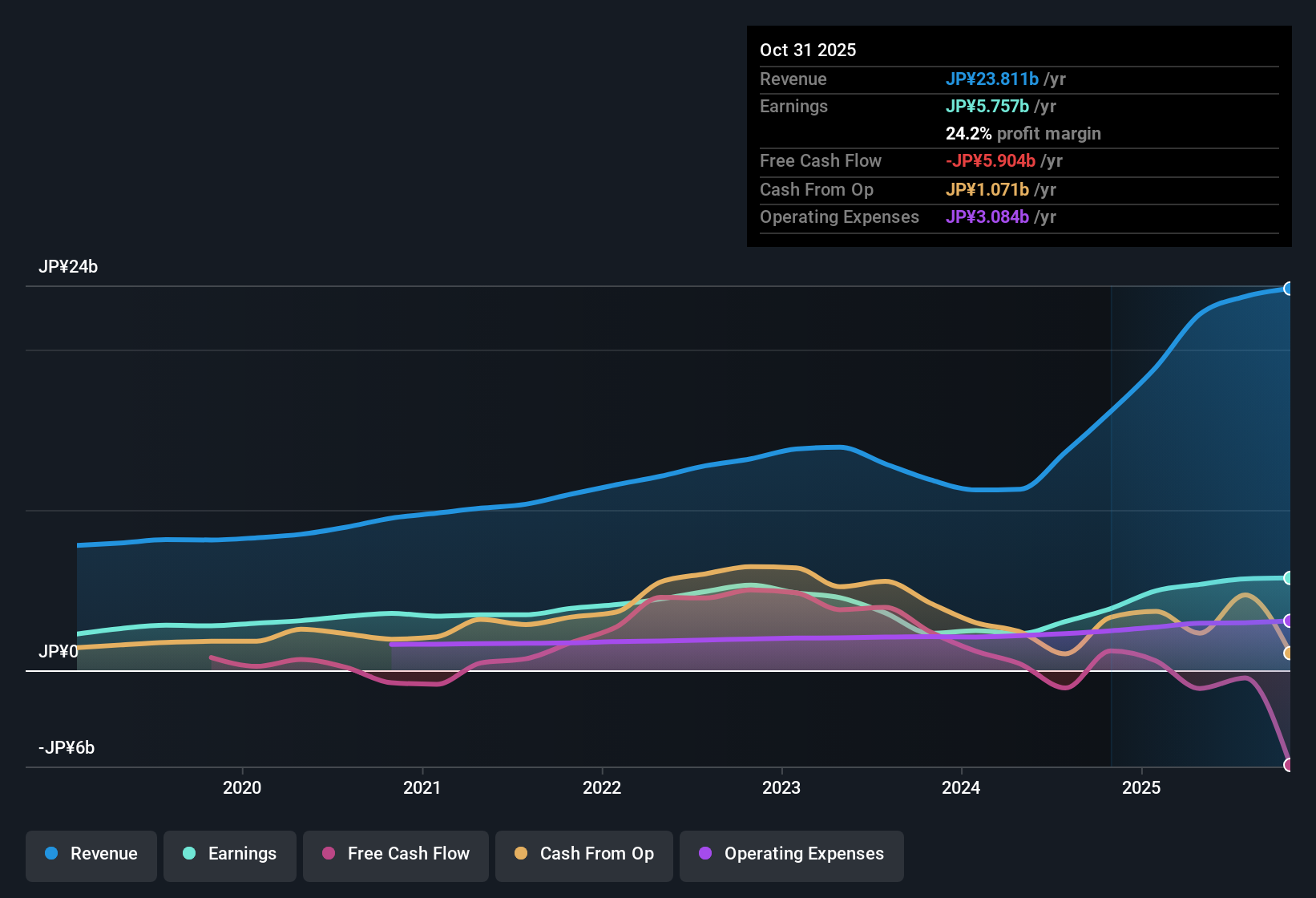

Tri Chemical Laboratories (TSE:4369) just posted Q3 2026 results with revenue of ¥5.6 billion and basic EPS of ¥38.30. Over the last year, the company has seen revenue climb from ¥13.6 billion to ¥23.8 billion and EPS rise from ¥93.79 to ¥177.16. Margins stayed robust throughout, reflecting the company’s ability to maintain profitability as sales expanded.

See our full analysis for Tri Chemical Laboratories.Now, let’s weigh these latest results against the broader market narratives. Some established views may be confirmed, while others could be up for debate.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margins Edge Higher

- Net profit margin for the trailing twelve months reached 24.2%, nudging up from 23.8% a year earlier, underlining steady profitability improvements as the top line expanded.

- Analyst expectations have called out strong margin durability, noting that robust net income of ¥5.8 billion ($5.8 billion) over the last year supports the view that Tri Chemical Laboratories is managing growth without sacrificing bottom-line health.

- Consensus narrative points to ongoing earnings outperformance, as annual profit growth (49.6%) tracks above the company’s five-year trend (5.1%) and the Japanese market average (8.3%).

- Even as revenue rose to ¥23.8 billion ($23.8 billion), margin stability provides confidence for those watching for sustained operating strength.

Share Price Trades Deep Below Intrinsic Value

- At ¥2,792.00, shares currently sit about 71% below DCF fair value estimates (¥9,726.57), and roughly 42% below the consensus analyst price target (¥3,968.00).

- The prevailing market view highlights that this valuation discount, paired with a price-to-earnings ratio of 15.8x versus the semiconductor sector average of 20.4x, frames the stock as an attractive relative value.

- Current price levels reflect a notable disconnect, giving value-focused investors plenty of justification for a closer look compared to peers.

- Discount to intrinsic value is further bolstered by sector demand drivers, with 13.2% forecast annual revenue growth against a market average of 4.5%.

Revenue Growth Surges Past Market Pace

- Total revenue grew from ¥13.6 billion ($13.6 billion) to ¥23.8 billion ($23.8 billion) year over year, representing a significant lead on the broader Japanese market’s growth expectations of 4.5%.

- Building on this, the general market perspective suggests that Tri Chemical Laboratories’ focused exposure to the semiconductor supply chain and diversification across key Asian markets contributes directly to this growth strength.

- The company’s projected earnings expansion of 13.1% a year is supported by sector-wide tailwinds, including ongoing investment in advanced manufacturing nodes and diversified regional customer bases.

- High revenue visibility from specialty product offerings is seen as a differentiator, mitigating some of the risks common to semiconductor suppliers.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Tri Chemical Laboratories's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Although Tri Chemical Laboratories is delivering standout revenue growth, the stock’s deep discount suggests ongoing market skepticism about the reliability or duration of this outperformance.

If stability and predictable financial performance matter most to you, now is the time to use our stable growth stocks screener (2075 results) to quickly discover companies with proven track records of steadily growing earnings and sales.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tri Chemical Laboratories might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4369

Tri Chemical Laboratories

Develops, manufactures, and sells high-purity chemicals for semiconductor manufacturing in Japan, Taiwan, China, South Korea, and internationally.It offers semiconductors, coating, optical, fiber, compound semiconductor, and reagents.

Very undervalued with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative