Advertisement

Rengo (TSE:3941) Valuation in Focus After Dividend Increases and Revised Earnings Guidance

Simply Wall St

Reviewed by Simply Wall St

Rengo (TSE:3941) made waves with its Board of Directors voting to increase interim and year-end dividend targets, and releasing updated earnings guidance for the coming year. These moves reflect management's confidence and focus on delivering value to shareholders.

See our latest analysis for Rengo.

Shares of Rengo have moved steadily higher in recent months, with a 9.2% share price return over the past month and an 11.1% gain in the last quarter, which hints at renewed momentum. Long-term investors have also been rewarded, as the stock has delivered a 16.3% total shareholder return over the past year and an impressive 39.5% total return over five years. This signals a solid track record as management signals more confidence.

If you’re looking for more investing ideas beyond the latest dividend updates, now’s a prime opportunity to discover fast growing stocks with high insider ownership.

With the stock’s solid performance and management committing to higher dividends, the key question now is whether Rengo shares remain undervalued or if the market has already priced in the company’s improving outlook and future growth prospects.

Price-to-Earnings of 11.8x: Is it justified?

Rengo currently trades at a price-to-earnings (P/E) ratio of 11.8x, noticeably above both the Japanese Packaging industry average of 9.4x and the peer average of 10.7x. This suggests that investors are paying a higher price for Rengo’s earnings compared to similar companies in its sector.

The P/E ratio reflects what shareholders are willing to pay for each yen of earnings, providing insight into market expectations for future profitability. In sectors with limited high-growth prospects, a premium multiple can sometimes indicate confidence in a company’s earnings stability or its leadership in the market.

Despite the higher multiple, Rengo’s profit margins have slipped compared to last year and earnings have actually declined over the past five years. The current premium may reflect optimism about management’s recent strategic updates. However, it raises questions as to whether future growth will justify the higher price. Relative to the estimated fair P/E of 16.1x, the market could still move higher if profit growth accelerates to match expectations.

Explore the SWS fair ratio for Rengo

Result: Price-to-Earnings of 11.8x (OVERVALUED)

However, slower revenue growth or a decline in annual net income could present challenges to the current optimism surrounding Rengo’s valuation and outlook.

Find out about the key risks to this Rengo narrative.

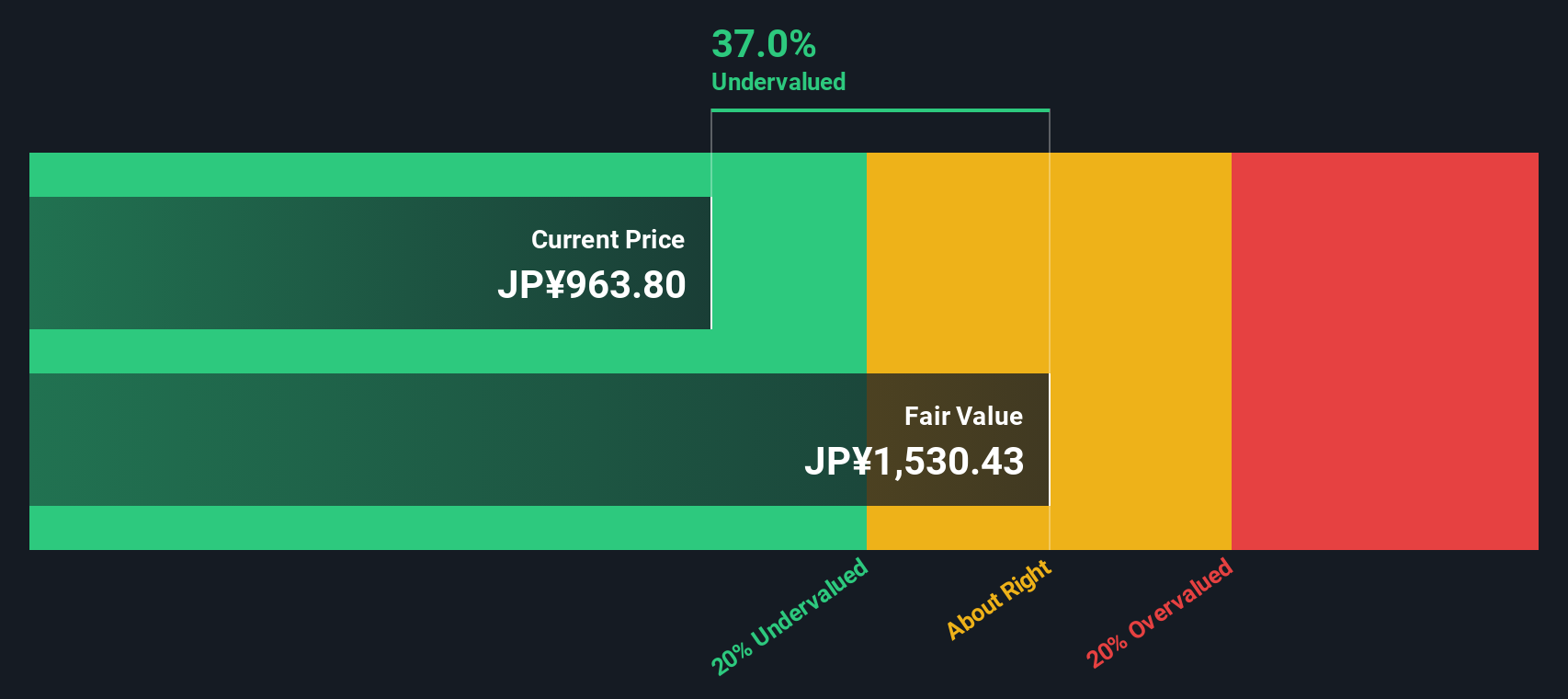

Another View: Discounted Cash Flow Says Undervalued

Looking from a different angle, our DCF model puts Rengo’s fair value at ¥1,565.29 per share, which is well above its current price of ¥1,003. This suggests the stock could be undervalued and challenges the message from its higher price-to-earnings ratio. Which approach will prove right as new results come in?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Rengo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 895 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Rengo Narrative

If you want to challenge these conclusions or would rather shape your own perspective, you can craft your narrative in just a few minutes. Do it your way.

A great starting point for your Rengo research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Seize your chance to get ahead of the market by finding standout opportunities in sectors most investors overlook using the powerful Simply Wall Street Screener today.

- Capture growth trends by tracking these 27 AI penny stocks at the forefront of artificial intelligence innovation and real-world adoption.

- Boost your portfolio's income potential by uncovering these 18 dividend stocks with yields > 3% currently delivering robust yields and reliable payments.

- Position yourself early in transformative industries by targeting these 26 quantum computing stocks, where breakthroughs could spark the next wave of tech growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3941

Rengo

Manufactures and sells paperboard and packaging-related products in Asia, Europe, and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor