Advertisement

What Tenma Corporation's (TSE:7958) 40% Share Price Gain Is Not Telling You

Tenma Corporation (TSE:7958) shares have had a really impressive month, gaining 40% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 55%.

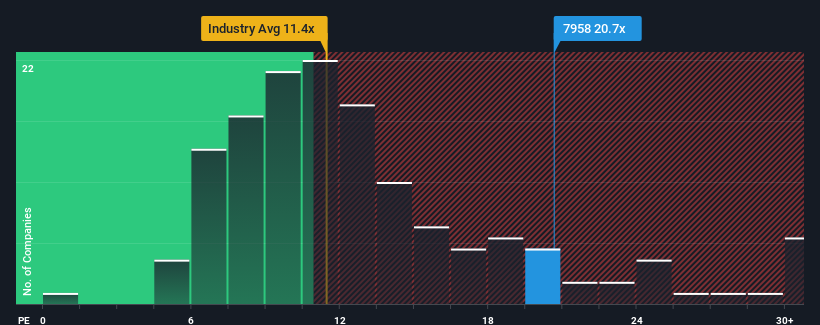

After such a large jump in price, given close to half the companies in Japan have price-to-earnings ratios (or "P/E's") below 13x, you may consider Tenma as a stock to avoid entirely with its 20.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Tenma has been doing a good job lately as it's been growing earnings at a solid pace. It might be that many expect the respectable earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Tenma

What Are Growth Metrics Telling Us About The High P/E?

Tenma's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered a decent 8.1% gain to the company's bottom line. This was backed up an excellent period prior to see EPS up by 33% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 10% shows it's about the same on an annualised basis.

With this information, we find it interesting that Tenma is trading at a high P/E compared to the market. Apparently many investors in the company are more bullish than recent times would indicate and aren't willing to let go of their stock right now. Nevertheless, they may be setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Final Word

Tenma's P/E is flying high just like its stock has during the last month. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Tenma currently trades on a higher than expected P/E since its recent three-year growth is only in line with the wider market forecast. When we see average earnings with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Tenma (1 is a bit concerning) you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Tenma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7958

Tenma

Engages in the manufacture and sale of plastic products in Japan and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor