- Japan

- /

- Interactive Media and Services

- /

- TSE:2371

3 Stocks Estimated To Be Discounted By Up To -32.8%

Reviewed by Simply Wall St

As global markets navigate through a period of mixed economic signals, with U.S. indexes approaching record highs and European business activity contracting, investors are keenly observing potential opportunities amidst the volatility. In this environment, identifying undervalued stocks can be a strategic move for those looking to capitalize on discrepancies between current stock prices and their intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Gaming Realms (AIM:GMR) | £0.3665 | £0.73 | 49.6% |

| BMC Medical (SZSE:301367) | CN¥67.53 | CN¥137.09 | 50.7% |

| Tongqinglou Catering (SHSE:605108) | CN¥21.71 | CN¥43.42 | 50% |

| EnomotoLtd (TSE:6928) | ¥1474.00 | ¥2936.95 | 49.8% |

| Winking Studios (Catalist:WKS) | SGD0.27 | SGD0.54 | 49.6% |

| Equity Bancshares (NYSE:EQBK) | US$49.21 | US$98.42 | 50% |

| Intermedical Care and Lab Hospital (SET:IMH) | THB4.94 | THB9.86 | 49.9% |

| Atlas Arteria (ASX:ALX) | A$4.94 | A$9.69 | 49% |

| Fine Foods & Pharmaceuticals N.T.M (BIT:FF) | €7.88 | €15.63 | 49.6% |

| Chengdu Olymvax Biopharmaceuticals (SHSE:688319) | CN¥11.60 | CN¥21.64 | 46.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

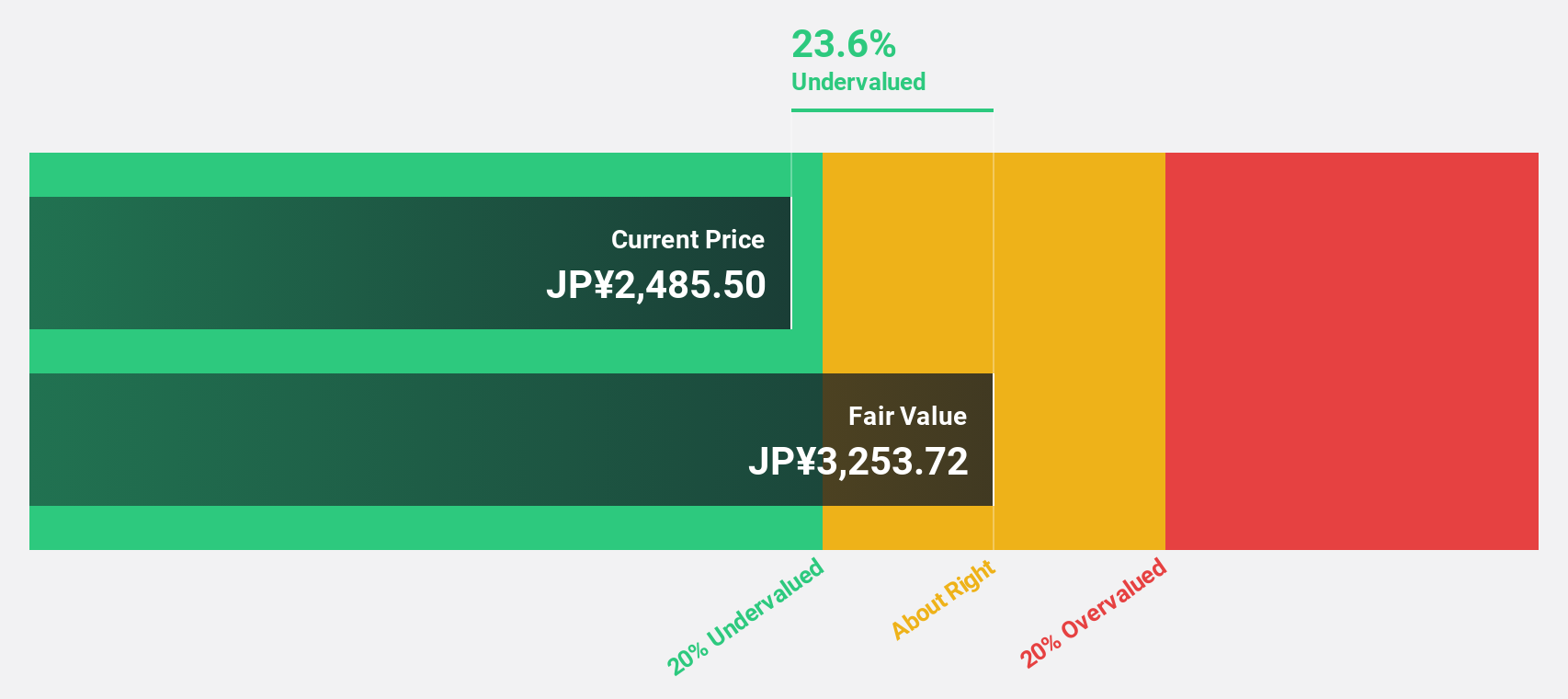

Kakaku.com (TSE:2371)

Overview: Kakaku.com, Inc. operates in Japan offering purchase support and restaurant review services through its subsidiaries, with a market cap of ¥462.40 billion.

Operations: The company's revenue segments include purchase support services generating ¥52.30 billion and restaurant review services contributing ¥13.75 billion.

Estimated Discount To Fair Value: 9%

Kakaku.com is trading at ¥2430.5, approximately 9% below its estimated fair value of ¥2672.28, suggesting it may be undervalued based on cash flows. The company's earnings grew by 23.5% last year and are expected to grow at 9.96% annually, outpacing the Japanese market's average growth rate of 7.9%. Despite a modest revenue growth forecast of 9.2%, Kakaku.com maintains a reliable dividend yield of 2.06%.

- The growth report we've compiled suggests that Kakaku.com's future prospects could be on the up.

- Navigate through the intricacies of Kakaku.com with our comprehensive financial health report here.

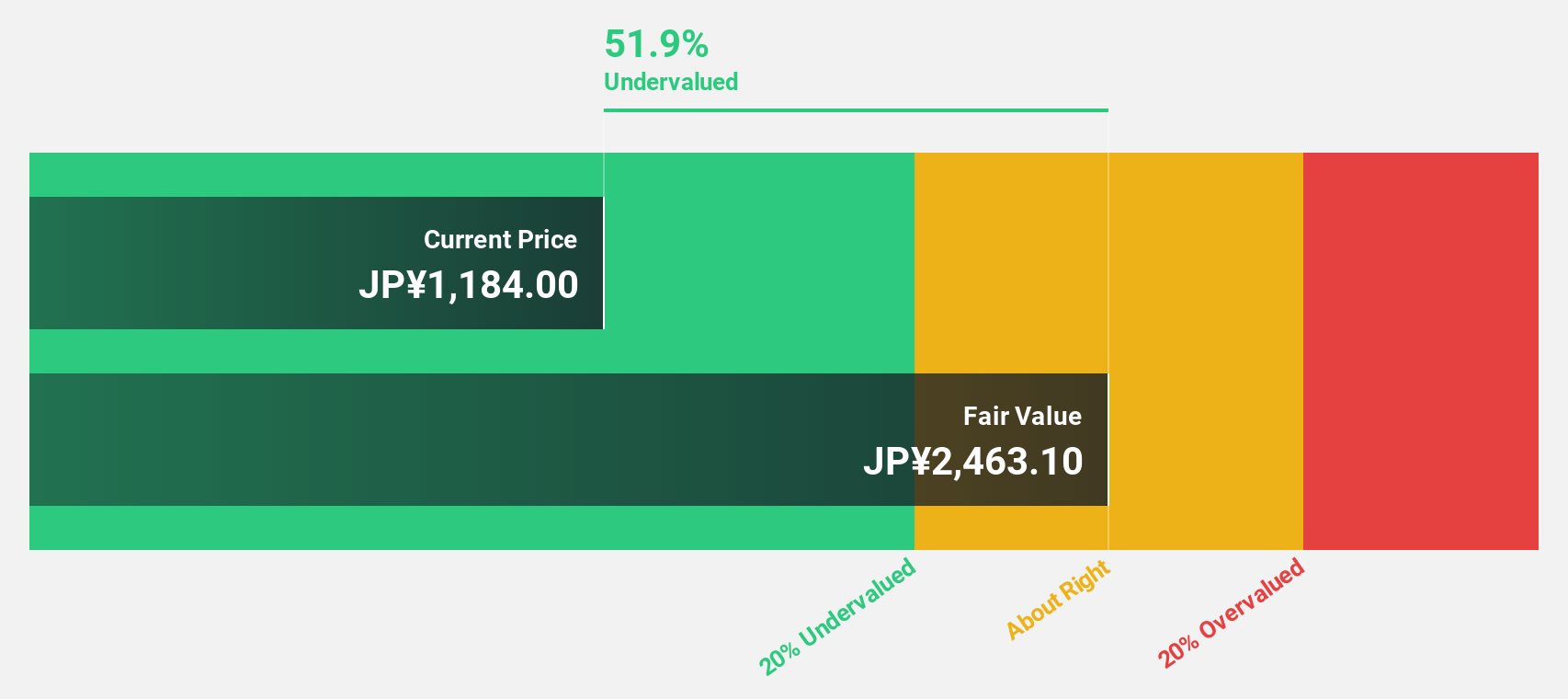

SIGMAXYZ Holdings (TSE:6088)

Overview: SIGMAXYZ Holdings Inc. operates in Japan through its subsidiaries, offering consulting, investment, and M&A advisory services with a market cap of ¥156.74 billion.

Operations: The company generates revenue primarily through its Consulting Business, which accounts for ¥24.30 billion, and its Investment Business, contributing ¥184.92 million.

Estimated Discount To Fair Value: -32.8%

SIGMAXYZ Holdings is trading at ¥1797, above its estimated fair value of ¥1352.8, indicating it may not be undervalued based on cash flows. The company forecasts annual earnings growth of 16.2%, surpassing the Japanese market's average growth rate of 7.9%. Recent buybacks totaling ¥637.2 million could support share price stability despite a volatile period and shareholder dilution last year. Dividend guidance suggests a reduction to ¥19 per share from last year's ¥27 per share.

- Upon reviewing our latest growth report, SIGMAXYZ Holdings' projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of SIGMAXYZ Holdings.

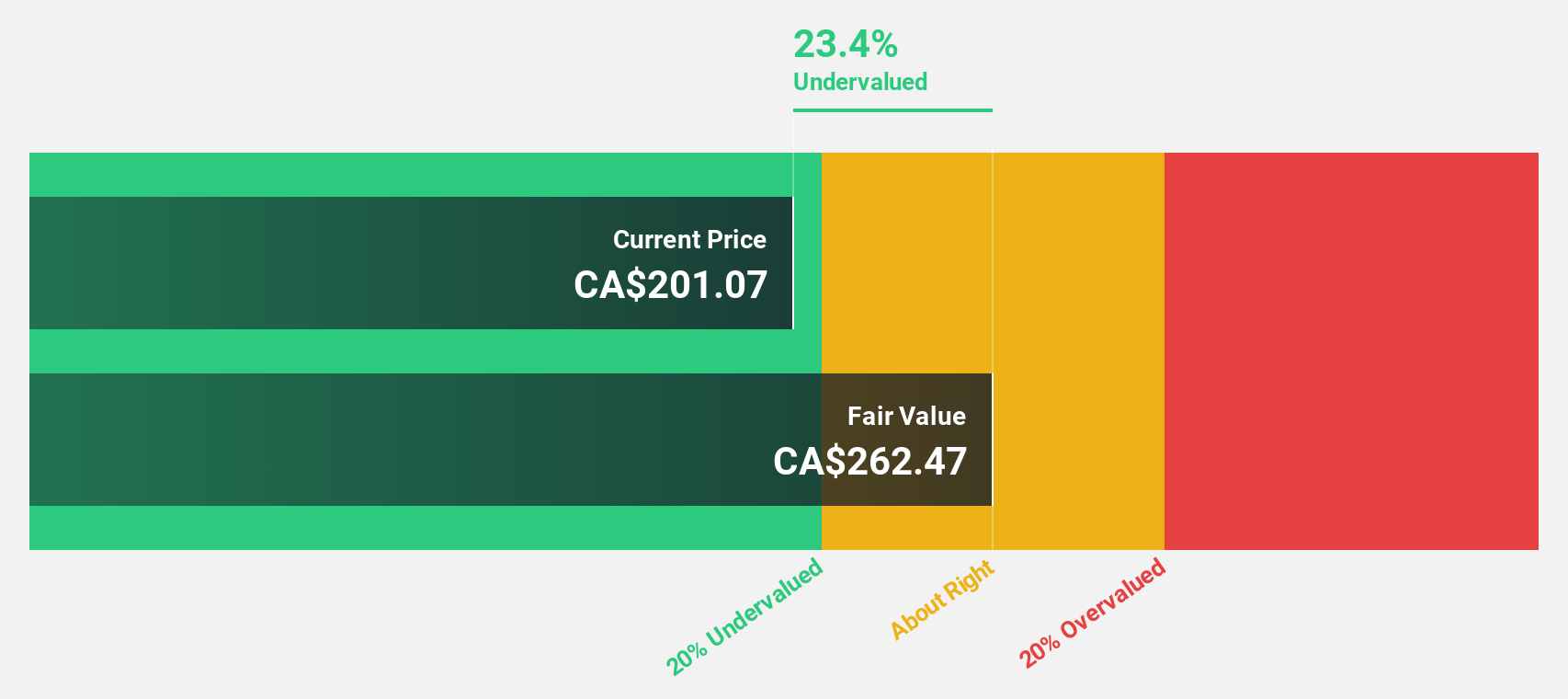

Kinaxis (TSX:KXS)

Overview: Kinaxis Inc. offers cloud-based subscription software for supply chain operations across the United States, Europe, Asia, and Canada, with a market cap of CA$4.82 billion.

Operations: The company's revenue is primarily derived from its Software & Programming segment, totaling $471.17 million.

Estimated Discount To Fair Value: 40.3%

Kinaxis, trading at CA$171.66, is significantly undervalued compared to its estimated fair value of CA$287.71. Despite recent leadership changes and activist pressures for a sale, the company maintains robust growth prospects with earnings expected to rise significantly over the next three years. Recent client wins like Elida Beauty and strategic partnerships such as with ExxonMobil bolster its market position in supply chain solutions, enhancing cash flow potential despite current valuation disparities.

- In light of our recent growth report, it seems possible that Kinaxis' financial performance will exceed current levels.

- Take a closer look at Kinaxis' balance sheet health here in our report.

Next Steps

- Dive into all 923 of the Undervalued Stocks Based On Cash Flows we have identified here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kakaku.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2371

Kakaku.com

Engages in the provision of purchase support, restaurant review, and other services in Japan.

Outstanding track record with flawless balance sheet and pays a dividend.