Advertisement

A Look at TVhi Holdings (TSE:9409) Valuation Following Upgraded Earnings Outlook and Dividend Increase

Simply Wall St

Reviewed by Simply Wall St

TVhi Holdings (TSE:9409) is in the spotlight after it raised its consolidated earnings guidance for the fiscal year ending March 2026 and announced a sizable boost to its second quarter dividend. Investors are watching these moves closely because they signal stronger financial performance and higher shareholder returns.

See our latest analysis for TVhi Holdings.

TVhi Holdings' recent earnings upgrade and dividend boost seem to have fueled further momentum, building on an already robust year. The company’s share price has climbed over 45% year-to-date. Looking at the bigger picture, shareholders have enjoyed an impressive 61% total return in the past 12 months, and gains stretch even further over three and five years. This suggests long-term growth optimism is growing stronger.

If you’re interested in catching other stocks with a similar upswing, now might be the perfect time to see what’s out there in our fast growing stocks with high insider ownership.

With the stock having surged over the past year, investors are now left wondering if TVhi Holdings remains undervalued or if the current price already reflects expectations for future growth. Could there still be a buying opportunity?

Price-to-Earnings of 10x: Is it justified?

TVhi Holdings trades at a price-to-earnings (P/E) ratio of 10x, noticeably below key industry benchmarks and its own fair value estimate. At last close of ¥3,255, the market is attributing a lower multiple than both the peer group and broad sector averages.

The price-to-earnings (P/E) ratio shows how much investors are willing to pay for each yen of current earnings. In the media sector, this is especially relevant because it reflects market confidence in future profit growth and overall earnings stability.

Given TVhi Holdings' robust profit expansion, as highlighted by an earnings growth rate far above the industry this past year, it appears the market may be discounting these strong results. The company’s P/E ratio not only trails the JP Media industry average of 16.1x, but also stands at half the estimated fair P/E ratio of 20x. If sentiment or results catch up with these stronger metrics, there could be room for a re-rating.

Explore the SWS fair ratio for TVhi Holdings

Result: Price-to-Earnings of 10x (UNDERVALUED)

However, slower annual net income growth and a price target that is only marginally above the current price could temper the outlook for further near-term gains.

Find out about the key risks to this TVhi Holdings narrative.

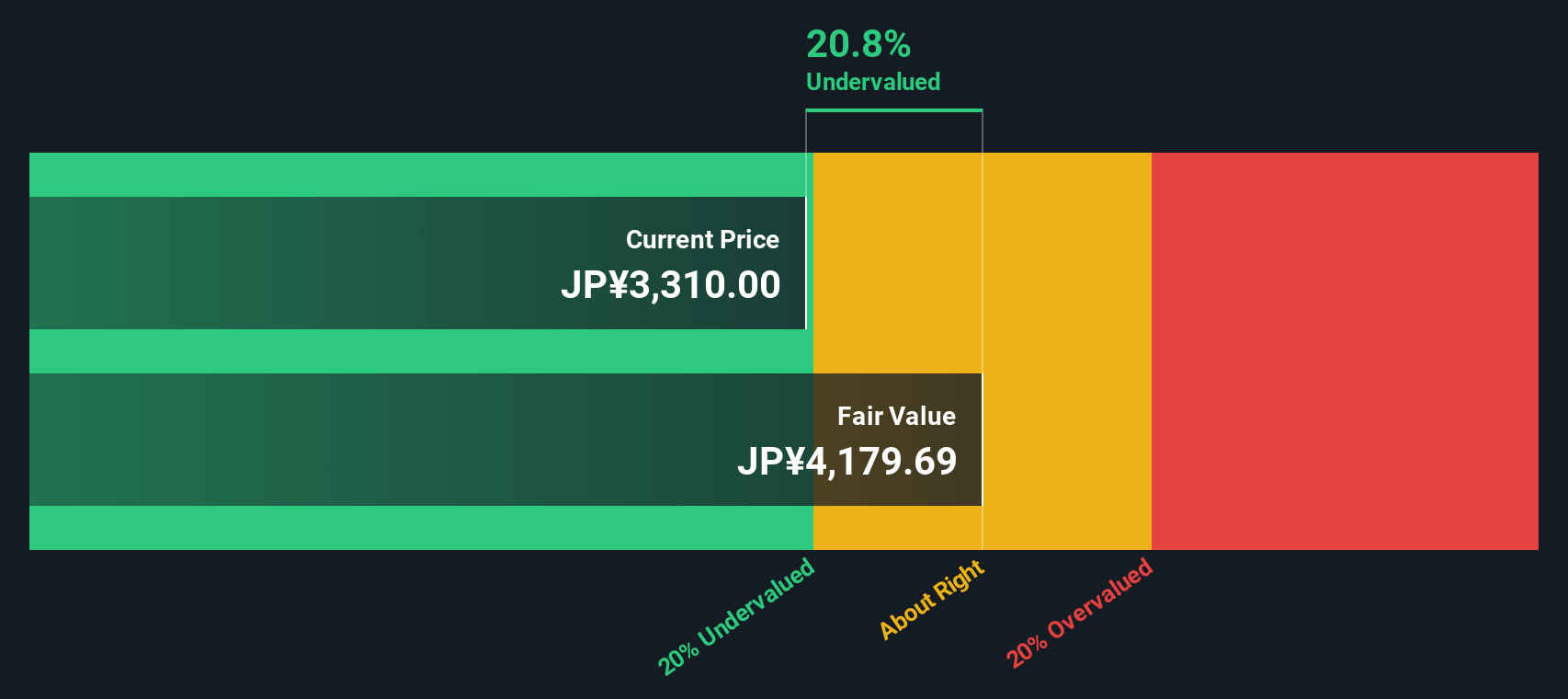

Another View: Discounted Cash Flow Sheds More Light

While the price-to-earnings ratio suggests TVhi Holdings might be undervalued, our SWS DCF model offers an even starker perspective. It estimates the company’s fair value at ¥4,179.69, which is 22% higher than the current share price. Could the market be missing something here?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TVhi Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 897 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own TVhi Holdings Narrative

If you think there’s more to the story or want to dive into the figures yourself, it only takes a few minutes to form your own perspective. Do it your way.

A great starting point for your TVhi Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Make your next smart investing move and don’t leave potential upside on the table. You could be getting in early on opportunities others miss.

- Uncover new growth potential by checking out these 897 undervalued stocks based on cash flows that are trading below what their financials suggest they’re worth.

- Tap into technology’s most innovative players and target the future of artificial intelligence through these 27 AI penny stocks.

- Boost your portfolio with cash returns by exploring these 15 dividend stocks with yields > 3% offering attractive yields over 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TVhi Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9409

TVhi Holdings

Engages in the television (TV) broadcasting business in Japan and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor