Advertisement

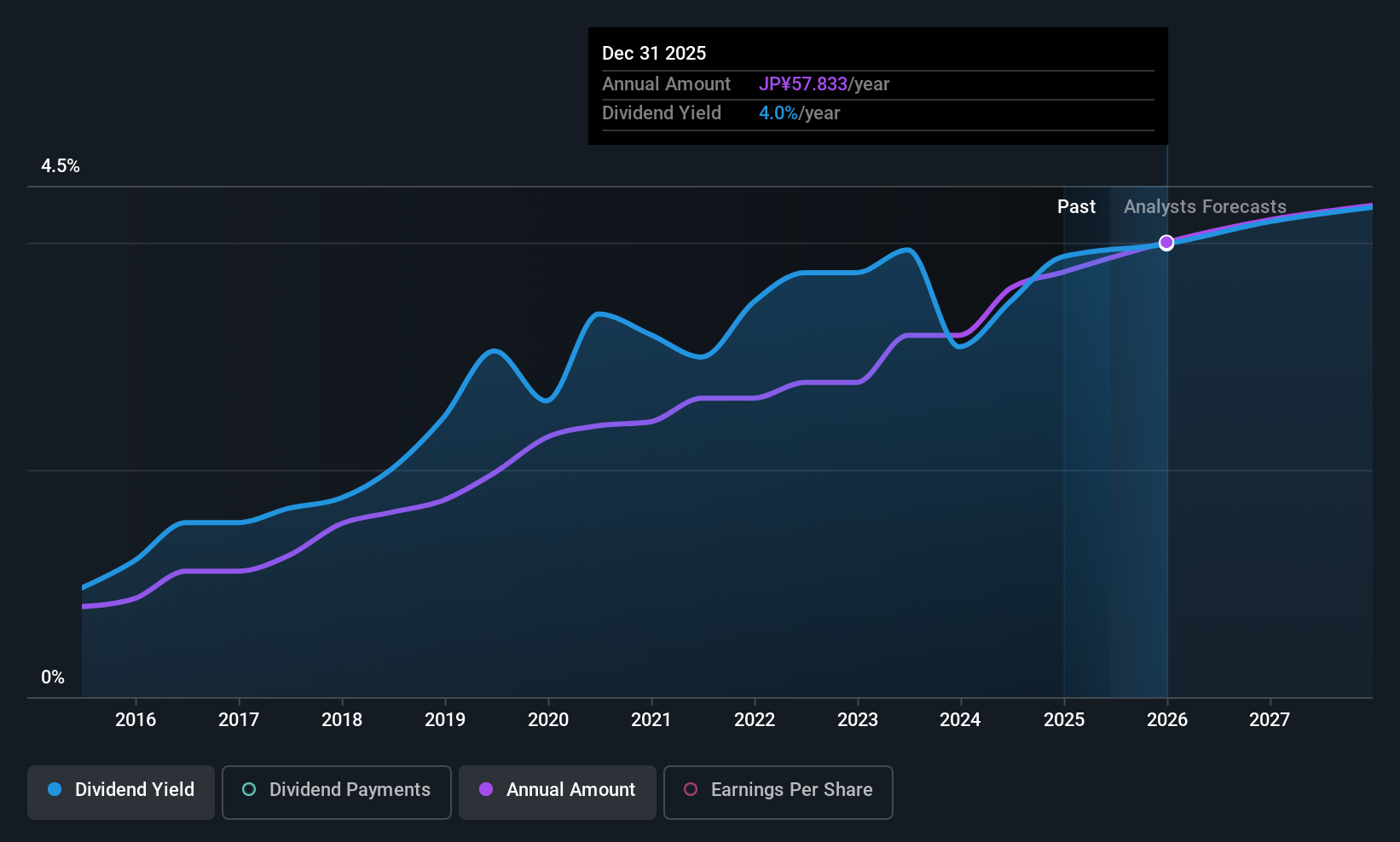

Hulic Co., Ltd.'s (TSE:3003) dividend will be increasing from last year's payment of the same period to ¥28.50 on 3rd of September. This will take the dividend yield to an attractive 3.9%, providing a nice boost to shareholder returns.

Hulic's Future Dividend Projections Appear Well Covered By Earnings

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last payment, Hulic was earning enough to cover the dividend, but free cash flows weren't positive. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

Over the next year, EPS is forecast to expand by 4.0%. If the dividend continues along recent trends, we estimate the payout ratio will be 45%, which is in the range that makes us comfortable with the sustainability of the dividend.

See our latest analysis for Hulic

Hulic Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2015, the annual payment back then was ¥11.50, compared to the most recent full-year payment of ¥57.00. This implies that the company grew its distributions at a yearly rate of about 17% over that duration. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Has Growth Potential

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. It's encouraging to see that Hulic has been growing its earnings per share at 6.8% a year over the past five years. Hulic definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think Hulic's payments are rock solid. While Hulic is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 2 warning signs for Hulic (of which 1 shouldn't be ignored!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hulic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3003

Hulic

Engages in the holding, leasing, brokerage, and sale of real estate properties in Japan.

Established dividend payer and good value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor