KOSÉ (TSE:4922) shares have moved recently, drawing interest from market watchers curious about what could be driving the action. Investors may be weighing the company’s current valuation in relation to its recent performance trends.

KOSÉ’s share price has been under pressure this year, down over 15% year-to-date and showing a one-year total shareholder return of -27.8%. While the pace of declines has slowed in recent months, market sentiment still seems to be weighed down by concerns about longer-term growth and a more cautious outlook from investors.

The question for investors now is whether KOSÉ’s current valuation truly reflects its recent struggles and future prospects, or if the market is overlooking a potential turnaround. Could this spell an attractive entry point for buyers?

Advertisement

Price-to-Earnings of 111.6x: Is it justified?

With KOSÉ trading at a price-to-earnings (P/E) ratio of 111.6x based on the last close price of ¥5,858, the stock stands notably above both peer and industry averages. This high multiple signals the market has priced in aggressive expectations despite recent share price weakness.

The P/E ratio reflects how much investors are willing to pay today for ¥1 of current earnings. In the personal products sector, this measure is crucial for comparing perceived growth potential and profitability across similar businesses. Normally, a much higher P/E suggests investors are betting on a significant rebound in earnings or sustained outperformance that current numbers do not fully reflect.

Compared to the average P/E of 28.5x for peers and 23x for the broader Japanese personal products industry, KOSÉ’s multiple appears excessive. The fair price-to-earnings ratio, as estimated, is 29x. The market could potentially recalibrate toward this level if current momentum or growth projections are not realized. Such a sharp premium demands extraordinary future performance or a meaningful shift in sentiment to be justified.

Another View: Is the Discounted Cash Flow Telling a Different Story?

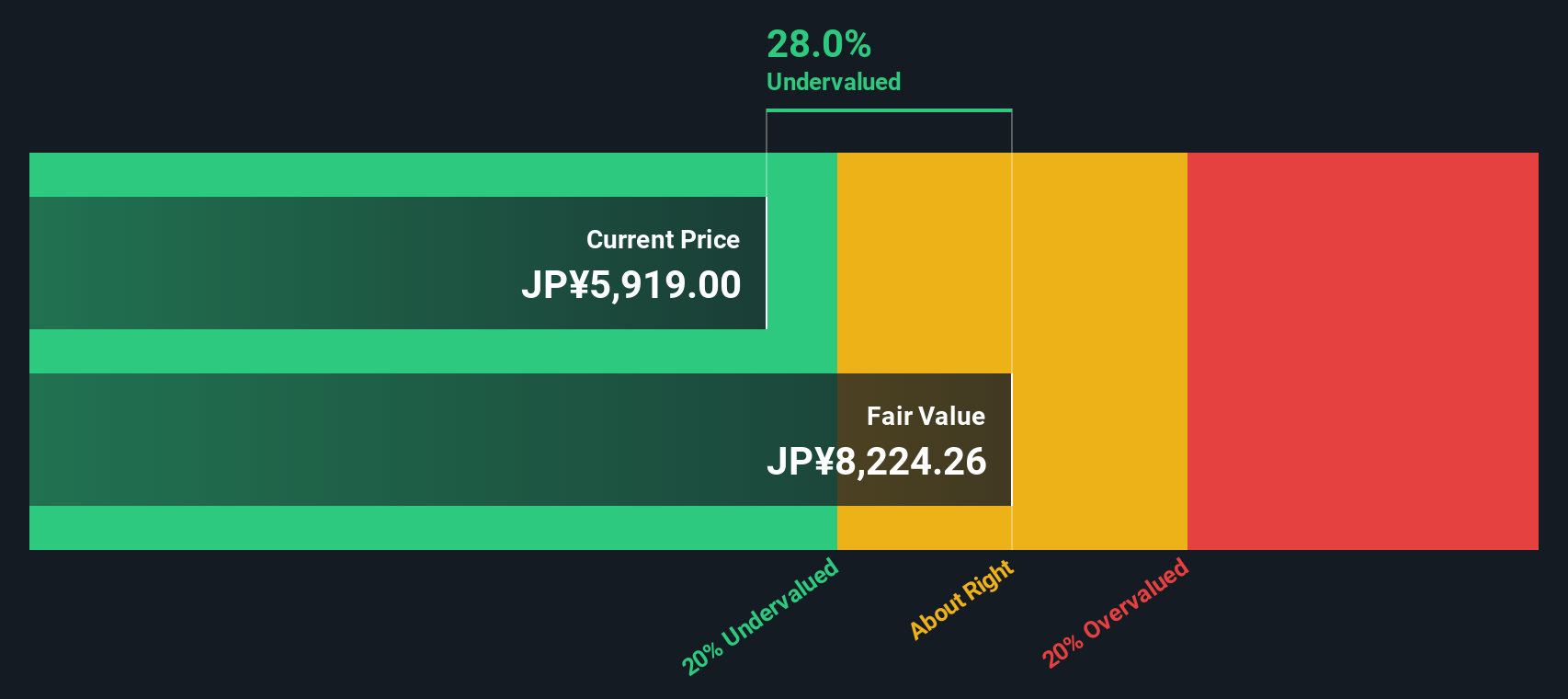

While the current market valuation looks steep based on earnings multiples, our DCF model takes a different approach. It estimates KOSÉ’s fair value at ¥8,211.45, which is around 28.7% above today’s share price. Could the market be underestimating long-term earnings power?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out KOSÉ for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own KOSÉ Narrative

If you see things differently or want to dig into the details yourself, you can quickly craft your own perspective in just a few minutes with Do it your way.

Don’t let powerful opportunities pass you by, especially when there are smart ways to target growth and income the market might be overlooking right now. Use these dynamic screens to supercharge your investing strategy today.

Unlock the next wave of innovation by tapping into the potential of these 26 AI penny stocks, which are reshaping entire industries with artificial intelligence breakthroughs.

Capture reliable income streams when you tap into these 21 dividend stocks with yields > 3%, offering yields above 3% and a strong track record of rewarding shareholders.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KOSÉ might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.