Advertisement

As global markets navigate a landscape marked by fluctuating corporate earnings and geopolitical tensions, small-cap stocks have experienced mixed performance amid broader economic shifts. The S&P 600, representing small-cap companies, has reflected this volatility, influenced by factors such as AI competition fears and monetary policy decisions. In this environment, identifying promising stocks often involves looking beyond immediate market reactions to uncover potential long-term value driven by innovation or niche market positioning.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Cresco | 6.62% | 8.15% | 9.94% | ★★★★★★ |

| Eagle Financial Services | 125.65% | 12.07% | 2.64% | ★★★★★★ |

| Ningbo United GroupLtd | 11.97% | -19.47% | -30.66% | ★★★★★★ |

| NOROO PAINT & COATINGS | 12.38% | 4.96% | 8.97% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Industrias del Cobre Sociedad Anónima | NA | 19.08% | 22.33% | ★★★★★★ |

| Zhejiang Chinastars New Materials Group | 36.20% | 2.98% | 3.98% | ★★★★★☆ |

| Guangdong Kingstrong Technology | 3.20% | 18.82% | 39.73% | ★★★★★☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

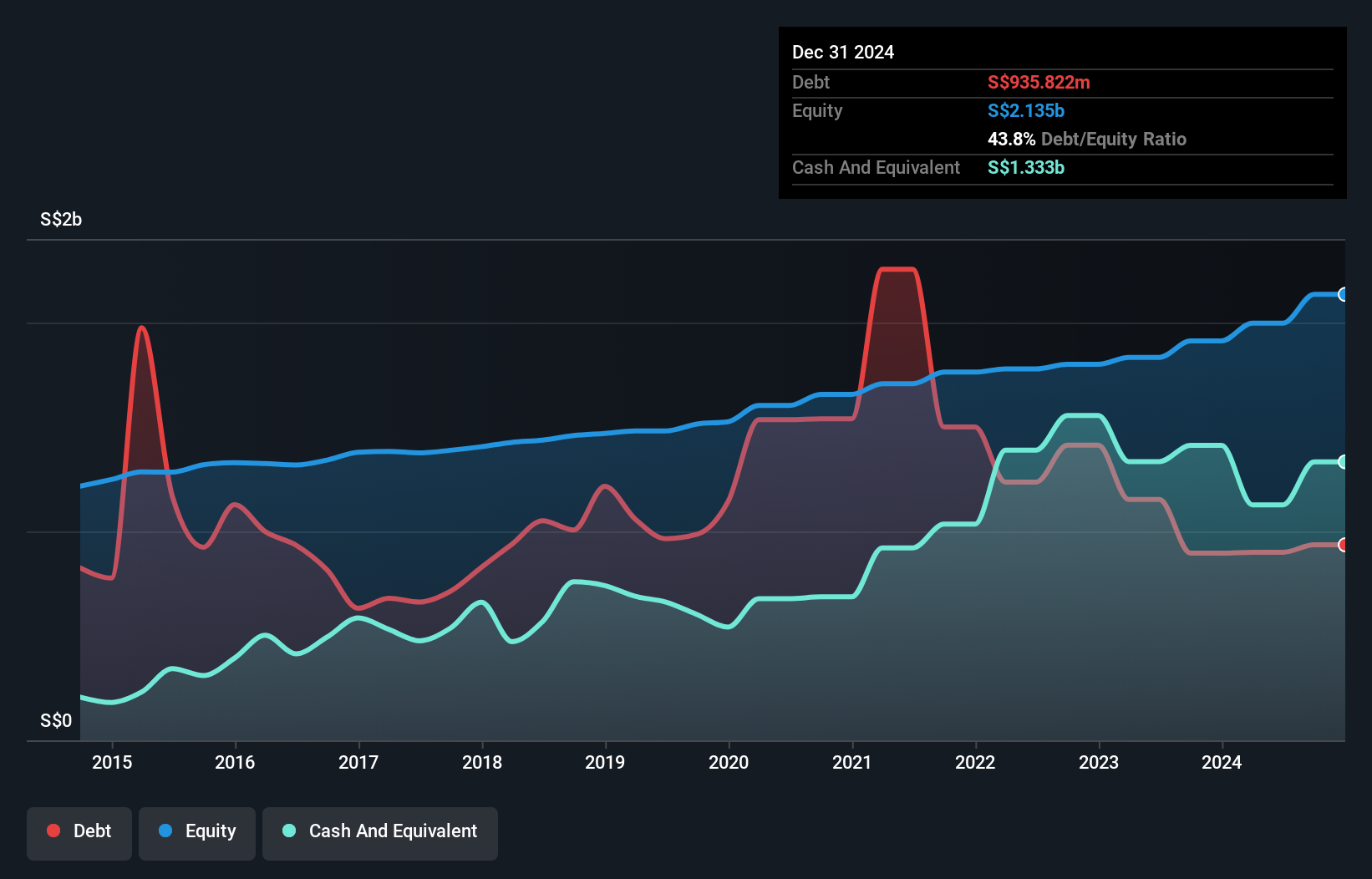

UOB-Kay Hian Holdings (SGX:U10)

Simply Wall St Value Rating: ★★★★☆☆

Overview: UOB-Kay Hian Holdings Limited is an investment holding company offering stockbroking, futures broking, structured lending, investment trading, margin financing, and research services across Singapore, Hong Kong, Thailand, Malaysia, and internationally with a market cap of SGD1.62 billion.

Operations: The primary revenue stream for UOB-Kay Hian Holdings is derived from securities and futures broking and related services, generating SGD581.07 million. The company's net profit margin reflects its efficiency in managing costs relative to its revenue.

UOB-Kay Hian Holdings, a financial player with high-quality earnings, is trading 19.3% below its estimated fair value. Over the past year, its earnings grew by 80%, outpacing the Capital Markets industry's 20.6%. The company has more cash than total debt, reducing its debt-to-equity ratio from 65.2% to 45.1% over five years. Recent strategic moves include establishing UOB Kay Hian Investment Management in Hong Kong and reconstituting board committees with new appointments effective January 2025, indicating an active approach to governance and regional expansion in investment management services.

- Get an in-depth perspective on UOB-Kay Hian Holdings' performance by reading our health report here.

Understand UOB-Kay Hian Holdings' track record by examining our Past report.

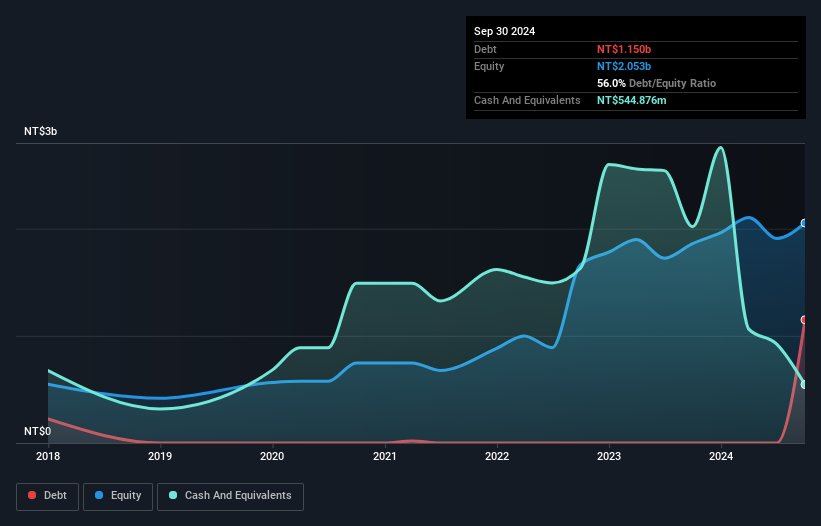

Acer E-Enabling Service Business (TPEX:6811)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Acer E-Enabling Service Business Inc. provides information and communication technology services mainly in Taiwan, with a market capitalization of NT$10.88 billion.

Operations: The company's primary revenue stream is from its Information Software and Application Development Department, generating NT$8.31 billion. The Other business sectors contribute NT$113.38 million to the total revenue.

Acer E-Enabling Service Business seems to be carving a niche with its impressive earnings growth of 10.6% over the past year, outpacing the IT industry’s 9.9%. Despite a highly volatile share price recently, it trades at nearly half of its estimated fair value, suggesting potential undervaluation. The net debt to equity ratio stands at a satisfactory 29.5%, though it has risen from 5.8% over five years, indicating increased leverage. Recent quarterly sales reached TWD 2.18 billion, up from TWD 1.79 billion last year, reflecting robust performance and highlighting Acer's promising trajectory in the market landscape.

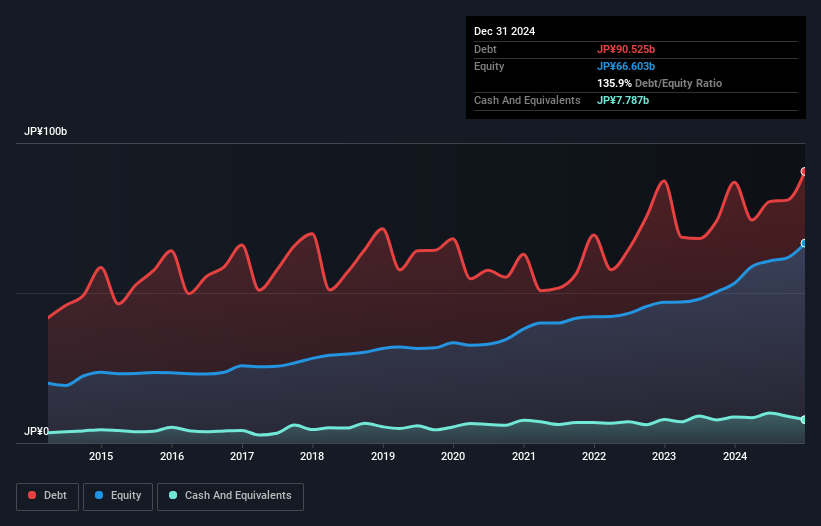

Kyokuyo (TSE:1301)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Kyokuyo Co., Ltd. operates in the marine products, fresh foods, processed food, and logistics sectors both domestically in Japan and internationally, with a market capitalization of approximately ¥49.11 billion.

Operations: Kyokuyo generates revenue primarily from its Marine Products Business, which accounts for ¥168.57 billion, followed by the Food Segment at ¥74.53 billion and Fresh Food Business at ¥71.68 billion. The Logistics Services contribute an additional ¥3 billion to the company's revenue streams.

Kyokuyo's recent half-year results reflect sales of ¥140.57 billion and a net income of ¥2.71 billion, with earnings per share at ¥228.16. The company has shown impressive earnings growth, outpacing the food industry with a 53.9% increase over the past year, highlighting its high-quality earnings profile. Despite facing challenges in covering debt through operating cash flow, Kyokuyo's debt-to-equity ratio has improved from 202% to 131% over five years, indicating better financial positioning. With interest payments well-covered by EBIT at 26.6 times, Kyokuyo seems poised for stability in managing its obligations amidst competitive market conditions.

- Take a closer look at Kyokuyo's potential here in our health report.

Evaluate Kyokuyo's historical performance by accessing our past performance report.

Make It Happen

- Click this link to deep-dive into the 4688 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kyokuyo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1301

Kyokuyo

Engages in the marine products, fresh foods, processed food, and logistics businesses in Japan and internationally.

Good value with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor