Advertisement

Impressive Earnings May Not Tell The Whole Story For Fujimi (TSE:5384)

Last week's profit announcement from Fujimi Incorporated (TSE:5384) was underwhelming for investors, despite headline numbers being robust. We did some digging and found some worrying underlying problems.

A Closer Look At Fujimi's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

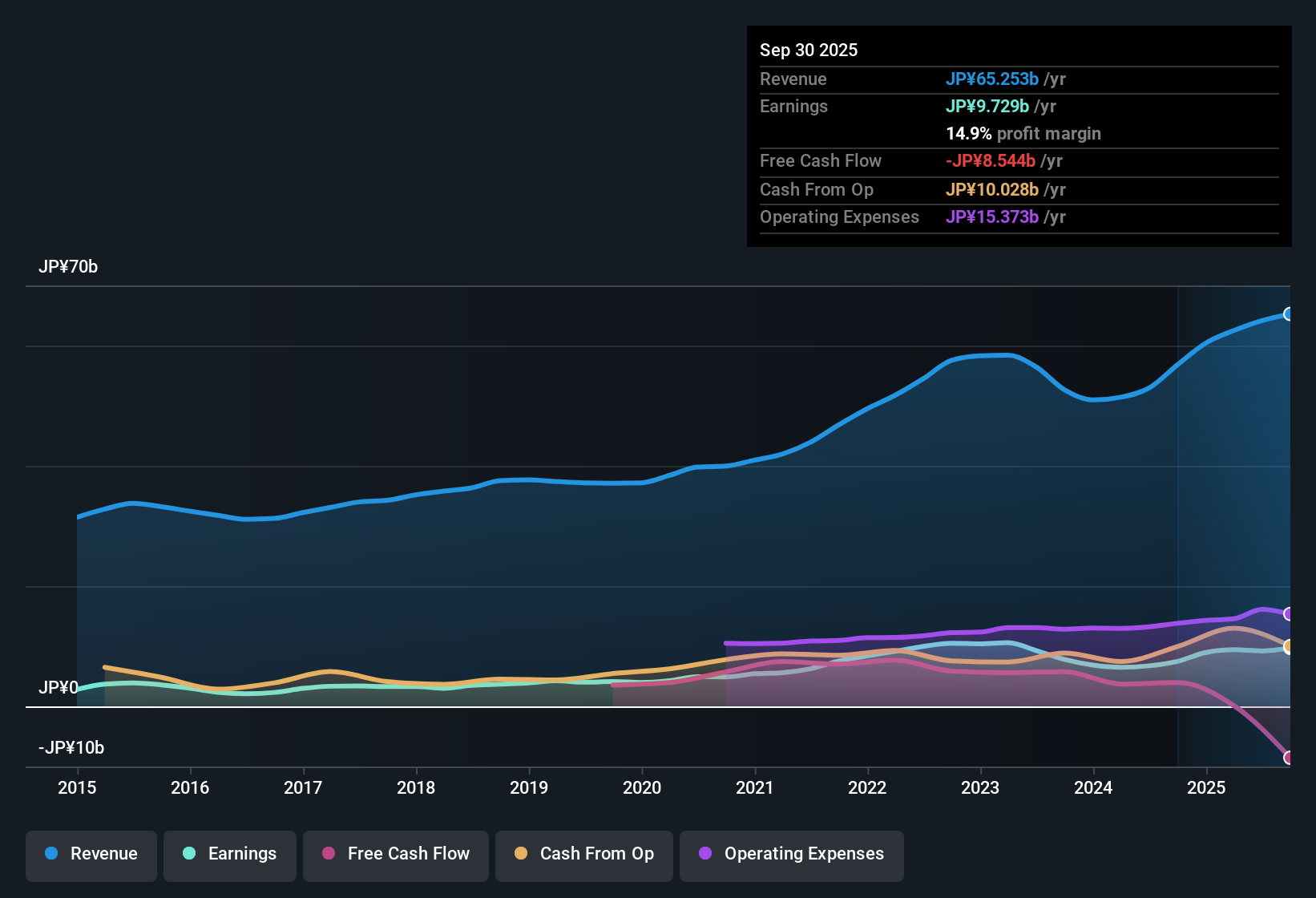

Fujimi has an accrual ratio of 0.36 for the year to September 2025. Statistically speaking, that's a real negative for future earnings. And indeed, during the period the company didn't produce any free cash flow whatsoever. Over the last year it actually had negative free cash flow of JP¥8.5b, in contrast to the aforementioned profit of JP¥9.73b. It's worth noting that Fujimi generated positive FCF of JP¥4.0b a year ago, so at least they've done it in the past.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Fujimi's Profit Performance

As we discussed above, we think Fujimi's earnings were not supported by free cash flow, which might concern some investors. For this reason, we think that Fujimi's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. The good news is that, its earnings per share increased by 30% in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So while earnings quality is important, it's equally important to consider the risks facing Fujimi at this point in time. To help with this, we've discovered 2 warning signs (1 is a bit unpleasant!) that you ought to be aware of before buying any shares in Fujimi.

Today we've zoomed in on a single data point to better understand the nature of Fujimi's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5384

Fujimi

Manufactures and sells synthetic precision abrasives in Japan, North America, Asia, and Europe.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor