Tosei Reit (TSE:3451) Cash-Flow-Strained 5.16% Yield Reinforces Cautious Income Narrative

Reviewed by Simply Wall St

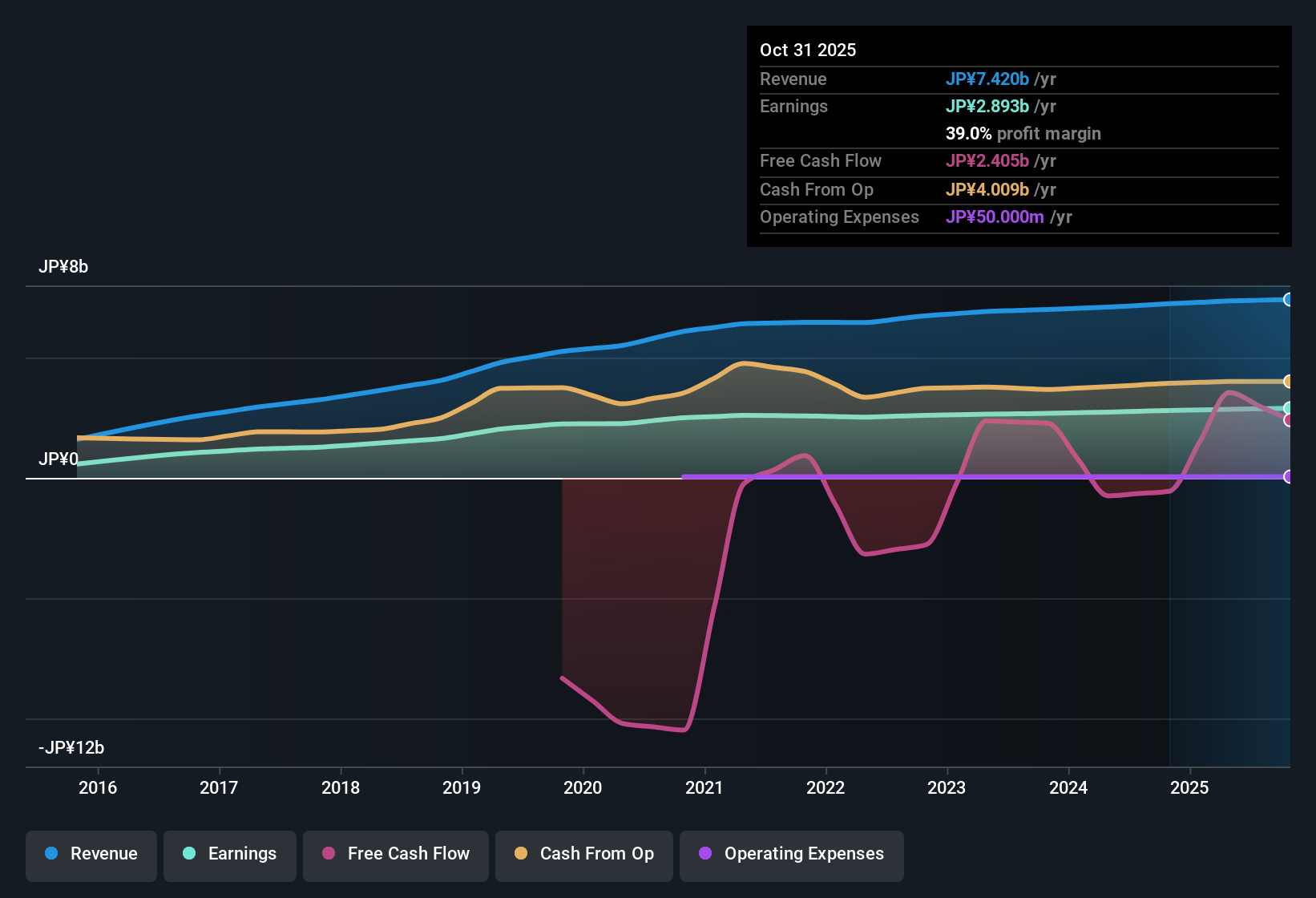

Tosei Reit Investment (TSE:3451) has just posted its FY 2025 second half numbers, with revenue at ¥3.7 billion and EPS of ¥3,873, setting the tone for another steady year of distributions. The REIT has seen revenue edge from ¥3.7 billion in FY 2024 second half to ¥3.7 billion in FY 2025 second half, while trailing twelve month EPS moved from ¥7,501 to ¥7,685, leaving investors with a picture of incremental progress rather than a step change in performance as they weigh the latest results against distribution prospects and cash generation.

See our full analysis for Tosei Reit Investment.With the headline figures on the table, the next step is to see how these numbers line up with the prevailing stories around Tosei Reit Investment and whether the data backs, tempers, or contradicts those narratives.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Margin Holds Near 39%

- Trailing twelve month net income reached ¥2,893 million on ¥7,420 million of revenue, keeping net margin at roughly 39% versus about 38.7% a year earlier.

- What stands out for a bullish angle is that earnings have grown about 2.8% per year over five years and 3.2% over the last year, which aligns with the stable margin profile, yet the pace is modest for anyone hoping for a rapid growth story.

- With EPS over the last twelve months at about ¥7,685 compared with roughly ¥7,501 a year earlier, the growth rate is steady but not dramatic.

- Revenue over the same trailing period edged from ¥7,239 million to ¥7,420 million, reinforcing a slow and incremental expansion that supports income continuity more than aggressive upside.

Valuation Gap Versus DCF Fair Value

- The units trade at ¥145,100 against a DCF fair value of about ¥77,157, while the price to earnings ratio sits at 18.9 times, below both the JP REITs average of 19.8 times and the peer average of 22.1 times.

- Critics highlight that the sizable gap between the current price and the DCF fair value heavily challenges any bullish claim that the units are clearly cheap just because the P E multiple is lower than peers.

- The nearly 50% premium of the market price to the DCF fair value contrasts with the modest 2.8% annual earnings growth, which is not the kind of high growth that typically justifies a large valuation stretch.

- Even though the 18.9 times P E is below peers, the combination of slow earnings growth and a DCF level far under the current price suggests valuation support is more constrained than a simple relative multiple comparison might imply.

5.16 Percent Yield but Cash Coverage Tight

- The REIT offers a 5.16% dividend yield, yet that payout is not well covered by free cash flow and debt is not well covered by operating cash flow according to the latest analysis.

- Skeptics argue that a yield led story is less compelling when cash coverage is thin, and the data on cash flow coverage meaningfully backs this cautious view rather than a straightforward bullish income thesis.

- Dividend coverage concerns sit alongside leverage coverage issues, with operating cash flow described as insufficient to comfortably cover debt. This raises the bar for how much risk investors are taking for that 5.16% yield.

- Set against earnings growth of just 3.2% over the last year, the reliance on distributions in excess of robust free cash flow makes the income stream more sensitive to any setback in rental income or refinancing costs.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Tosei Reit Investment's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Tosei Reit Investment combines modest earnings growth with strained cash coverage of dividends and debt, which sharpens concerns around the sustainability of its income profile.

If that balance sheet risk feels uncomfortable, use our solid balance sheet and fundamentals stocks screener (1943 results) to quickly shift your focus toward companies built on stronger finances and more resilient cash coverage today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tosei Reit Investment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3451

Tosei Reit Investment

Targeting relatively small- and medium-sized office buildings, retail facilities, residential properties and logistics facilities as major marketable real estate and thus its investment properties from among the vast existing building stock(Note) in Japan’s real estate market, and leveraging the three major strengths representing the core competencies of Tosei Corporation (“Tosei”), the Asset Manager’s parent company, Tosei Reit Investment Corporation (“Tosei Reit”) assesses the potential of assets as rental properties with an emphasis on yield levels and stability, and invests in and manages them with an eye to the possibility for adding value as it aims to increase unitholder value.

Proven track record average dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion