Advertisement

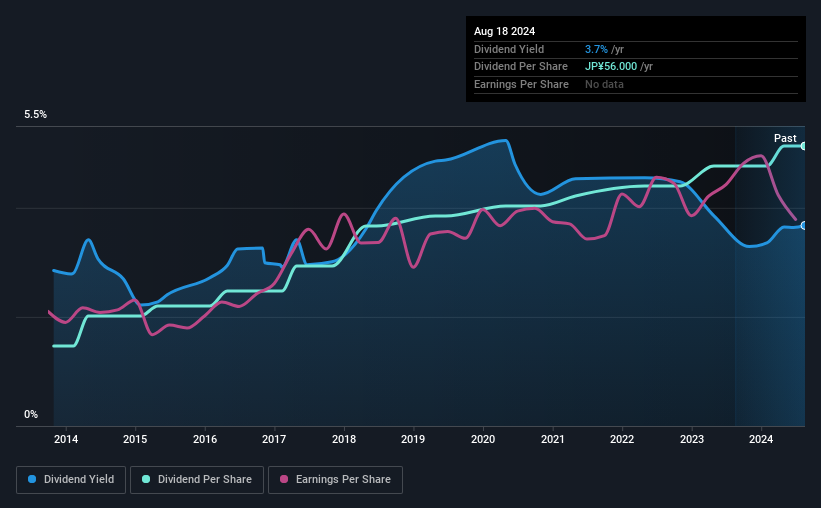

Itochu Enex Co.,Ltd. (TSE:8133) has announced that it will pay a dividend of ¥28.00 per share on the 6th of December. This takes the annual payment to 3.7% of the current stock price, which is about average for the industry.

View our latest analysis for Itochu EnexLtd

Itochu EnexLtd's Payment Has Solid Earnings Coverage

Solid dividend yields are great, but they only really help us if the payment is sustainable. The last dividend was quite easily covered by Itochu EnexLtd's earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Over the next year, EPS could expand by 1.2% if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio will be 55%, which is in the range that makes us comfortable with the sustainability of the dividend.

Itochu EnexLtd Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The annual payment during the last 10 years was ¥16.00 in 2014, and the most recent fiscal year payment was ¥56.00. This works out to be a compound annual growth rate (CAGR) of approximately 13% a year over that time. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

Dividend Growth May Be Hard To Achieve

The company's investors will be pleased to have been receiving dividend income for some time. Although it's important to note that Itochu EnexLtd's earnings per share has basically not grown from where it was five years ago, which could erode the purchasing power of the dividend over time. The company has been growing at a pretty soft 1.2% per annum, and is paying out quite a lot of its earnings to shareholders. While this isn't necessarily a negative, it definitely signals that dividend growth could be constrained in the future unless earnings start to pick up again.

Itochu EnexLtd Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. See if management have their own wealth at stake, by checking insider shareholdings in Itochu EnexLtd stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8133

Itochu EnexLtd

Engages in the sale of petroleum products and liquefied petroleum gas (LPG), electricity, heat supply, vehicle sales in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor