Advertisement

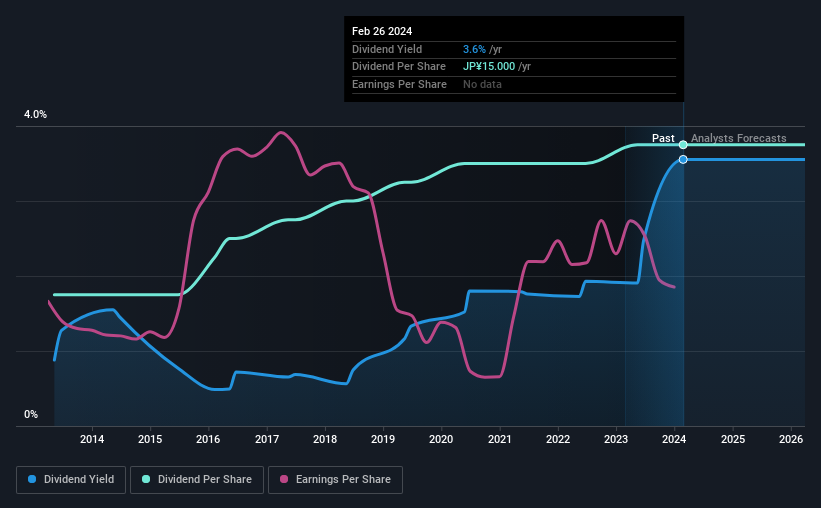

The board of Linical Co., Ltd. (TSE:2183) has announced that it will be paying its dividend of ¥15.00 on the 10th of June, an increased payment from last year's comparable dividend. This takes the dividend yield to 3.6%, which shareholders will be pleased with.

See our latest analysis for Linical

Linical's Earnings Easily Cover The Distributions

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Based on the last payment, Linical was quite comfortably earning enough to cover the dividend. This indicates that quite a large proportion of earnings is being invested back into the business.

Over the next year, EPS is forecast to fall by 5.1%. If the dividend continues along the path it has been on recently, we estimate the payout ratio could be 57%, which is comfortable for the company to continue in the future.

Linical Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2014, the dividend has gone from ¥7.00 total annually to ¥15.00. This works out to be a compound annual growth rate (CAGR) of approximately 7.9% a year over that time. Dividends have grown at a reasonable rate over this period, and without any major cuts in the payment over time, we think this is an attractive combination as it provides a nice boost to shareholder returns.

The Dividend's Growth Prospects Are Limited

Investors could be attracted to the stock based on the quality of its payment history. However, initial appearances might be deceiving. Over the past five years, it looks as though Linical's EPS has declined at around 4.3% a year. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits.

In Summary

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. The earnings coverage is acceptable for now, but with earnings on the decline we would definitely keep an eye on the payout ratio. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 1 warning sign for Linical that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2183

Linical

A global contract research organization provides full spectrum of drug development services to pharmaceutical companies worldwide.

Adequate balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor