KOSÉ (TSE:4922) shares have seen some interesting price moves over the past month, up around 5%. Investors are weighing the company’s recent performance as they look for hints about where the stock might be headed.

While KOSÉ’s 5% gain over the past month is grabbing attention, it comes after a challenging year for investors, as the 1-year total shareholder return remains deep in negative territory. Even with a bump in short-term momentum, the longer-term performance suggests there are still questions around growth potential and market confidence.

The key question now is whether KOSÉ shares are attractively undervalued given recent declines, or if the current price already reflects expectations of a turnaround and leaves little room for upside ahead.

Advertisement

Price-to-Earnings of 116.6x: Is it justified?

KOSÉ trades at a price-to-earnings (P/E) ratio of 116.6x, significantly higher than its peers and industry averages. With the last close at ¥6,123, this premium pricing raises questions about whether the market is overestimating its future growth or simply optimistic for a sharp turnaround.

The price-to-earnings ratio measures how much investors are willing to pay for each yen of the company’s earnings. In the personal products sector, P/E is closely watched because it reflects both current profitability and what investors expect for the future. At this level, the market appears to be anticipating a dramatic recovery in earnings. Such a high figure leaves little room for disappointment without a reset in expectations.

Compared to the industry average of 24.1x and a peer average of 29.5x, KOSÉ is trading at a striking premium. Even measured against the estimated fair P/E ratio of 29x, the company still appears substantially overvalued based on earnings multiples alone. If the market moves toward the sector or fair multiple, the stock could face valuation pressure ahead.

However, slowing revenue growth and a disappointing long-term total return could pose real risks if earnings momentum does not pick up meaningfully from this point.

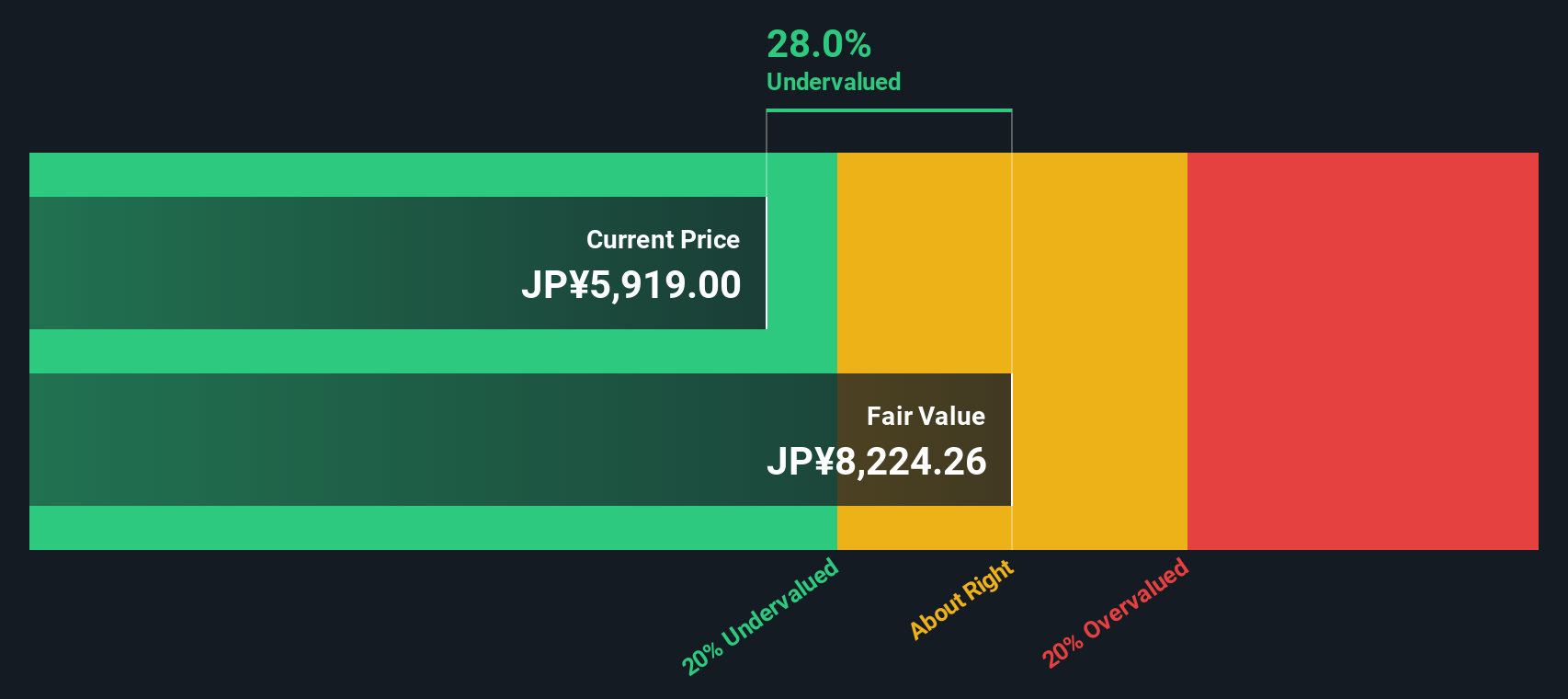

While the current P/E ratio highlights a steep valuation, our SWS DCF model presents a very different perspective. Based on estimated future cash flows, KOSÉ appears to be trading about 25% below its fair value. This suggests the market might be underpricing its potential. Could forward-looking optimism outweigh the risks in the near term?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out KOSÉ for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own KOSÉ Narrative

If you see the story differently or want to investigate further, you can dive into the numbers yourself and shape your own view in just a few minutes with Do it your way.

Smart investors never limit themselves. Make your next move by finding hidden opportunities that could give your portfolio a serious edge. These screens are handpicked for standout potential.

Catch the next innovation wave and seize growth potential by targeting these 24 AI penny stocks at the forefront of artificial intelligence advancements.

Capitalize on breakthrough technologies set to transform industries through these 26 quantum computing stocks with unique positions in the quantum computing race.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KOSÉ might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.