Advertisement

Kanto Denka Kogyo's (TSE:4047) Upcoming Dividend Will Be Larger Than Last Year's

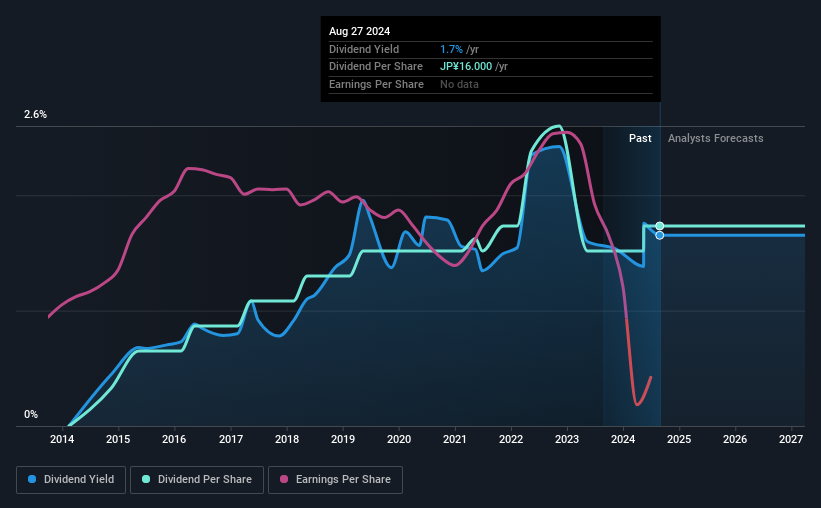

Kanto Denka Kogyo Co., Ltd.'s (TSE:4047) dividend will be increasing from last year's payment of the same period to ¥8.00 on 9th of December. This takes the annual payment to 1.7% of the current stock price, which unfortunately is below what the industry is paying.

View our latest analysis for Kanto Denka Kogyo

Kanto Denka Kogyo's Distributions May Be Difficult To Sustain

Even a low dividend yield can be attractive if it is sustained for years on end. Kanto Denka Kogyo isn't generating any profits, and it is paying out a very high proportion of the cash it is earning. These payout levels would generally be quite difficult to keep up.

Looking forward, earnings per share is forecast to rise by 70.8% over the next year. This is the right direction to be moving, but it is not enough to achieve profitability. Unfortunately, for the dividend to continue at current levels the company definitely needs to get there sooner rather than later.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2014, the dividend has gone from ¥3.00 total annually to ¥16.00. This works out to be a compound annual growth rate (CAGR) of approximately 18% a year over that time. Kanto Denka Kogyo has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Has Limited Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Earnings per share has been sinking by 11% over the last five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

We're Not Big Fans Of Kanto Denka Kogyo's Dividend

In conclusion, we have some concerns about this dividend, even though it being raised is good. The company isn't making enough to be paying as much as it is, and the other factors don't look particularly promising either. The dividend doesn't inspire confidence that it will provide solid income in the future.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Are management backing themselves to deliver performance? Check their shareholdings in Kanto Denka Kogyo in our latest insider ownership analysis. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Kanto Denka Kogyo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4047

Kanto Denka Kogyo

Manufactures and sells various chemical products in Japan and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor