- Japan

- /

- Wireless Telecom

- /

- TSE:9434

Olympus (TSE:7733) Boosts Shareholder Value with Buyback and Dividend Increase, Faces Growth Challenges

Reviewed by Simply Wall St

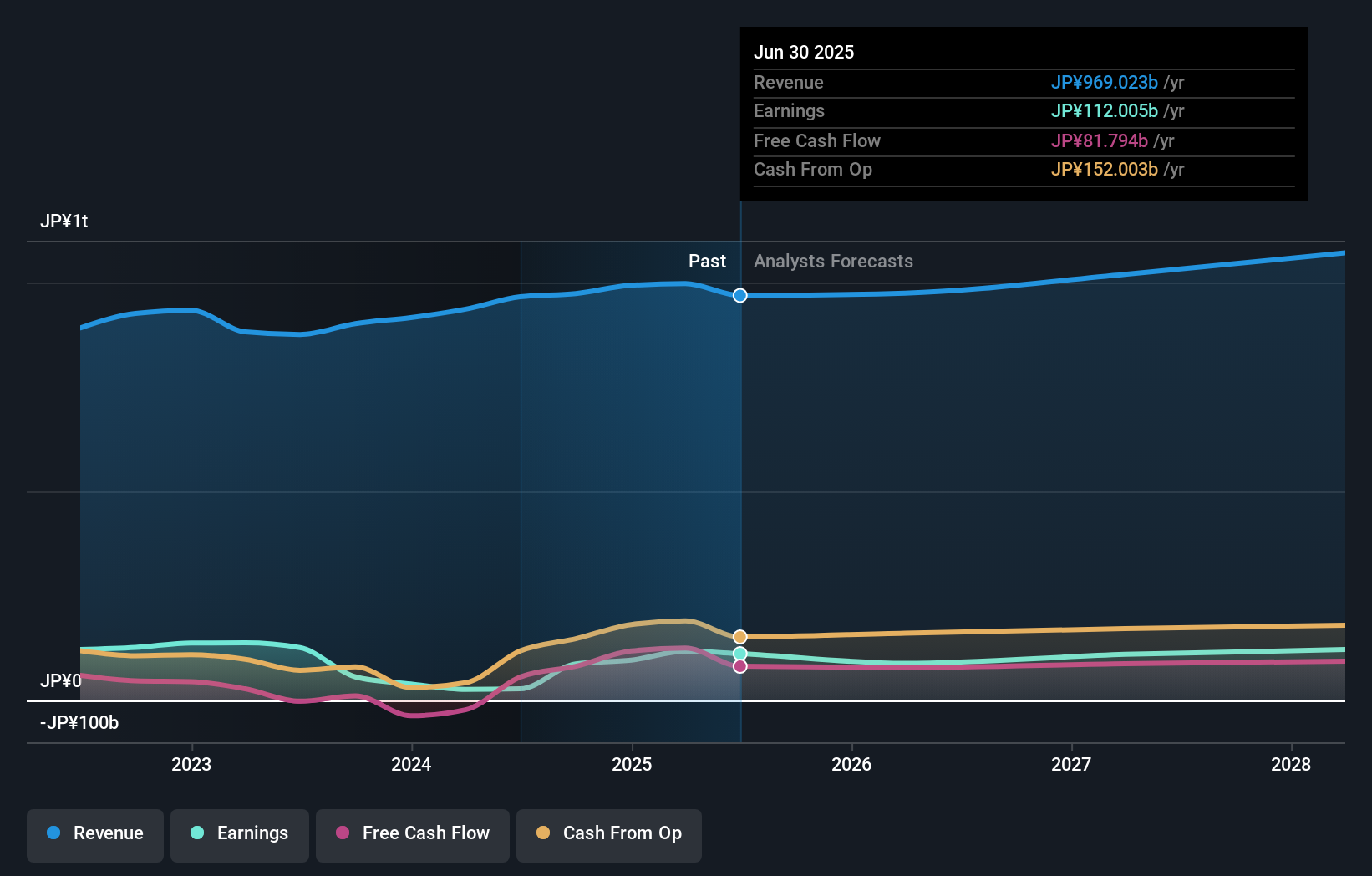

Olympus (TSE:7733) is making strategic moves to enhance shareholder value, evidenced by its recent buyback of 22,373,500 shares for ¥56.46 billion. Challenges like a significant drop in earnings and a high P/E ratio persist, yet Olympus is poised for growth with its strong financial health and exploration of new markets in Asia and Europe. Readers should expect a detailed analysis of how Olympus plans to leverage its competitive advantages while addressing potential constraints and market volatility.

Click here to discover the nuances of Olympus with our detailed analytical report.

Competitive Advantages That Elevate Olympus

Olympus demonstrates strong financial health with earnings projected to grow at an impressive 24.1% annually, outpacing the broader JP market's revenue growth of 5.1% compared to 4.2%. The company's cash position exceeds its total debt, and an interest coverage ratio of 19.5x underscores its financial stability. The recent share buyback of 22,373,500 shares, representing 1.92% of outstanding shares for ¥56.46 billion, reflects management's commitment to enhancing shareholder value. Furthermore, the board's average tenure of 3.3 years suggests seasoned leadership that can effectively guide strategic initiatives. This is complemented by strategic alliances and product innovations, as highlighted by CEO Stefan Kaufmann, which have received positive customer feedback and contributed to a high retention rate.

Challenges Constraining Olympus's Potential

However, Olympus faces significant challenges, including a 77.9% drop in earnings over the past year and a low return on equity of 3.6%. These figures highlight areas of concern, particularly when current net profit margins have decreased to 2.9% from 14.4% the previous year. The management team's relatively short average tenure of 1.5 years may contribute to these issues, potentially impacting strategic continuity. Additionally, the company's current share price of ¥2815, trading above the estimated fair value of ¥2508.03, coupled with a high Price-To-Earnings Ratio of 115.4x, raises concerns about its valuation compared to industry peers.

Emerging Markets Or Trends for Olympus

Opportunities for Olympus are abundant, with high expected annual profit growth indicating potential for increased profitability. The company's exploration of new markets in Asia and Europe, as mentioned by Stefan Kaufmann, CEO, could significantly boost growth. The rising demand for sustainable products presents another avenue for expansion, aligning with global market trends. Strategic partnerships, such as the recent collaboration with a leading tech firm, are poised to enhance product offerings and market reach, positioning Olympus to capitalize on these emerging opportunities.

Market Volatility Affecting Olympus's Position

Nevertheless, Olympus must navigate several threats, including its high valuation, which could deter potential investors. The presence of large one-off items in financial results poses a risk to future stability. Additionally, the competitive environment is rapidly evolving, with increased pressure on pricing strategies, as noted by COO Izumi Tatsuya. Economic uncertainties and potential regulatory changes could further impact consumer spending and operational dynamics. These external factors necessitate vigilant risk management to maintain market share and ensure long-term growth.

To gain deeper insights into Olympus's historical performance, explore our detailed analysis of past performance. To dive deeper into how Olympus's valuation metrics are shaping its market position, check out our detailed analysis of Olympus's Valuation.Conclusion

Olympus's financial health is underscored by its strong cash position and projected earnings growth of 24.1% annually, which positions the company to outpace the broader JP market. However, the challenges of a significant earnings drop and low return on equity indicate areas that require strategic attention, particularly as the company's current share price of ¥2815 exceeds its estimated fair value of ¥2508.03, suggesting potential investor hesitance due to its high Price-To-Earnings Ratio of 115.4x. Despite these hurdles, Olympus's exploration of new markets and strategic partnerships present substantial growth opportunities, although the company must carefully manage external threats such as economic uncertainties and competitive pressures to ensure sustained profitability and market share. The seasoned leadership and strategic initiatives are vital for navigating these challenges and leveraging emerging trends for future success.

Turning Ideas Into Actions

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSE:9434

SoftBank

Engages in the telecommunication and information technology businesses in Japan.

Good value with adequate balance sheet and pays a dividend.