Advertisement

- Japan

- /

- Metals and Mining

- /

- TSE:5603

Some Investors May Be Willing To Look Past Kogi's (TSE:5603) Soft Earnings

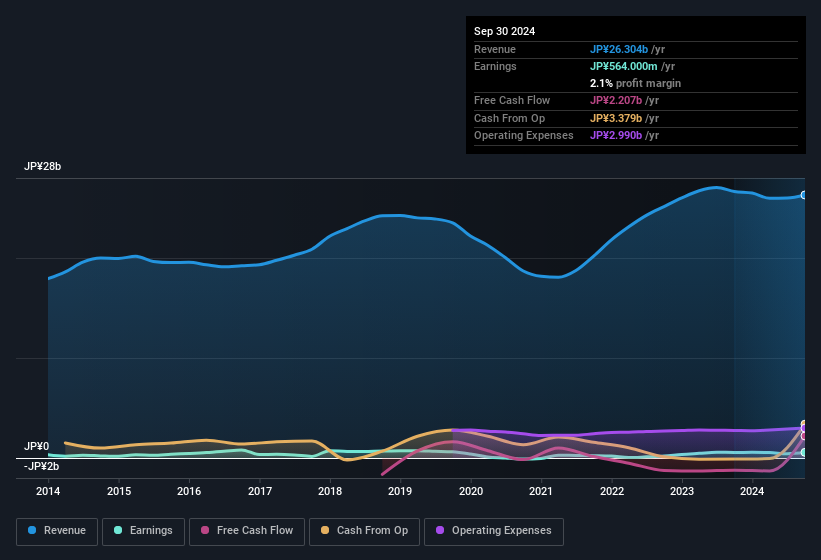

Shareholders appeared unconcerned with Kogi Corporation's (TSE:5603) lackluster earnings report last week. We did some digging, and we believe the earnings are stronger than they seem.

Check out our latest analysis for Kogi

The Impact Of Unusual Items On Profit

To properly understand Kogi's profit results, we need to consider the JP¥237m expense attributed to unusual items. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. Assuming those unusual expenses don't come up again, we'd therefore expect Kogi to produce a higher profit next year, all else being equal.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Kogi.

Our Take On Kogi's Profit Performance

Because unusual items detracted from Kogi's earnings over the last year, you could argue that we can expect an improved result in the current quarter. Because of this, we think Kogi's earnings potential is at least as good as it seems, and maybe even better! And on top of that, its earnings per share have grown at an extremely impressive rate over the last three years. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you'd like to know more about Kogi as a business, it's important to be aware of any risks it's facing. Case in point: We've spotted 3 warning signs for Kogi you should be aware of.

Today we've zoomed in on a single data point to better understand the nature of Kogi's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Kogi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5603

Kogi

Manufactures and sells casting roll-related products, environmental equipment, and friction materials in Japan and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor