Advertisement

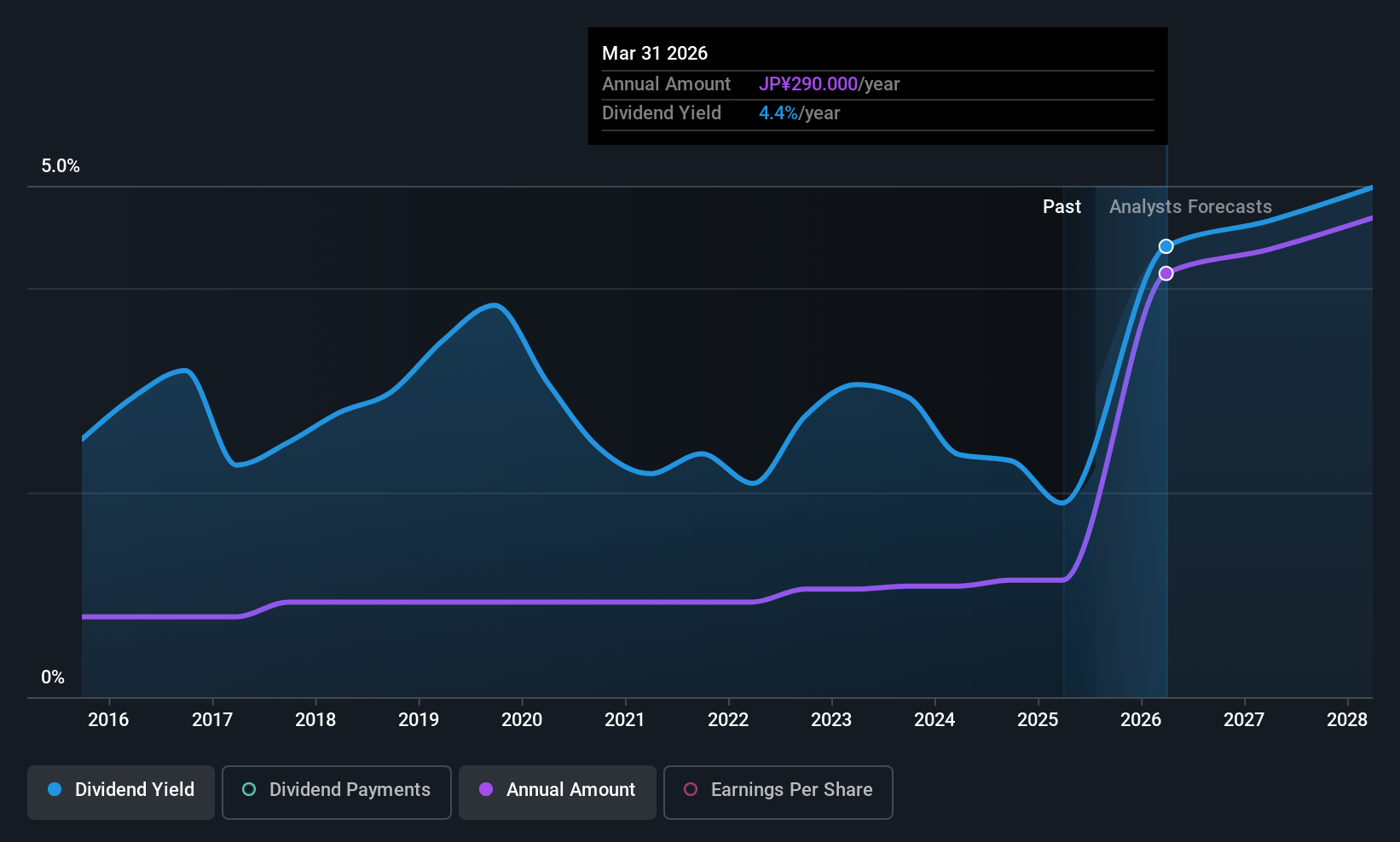

The board of Taiyo Holdings Co., Ltd. (TSE:4626) has announced that it will pay a dividend on the 2nd of December, with investors receiving ¥145.00 per share. This takes the dividend yield to 4.4%, which shareholders will be pleased with.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Taiyo Holdings' stock price has increased by 41% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Estimates Indicate Taiyo Holdings' Could Struggle to Maintain Dividend Payments In The Future

If the payments aren't sustainable, a high yield for a few years won't matter that much. Based on the last payment, the company wasn't making enough to cover what it was paying to shareholders. This situation certainly isn't ideal, and could place significant strain on the balance sheet if it continues.

Earnings per share is forecast to rise by 16.8% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could reach 138%, which probably can't continue without putting some pressure on the balance sheet.

View our latest analysis for Taiyo Holdings

Taiyo Holdings Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2015, the dividend has gone from ¥45.00 total annually to ¥290.00. This means that it has been growing its distributions at 20% per annum over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Taiyo Holdings Might Find It Hard To Grow Its Dividend

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see that Taiyo Holdings has been growing its earnings per share at 24% a year over the past five years. Although earnings per share is up nicely Taiyo Holdings is paying out 98% of its earnings as dividends, which we feel is borderline unsustainable without extenuating circumstances.

Taiyo Holdings' Dividend Doesn't Look Sustainable

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. Although they have been consistent in the past, we think the payments are a little high to be sustained. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 3 warning signs for Taiyo Holdings (of which 1 is a bit unpleasant!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Taiyo Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4626

Flawless balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor