- Japan

- /

- Food and Staples Retail

- /

- TSE:8242

Discovering Japan's Undiscovered Gems October 2024

Reviewed by Simply Wall St

Amidst Japan's recent political shifts and market fluctuations, the Nikkei 225 Index and TOPIX Index have experienced notable declines, reflecting investor reactions to new leadership and monetary policy signals. As these indices navigate through economic uncertainties, discerning investors might find opportunities in lesser-known stocks that show resilience and potential for growth despite broader market challenges. Identifying such gems often involves looking at companies with strong fundamentals, innovative strategies, or niche market positions that can thrive even when larger economic indicators are volatile.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Tokyo Tekko | 10.81% | 7.30% | 7.30% | ★★★★★★ |

| Nihon Parkerizing | 0.31% | 0.86% | 4.40% | ★★★★★★ |

| Central Forest Group | NA | 7.05% | 14.29% | ★★★★★★ |

| Kanda HoldingsLtd | 30.47% | 4.35% | 18.02% | ★★★★★★ |

| Toukei Computer | NA | 5.46% | 12.14% | ★★★★★★ |

| Ohashi Technica | NA | 1.57% | -20.55% | ★★★★★★ |

| Otec | 9.81% | 2.32% | -1.39% | ★★★★★★ |

| NPR-Riken | 15.31% | 10.00% | 44.55% | ★★★★★☆ |

| MIRARTH HOLDINGSInc | 266.33% | 3.00% | -2.40% | ★★★★☆☆ |

| Ogaki Kyoritsu Bank | 139.93% | 2.20% | -0.27% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

SAN-ALTD (TSE:2659)

Simply Wall St Value Rating: ★★★★★★

Overview: SAN-A CO., LTD. operates a chain of supermarkets in Okinawa with a market capitalization of ¥162.04 billion.

Operations: The company generates revenue primarily from its retail segment, amounting to ¥221.26 billion, and a smaller portion from convenience stores at ¥8.39 billion.

SAN-A seems to be a promising player in Japan's retail sector, with earnings growth of 34.4% over the past year, outpacing the industry average of 22.2%. The company is debt-free, a significant shift from five years ago when its debt-to-equity ratio was 0.2%. Trading at 42.6% below its estimated fair value, SAN-A offers potential upside despite reducing dividends to ¥55 per share from ¥110 last year.

- Get an in-depth perspective on SAN-ALTD's performance by reading our health report here.

Understand SAN-ALTD's track record by examining our Past report.

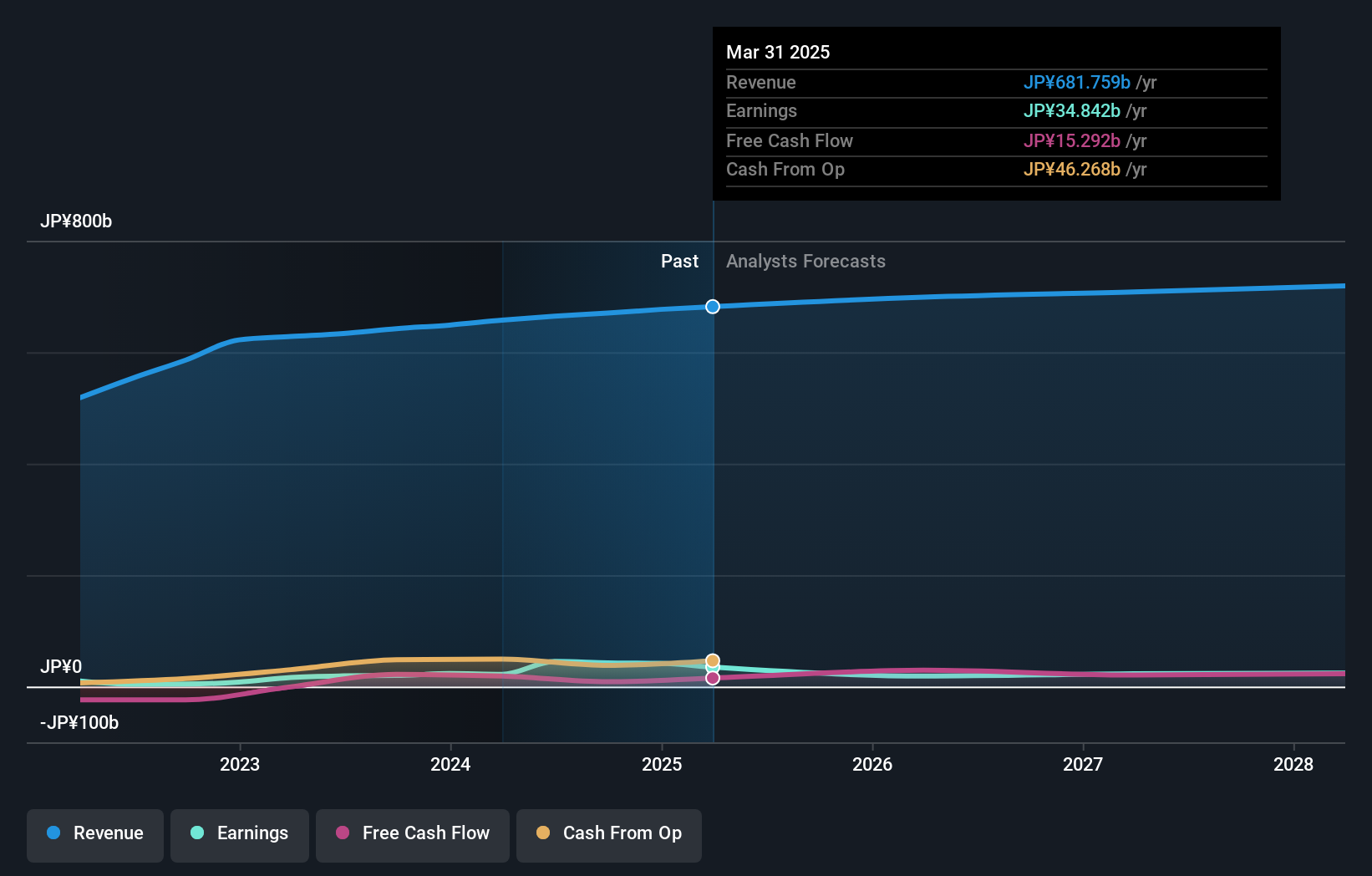

H2O Retailing (TSE:8242)

Simply Wall St Value Rating: ★★★★☆☆

Overview: H2O Retailing Corporation operates department stores, supermarkets, and shopping centers in Japan with a market capitalization of ¥226.17 billion.

Operations: H2O Retailing generates revenue primarily through its department stores, supermarkets, and shopping centers in Japan. The company's net profit margin has shown variability over recent periods.

In the Japanese retail landscape, H2O Retailing stands out with impressive earnings growth of 136% over the past year, surpassing industry averages. The company revised its earnings guidance upward for 2024, projecting a net sales increase to ¥702 billion and profits attributable to owners reaching ¥30 billion. Recent sales figures show consistent year-on-year growth, notably 115% in June and July. Despite a satisfactory debt-to-equity ratio of 39%, future earnings are expected to decrease by an average of 23% annually over the next three years.

- Click here to discover the nuances of H2O Retailing with our detailed analytical health report.

Gain insights into H2O Retailing's past trends and performance with our Past report.

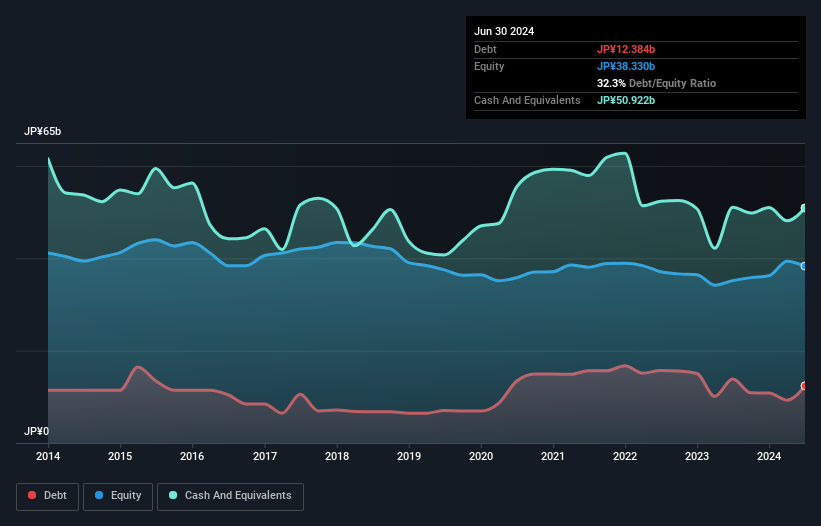

Toyo Securities (TSE:8614)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Toyo Securities Co., Ltd. operates as a financial products brokerage service provider in Japan, the United States, China, Hong Kong, and internationally with a market capitalization of ¥37.83 billion.

Operations: Toyo Securities generates revenue primarily from its Investment and Financial Services Business, amounting to ¥12.09 billion.

With a recent shift to profitability, Toyo Securities has emerged as an intriguing player in the market. Its debt-to-equity ratio climbed from 18.7% to 32.3% over five years, indicating increased leverage. However, high-quality earnings and more cash than total debt suggest resilience in its financial structure. Despite insufficient data on interest coverage by EBIT, the company seems well-positioned with positive free cash flow and no immediate cash runway concerns due to profitability gains this year.

- Take a closer look at Toyo Securities' potential here in our health report.

Gain insights into Toyo Securities' historical performance by reviewing our past performance report.

Key Takeaways

- Embark on your investment journey to our 733 Japanese Undiscovered Gems With Strong Fundamentals selection here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if H2O Retailing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8242

H2O Retailing

Operates department stores, supermarkets, and shopping centers in Japan.

Undervalued with proven track record.