Advertisement

- Japan

- /

- Industrial REITs

- /

- TSE:3281

GLP J-REIT (TSE:3281) Valuation in Focus After Lower Dividend and Earnings Guidance

Simply Wall St

Reviewed by Simply Wall St

GLP J-REIT (TSE:3281) updated its earnings and dividend guidance for the coming year, signaling that both net income per unit and dividends are expected to dip compared to previous periods. As a result, investors responded by reevaluating potential returns.

See our latest analysis for GLP J-REIT.

GLP J-REIT’s updated guidance prompted investors to reassess the outlook, but that hasn't stopped momentum building. Its share price is up over 12% year-to-date. The 1-year total shareholder return stands at nearly 8%, reflecting steady, if modest, long-term gains.

If you’re looking for what else could be on the move, broaden your search and discover fast growing stocks with high insider ownership

With guidance pointing to lower payouts ahead, but shares trading at a notable discount to analyst price targets, investors have to ask whether GLP J-REIT is now undervalued or if future growth is already fully reflected by the market.

Price-to-Earnings of 39x: Is it justified?

GLP J-REIT's shares currently trade at a price-to-earnings (P/E) ratio of 39, putting it at a premium compared to similar companies. With the last close at ¥139,100, the numbers indicate investors are willing to pay considerably more yen per unit of earnings than the peer group.

The P/E ratio measures how much investors are paying for every yen of earnings. This can be useful for comparing valuations across peers in the same sector. For a REIT, this metric helps gauge whether the market is pricing in high growth or other advantages, or possibly overlooking weakness. In this case, the market appears to be expecting robust future results or a substantial turnaround.

When comparing with peers, GLP J-REIT’s 39x multiple is notably higher than the peer average of 28x and even further above the Asian Industrial REITs industry average of 20.3x. Furthermore, the figure surpasses the estimated Fair Price-to-Earnings Ratio of 28.9x. This suggests that the current price might be rich unless future growth or profitability significantly exceeds typical expectations. If the market reverts closer to that fair level, there could be notable valuation shifts on the horizon.

Explore the SWS fair ratio for GLP J-REIT

Result: Price-to-Earnings of 39x (OVERVALUED)

However, slowing net income growth or a sustained drop in market momentum could quickly shift sentiment and challenge the premium valuation currently assigned to GLP J-REIT.

Find out about the key risks to this GLP J-REIT narrative.

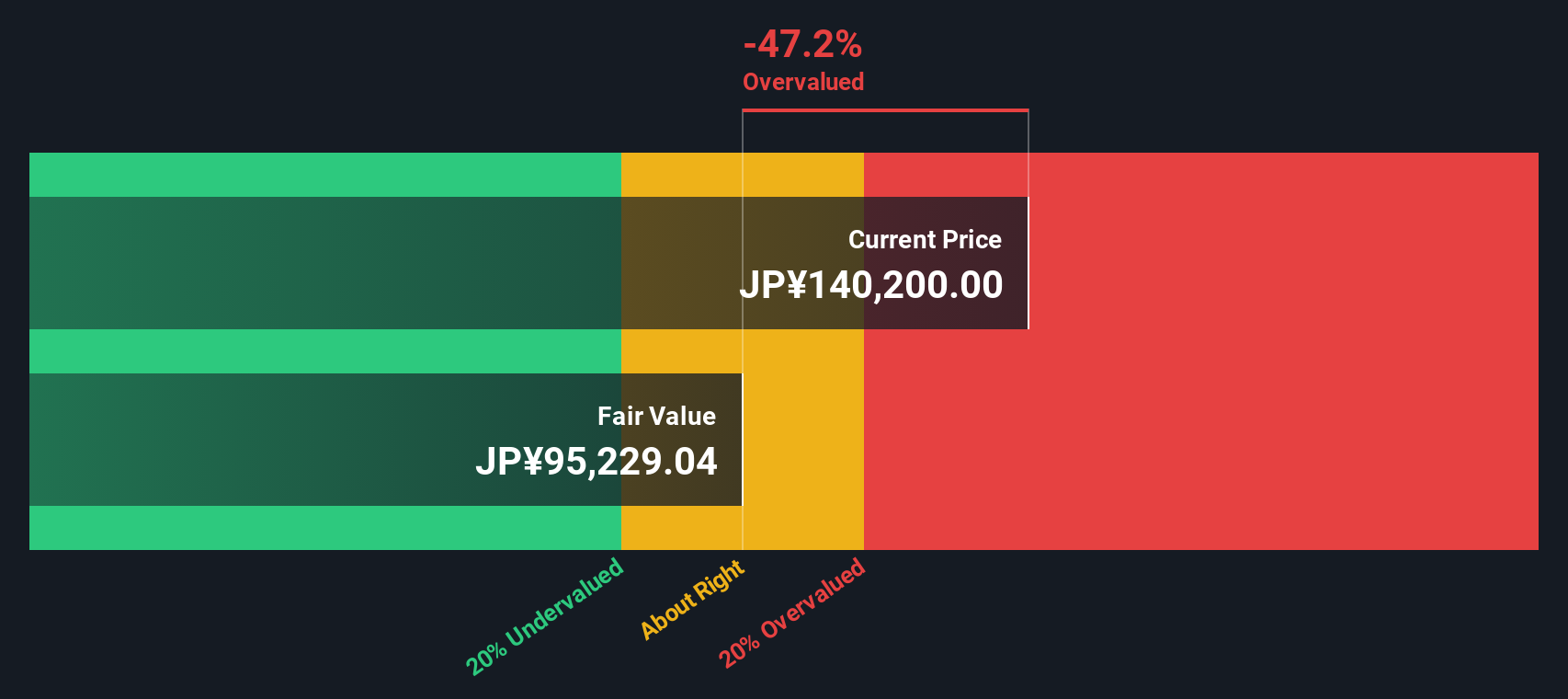

Another View: Discounted Cash Flow Model Offers a Different Perspective

Looking at GLP J-REIT through the lens of the SWS DCF model shows an even starker story. The current share price of ¥139,100 is well above the model’s estimate of fair value at around ¥94,080. This suggests that, by this method, the company appears significantly overvalued. Do market expectations justify this disconnect, or could there be a shift ahead?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out GLP J-REIT for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own GLP J-REIT Narrative

If you have your own perspective or want to investigate the numbers further, you can build your own narrative from scratch in just a few minutes. Take the next step and Do it your way.

A great starting point for your GLP J-REIT research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t just watch from the sidelines when new trends shape the market. Act now and uncover unique growth and income opportunities before they’re mainstream.

- Maximize potential returns by targeting these 869 undervalued stocks based on cash flows that currently trade below fair value. This approach may give you an edge before prices catch up.

- Strengthen your portfolio with reliable income. Pursue higher yields with these 19 dividend stocks with yields > 3% offering over 3% dividends, which can be ideal for steady cash flow.

- Ride the next technological surge and position yourself for tomorrow’s breakthroughs by checking out these 27 AI penny stocks on the frontier of artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3281

GLP J-REIT

A real estate investment corporation (“J-REIT”) specializing in logistics facilities, and it primarily invests in modern logistics facilities.

Reasonable growth potential average dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor