- Japan

- /

- Interactive Media and Services

- /

- TSE:2371

Kakaku.com (TSE:2371) Is Due To Pay A Dividend Of ¥23.00

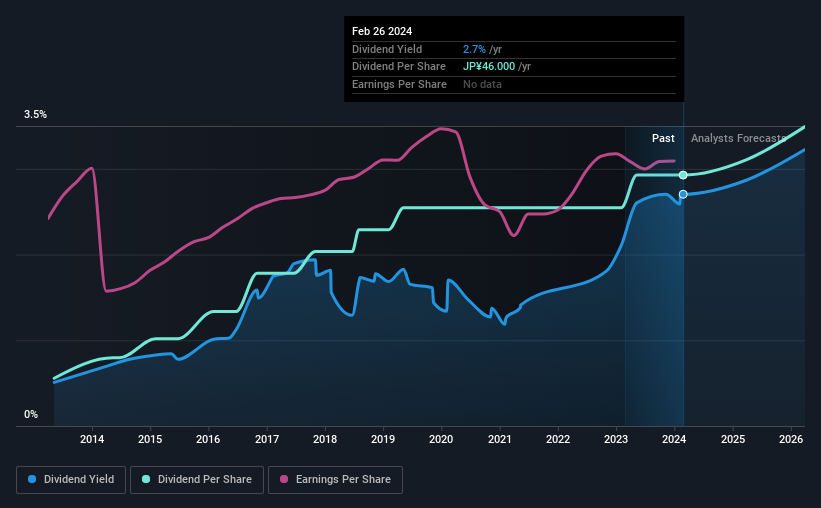

Kakaku.com, Inc.'s (TSE:2371) investors are due to receive a payment of ¥23.00 per share on 21st of June. This will take the dividend yield to an attractive 2.7%, providing a nice boost to shareholder returns.

See our latest analysis for Kakaku.com

Kakaku.com's Earnings Easily Cover The Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. The last payment made up 79% of earnings, but cash flows were much higher. This leaves plenty of cash for reinvestment into the business.

Looking forward, earnings per share is forecast to rise by 39.3% over the next year. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 45% which would be quite comfortable going to take the dividend forward.

Kakaku.com Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. The dividend has gone from an annual total of ¥8.75 in 2014 to the most recent total annual payment of ¥46.00. This means that it has been growing its distributions at 18% per annum over that time. It is good to see that there has been strong dividend growth, and that there haven't been any cuts for a long time.

Kakaku.com May Find It Hard To Grow The Dividend

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Unfortunately, Kakaku.com's earnings per share has been essentially flat over the past five years, which means the dividend may not be increased each year. Slow growth and a high payout ratio could mean that Kakaku.com has maxed out the amount that it has been able to pay to shareholders. When the rate of return on reinvestment opportunities falls below a certain minimum level, companies often elect to pay a larger dividend instead. This is why many mature companies often have larger dividend yields.

Our Thoughts On Kakaku.com's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company is generating plenty of cash, but we still think the dividend is a bit high for comfort. We don't think Kakaku.com is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Earnings growth generally bodes well for the future value of company dividend payments. See if the 11 Kakaku.com analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Is Kakaku.com not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kakaku.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2371

Kakaku.com

Provides purchase support, restaurant review, and other services in Japan.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion