Advertisement

Morinaga (TSE:2201): Valuation Insight Following Earnings Forecast Upgrade and New Interim Dividend Announcement

Simply Wall St

Reviewed by Simply Wall St

Morinaga&Co (TSE:2201) has just updated its earnings outlook, pointing to stronger profitability even with some challenges in specific business segments and higher costs. The company also introduced a new interim dividend to boost shareholder returns and signal confidence in ongoing earnings stability.

See our latest analysis for Morinaga&Co.

Morinaga&Co.'s share price has seen a modest decline of 4.8% so far this year, but steady mid-single-digit total shareholder returns over the past twelve months, and an impressive 52.6% three-year total return, point to a resilient long-term track record. Management’s recent guidance update and interim dividend move have helped to shore up sentiment, suggesting the company is focused on building momentum even as near-term price performance remains subdued.

If you’re looking to spot the next wave of opportunity in the market, it’s a great moment to explore fast growing stocks with high insider ownership.

With shares still trading at a discount to analyst price targets and the company’s profitability outpacing expectations, investors are left to ponder whether Morinaga&Co is undervalued or if the market has already priced in its future growth.

Price-to-Earnings of 12x: Is it justified?

Morinaga&Co’s current price-to-earnings (P/E) ratio sits at 12x, which looks attractive when matched against both peers and industry benchmarks. With the last close at ¥2,586, this multiple suggests the market is attributing relatively modest expectations to the company’s future earnings despite recent growth.

The P/E ratio reflects how much investors are willing to pay for each yen of earnings, giving a quick snapshot of sentiment around profitability and growth potential. In the context of the food sector, where earnings are generally steady but not explosive, a lower P/E can also highlight overlooked opportunities when growth is quietly robust.

Morinaga&Co’s P/E ratio is substantially lower than both its peer average of 14.7x and the broader JP Food industry average of 16.5x. Even more convincingly, it sits well below the estimated “fair” P/E ratio of 15.6x that might be expected for companies with similar profiles. This signals a possible gap for re-rating if earnings growth persists and confidence builds in management’s execution.

Explore the SWS fair ratio for Morinaga&Co

Result: Price-to-Earnings of 12x (UNDERVALUED)

However, persistent sector volatility and unexpected cost pressures could limit upside. This challenges the case for a swift market re-rating despite attractive valuations.

Find out about the key risks to this Morinaga&Co narrative.

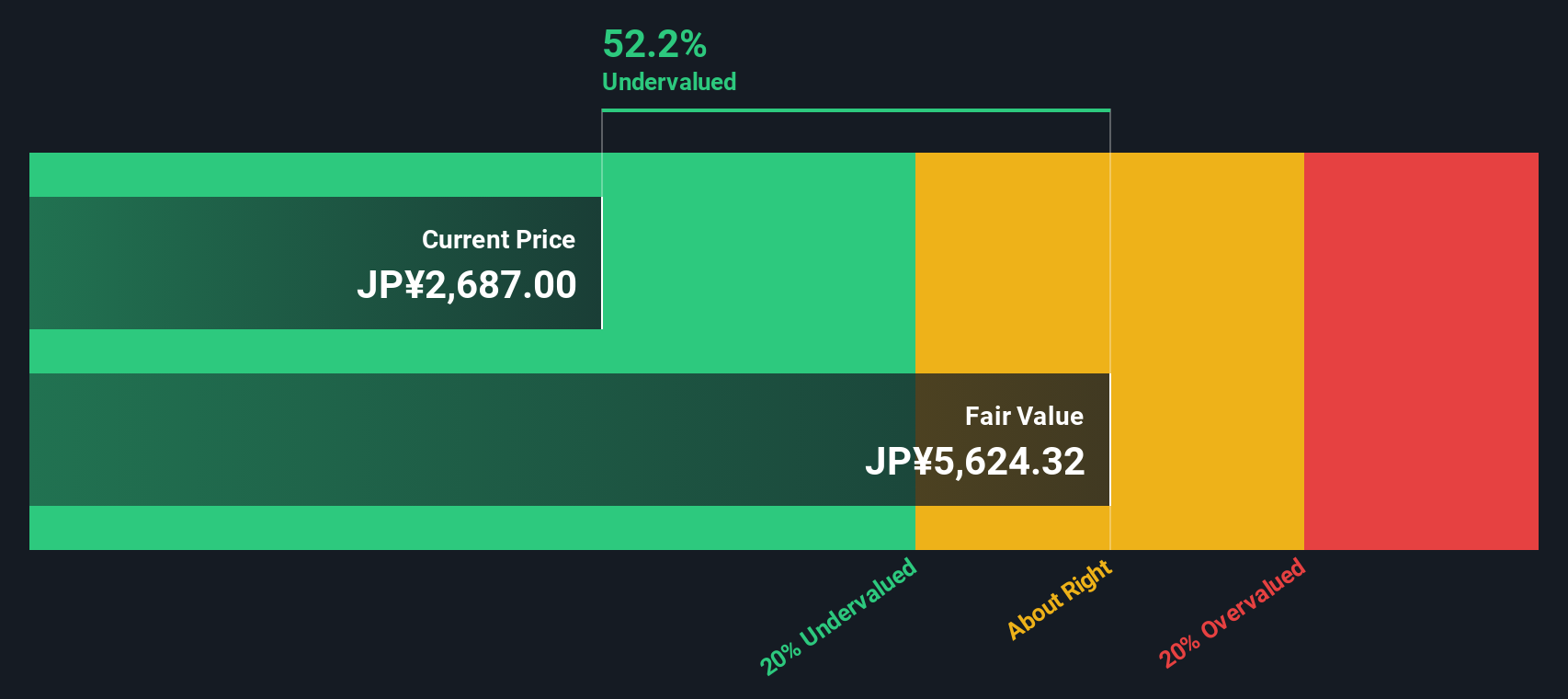

Another View: Discounted Cash Flow Tells a Bigger Story

Looking at Morinaga&Co through the lens of our DCF model, the potential undervaluation appears even greater. While market multiples look modest, the SWS DCF model estimates fair value at ¥5,600.74. This puts the current price at a significant 53.8% discount. Could the market be missing something?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Morinaga&Co for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Morinaga&Co Narrative

If you’d rather form your own perspective or dig deeper into the numbers, you can shape your own narrative in just a few minutes. Do it your way.

A great starting point for your Morinaga&Co research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors are always one step ahead. Uncover new opportunities and gain an edge by using the Simply Wall Street Screener to spot high-potential stocks you might be missing out on.

- Unleash the power of next-generation artificial intelligence by checking out these 25 AI penny stocks, which are reshaping entire industries with smart innovation.

- Seize the advantage in emerging technologies when you research these 26 quantum computing stocks, companies riding the quantum wave with breakthroughs in computing speed and security.

- Supercharge your returns by uncovering income opportunities through these 16 dividend stocks with yields > 3%, which offer reliable yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2201

Morinaga&Co

Manufactures, purchases, and sells confectionaries, food, frozen desserts, and health products in Japan and internationally.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor