Advertisement

As global markets react to the Trump administration's emerging policies, U.S. stocks have reached record highs, buoyed by optimism around softer tariffs and AI investments. In this dynamic environment, dividend stocks can offer a blend of income and potential growth, making them an appealing option for investors seeking stability amidst market fluctuations.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Tsubakimoto Chain (TSE:6371) | 4.25% | ★★★★★★ |

| Guaranty Trust Holding (NGSE:GTCO) | 6.04% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.90% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.67% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.49% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.45% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.01% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.41% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.46% | ★★★★★★ |

| E J Holdings (TSE:2153) | 4.04% | ★★★★★★ |

Click here to see the full list of 1971 stocks from our Top Dividend Stocks screener.

Let's dive into some prime choices out of the screener.

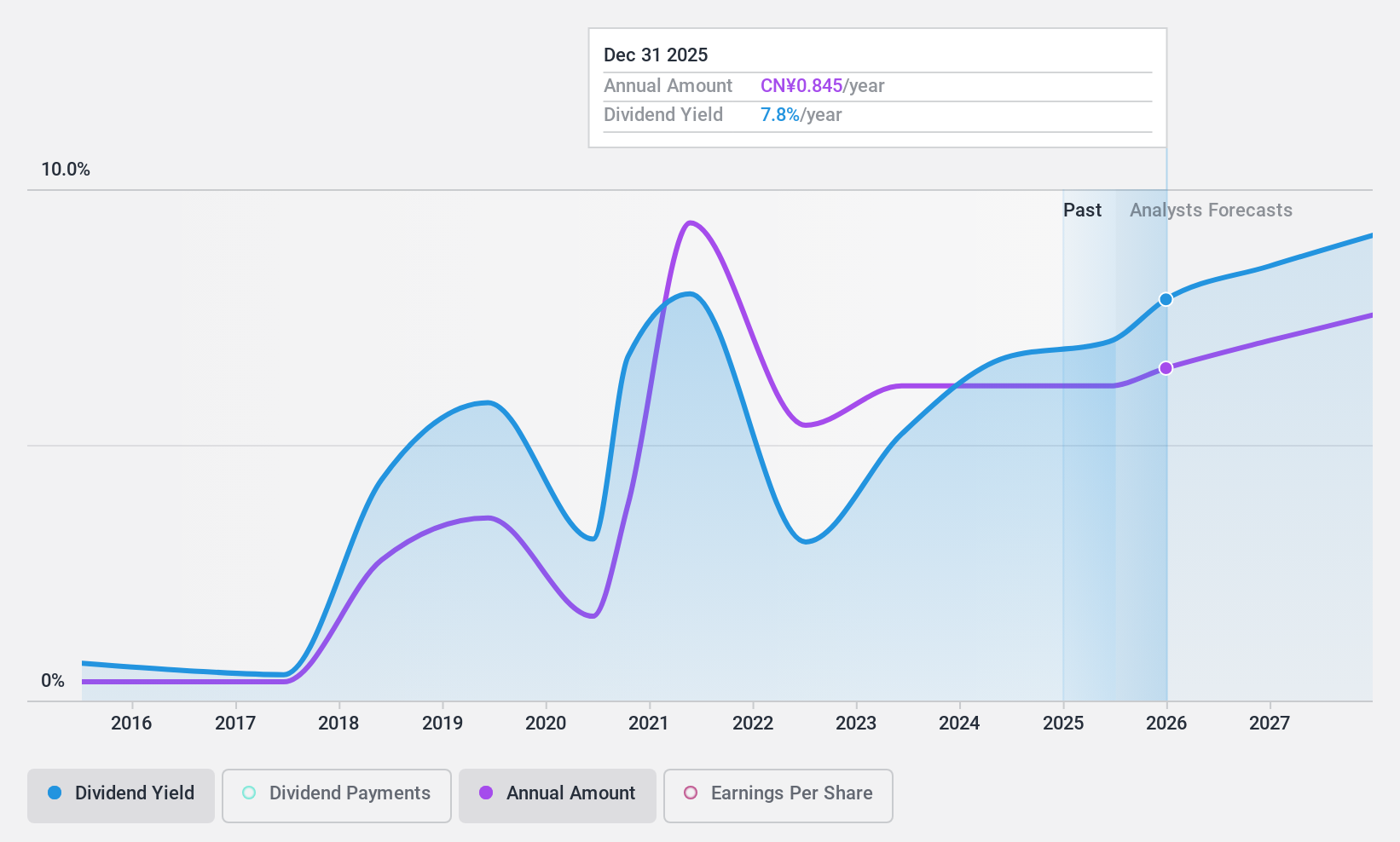

Luyang Energy-Saving Materials (SZSE:002088)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Luyang Energy-Saving Materials Co., Ltd. is engaged in the research, development, production, and sale of energy-saving products such as ceramic fiber, alumina fiber, soluble fiber, basalt fiber, and insulating firebrick both in China and internationally with a market cap of CN¥6.13 billion.

Operations: Luyang Energy-Saving Materials Co., Ltd. generates revenue through the production and sale of energy-efficient materials, including ceramic fiber, alumina fiber, soluble fiber, basalt fiber, and insulating firebrick for domestic and international markets.

Dividend Yield: 6.5%

Luyang Energy-Saving Materials offers a dividend yield of 6.46%, placing it among the top 25% of dividend payers in China. However, the sustainability is questionable as dividends are not well covered by free cash flows and have been volatile over the past decade. The company's payout ratio is high at 87.1%, and its price-to-earnings ratio of 13.5x suggests it trades at good value compared to peers, despite recent declines in earnings and revenue.

- Take a closer look at Luyang Energy-Saving Materials' potential here in our dividend report.

- Our valuation report unveils the possibility Luyang Energy-Saving Materials' shares may be trading at a discount.

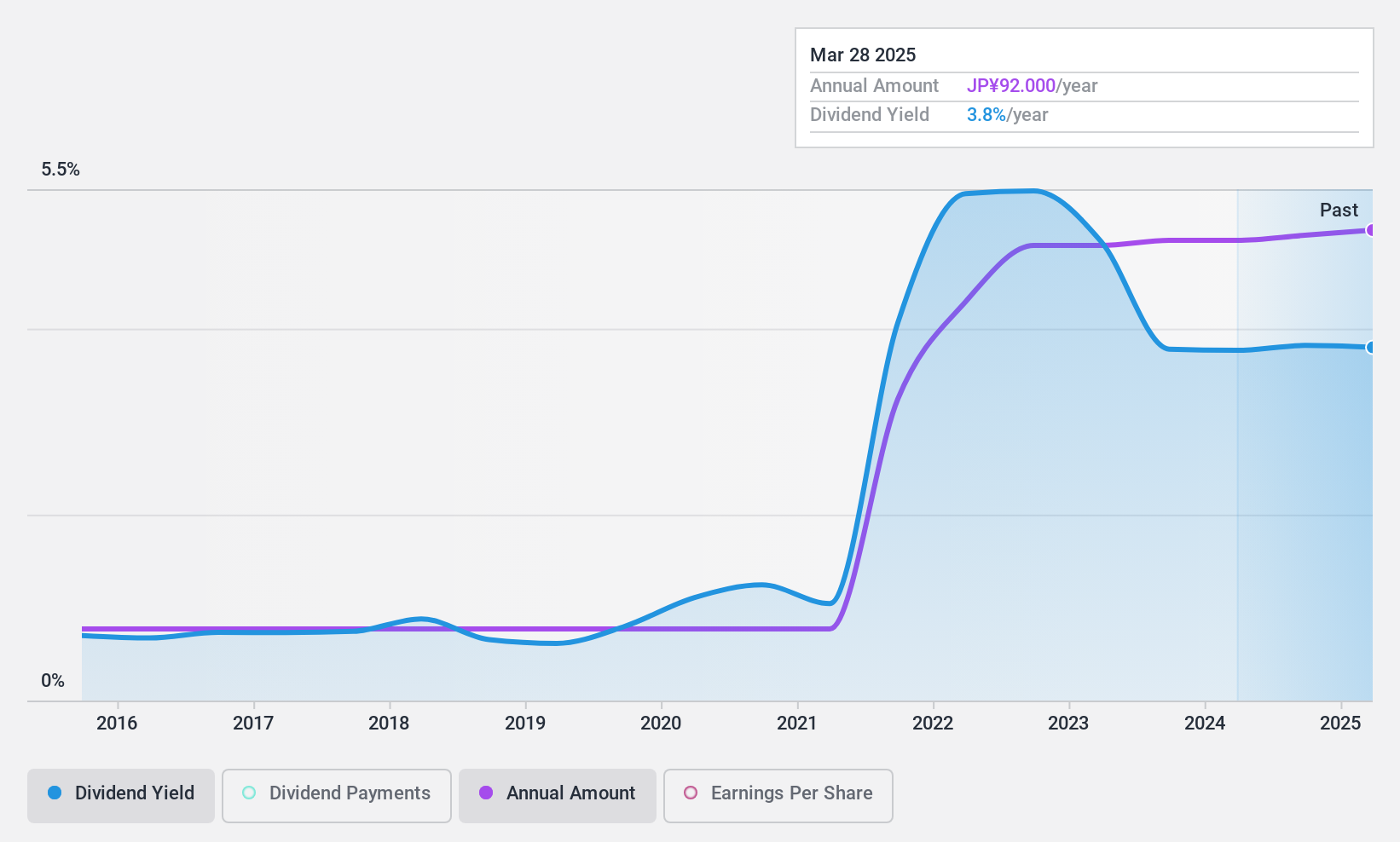

Toyo Seikan Group Holdings (TSE:5901)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Toyo Seikan Group Holdings, Ltd. manufactures and sells packaging containers both in Japan and internationally, with a market cap of ¥381.83 billion.

Operations: Toyo Seikan Group Holdings generates revenue primarily from its Packaging Business at ¥601.74 billion, followed by the Engineering / Filling / Logistics Business at ¥231.32 billion, Steel Plate Business at ¥112.21 billion, and Functional Material Related Business at ¥47.26 billion, with additional contributions from its Real Estate Related Business totaling ¥9.54 billion.

Dividend Yield: 3.9%

Toyo Seikan Group Holdings' dividend yield is in the top 25% of Japan's market, but its dividends have been volatile over the past decade. Despite this instability, recent earnings growth of 61.9% supports a payout ratio of 75.6%, indicating dividends are covered by earnings and cash flows, with a low cash payout ratio of 24.7%. The company trades at a considerable discount to estimated fair value, though its dividend history remains inconsistent despite increases over ten years.

- Dive into the specifics of Toyo Seikan Group Holdings here with our thorough dividend report.

- According our valuation report, there's an indication that Toyo Seikan Group Holdings' share price might be on the expensive side.

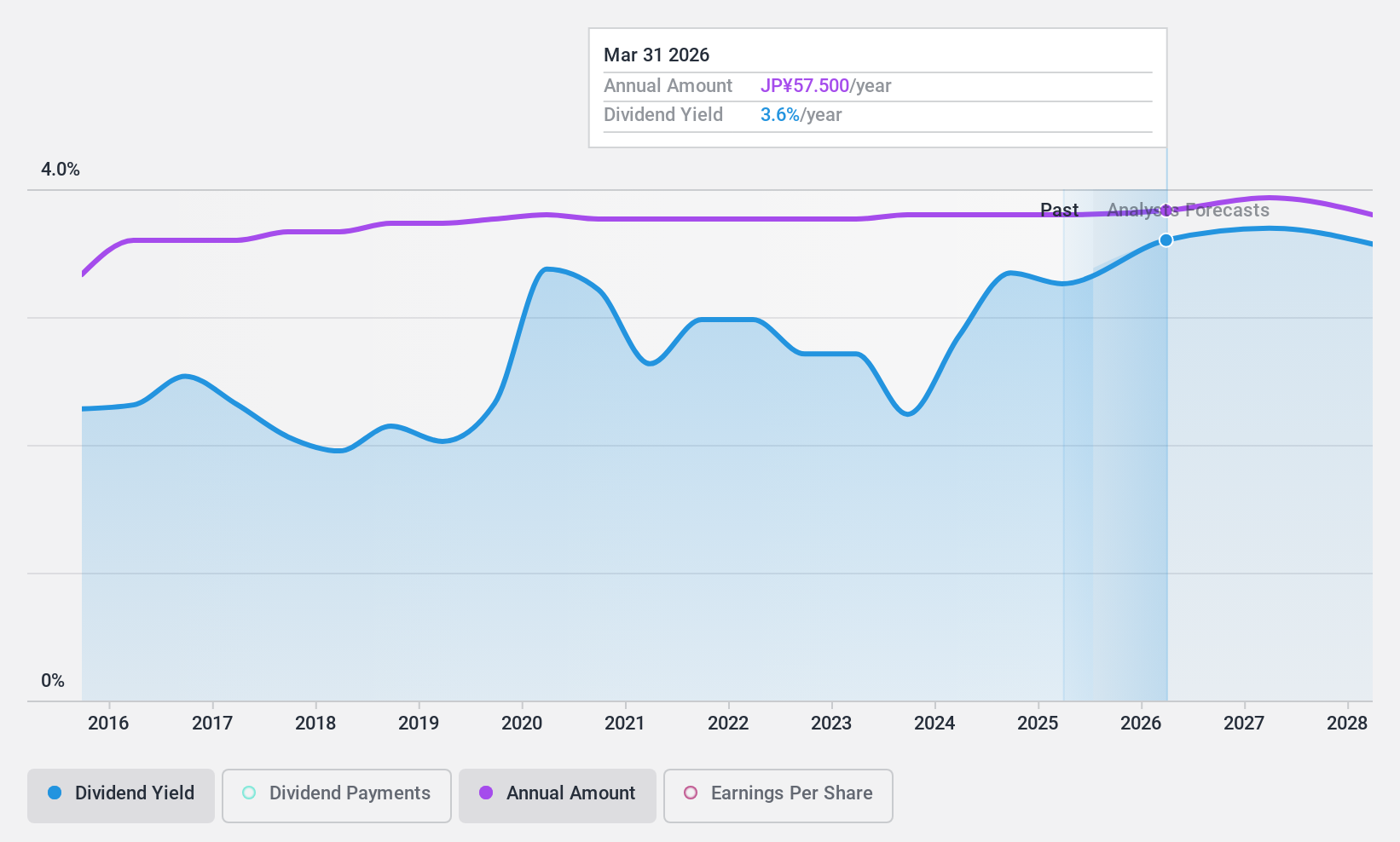

Daiichikosho (TSE:7458)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Daiichikosho Co., Ltd. operates in Japan, focusing on the sale and rental of commercial karaoke systems, with a market cap of ¥186.70 billion.

Operations: Daiichikosho Co., Ltd. generates revenue primarily from its Commercial Karaoke segment, which accounts for ¥61.39 billion, and its Karaoke and Restaurant Business, contributing ¥65.87 billion.

Dividend Yield: 3.1%

Daiichikosho's dividends have been stable and growing over the past decade, supported by a low payout ratio of 38.9%, though not covered by free cash flows. The dividend yield of 3.13% is below Japan's top quartile payers. Despite high non-cash earnings, future earnings are expected to decline by 3.3% annually over three years. Recent announcements include a consistent JPY 28 per share dividend and an upcoming karaoke system launch in April 2025, potentially impacting future revenue streams positively.

- Navigate through the intricacies of Daiichikosho with our comprehensive dividend report here.

- Our expertly prepared valuation report Daiichikosho implies its share price may be lower than expected.

Key Takeaways

- Delve into our full catalog of 1971 Top Dividend Stocks here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toyo Seikan Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5901

Toyo Seikan Group Holdings

Manufactures and sells packaging containers in Japan and internationally.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor