- Japan

- /

- Professional Services

- /

- TSE:6532

3 Japanese Growth Companies With High Insider Ownership And 41% ROE

Reviewed by Simply Wall St

Japan's stock markets have shown mixed performance recently, with the Nikkei 225 Index gaining 0.5% while the broader TOPIX Index declined by 1.0%. Amid this backdrop of fluctuating indices and a strengthening yen, growth companies with high insider ownership can offer unique investment opportunities. In today's market conditions, identifying stocks that combine strong growth potential with significant insider ownership can be particularly appealing. Here are three Japanese growth companies that not only exhibit robust financial metrics but also boast high levels of insider ownership and an impressive return on equity (ROE) of 41%.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 32.7% |

| Hottolink (TSE:3680) | 27% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 43.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| AeroEdge (TSE:7409) | 10.7% | 25.3% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

Here's a peek at a few of the choices from the screener.

Medley (TSE:4480)

Simply Wall St Growth Rating: ★★★★★★

Overview: Medley, Inc. operates platforms for recruitment and medical businesses in Japan and the United States, with a market cap of ¥107.36 billion.

Operations: Revenue segments include ¥5.67 billion from New Services, ¥6.09 billion from the Medical Platform Business, and ¥17.87 billion from the Human Resource Platform Business.

Insider Ownership: 34%

Return On Equity Forecast: 24% (2027 estimate)

Medley, a growth company with high insider ownership in Japan, is forecast to see its earnings grow significantly at 30.36% per year, outpacing the JP market's 8.7%. Despite recent share price volatility, Medley trades at 57.7% below its estimated fair value and boasts a strong return on equity forecast of 24.4%. Recent expansion efforts in the U.S., particularly through Jobley’s service rollout to 39 states and D.C., highlight promising growth prospects amidst healthcare hiring challenges.

- Click here to discover the nuances of Medley with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Medley is trading behind its estimated value.

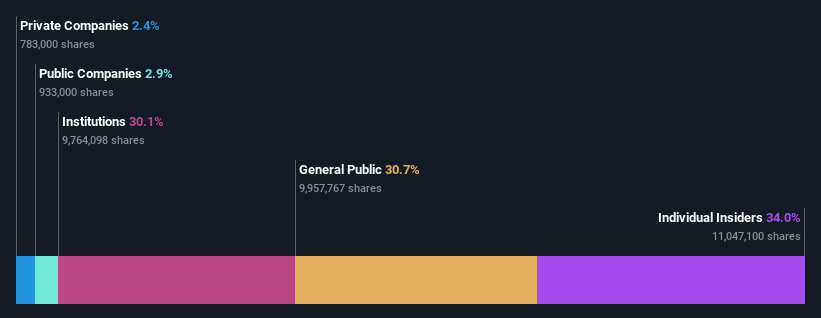

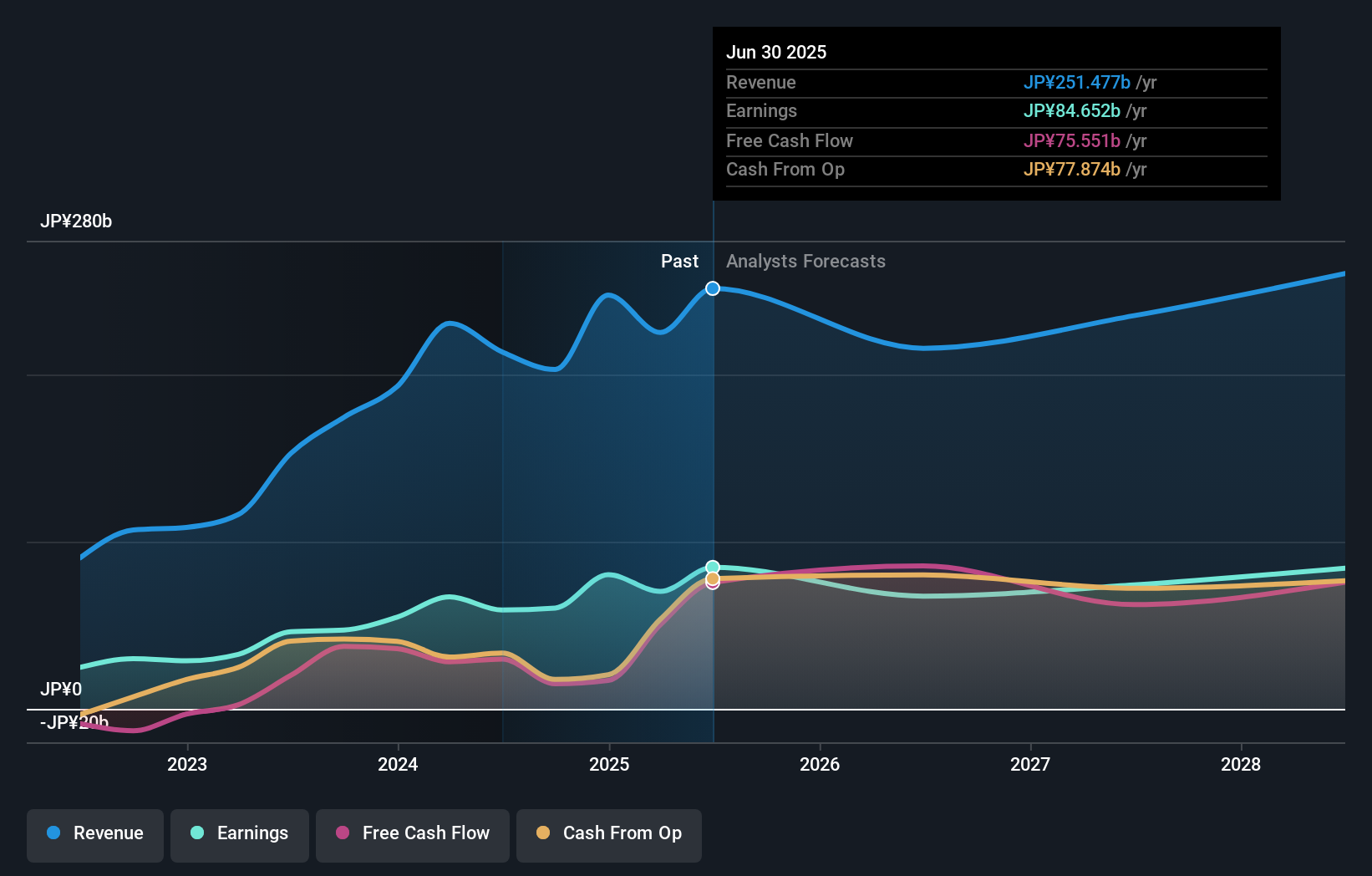

BayCurrent Consulting (TSE:6532)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc. provides consulting services in Japan and has a market cap of ¥778.18 billion.

Operations: BayCurrent Consulting, Inc. generates revenue from consulting services in Japan amounting to ¥null million.

Insider Ownership: 13.9%

Return On Equity Forecast: 35% (2027 estimate)

BayCurrent Consulting, with high insider ownership, is forecast to grow its revenue at 18.6% per year, outpacing the JP market's 4.3%. Earnings are expected to increase by 18.8% annually, faster than the market's 8.7%. Despite trading at 46% below its estimated fair value and a strong return on equity forecast of 35.5%, recent earnings growth of 16.8% suggests solid performance potential in Japan’s consulting sector without significant insider trading activity recently reported.

- Click to explore a detailed breakdown of our findings in BayCurrent Consulting's earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of BayCurrent Consulting shares in the market.

Lasertec (TSE:6920)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Lasertec Corporation designs, manufactures, and sells inspection and measurement equipment both in Japan and internationally with a market cap of ¥2.01 trillion.

Operations: The company's revenue segment, amounting to ¥213.51 billion, is derived from the design, manufacture, and sale of inspection and measurement equipment in Japan and internationally.

Insider Ownership: 11.8%

Return On Equity Forecast: 42% (2027 estimate)

Lasertec, with significant insider ownership, is forecast to grow earnings by 20.1% annually, outpacing the JP market's 8.7%. Despite a highly volatile share price recently, its return on equity is projected to reach 41.8% in three years. Revenue growth of 16.7% per year will also surpass the market average of 4.3%. Recent board resignations and updated dividend guidance reflect ongoing corporate changes while maintaining robust financial performance expectations for FY2025 with net sales of ¥240 billion ($1.63 billion).

- Navigate through the intricacies of Lasertec with our comprehensive analyst estimates report here.

- The analysis detailed in our Lasertec valuation report hints at an inflated share price compared to its estimated value.

Next Steps

- Dive into all 93 of the Fast Growing Japanese Companies With High Insider Ownership we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if BayCurrent Consulting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6532

Flawless balance sheet with reasonable growth potential.