Advertisement

- Japan

- /

- Diversified Financial

- /

- TSE:8439

Tokyo Century's (TSE:8439) Shareholders Will Receive A Bigger Dividend Than Last Year

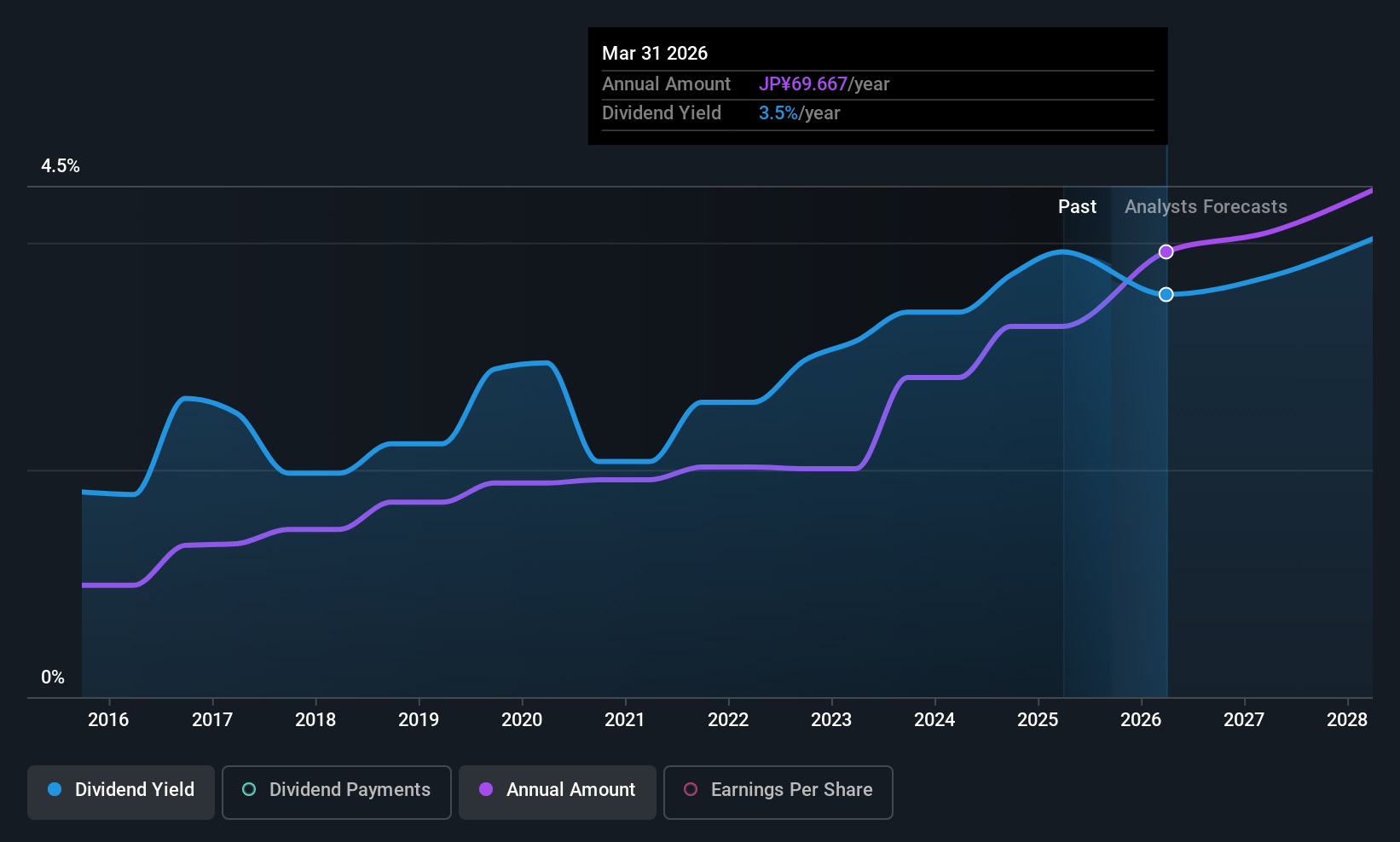

Tokyo Century Corporation (TSE:8439) will increase its dividend from last year's comparable payment on the 3rd of December to ¥34.00. This takes the annual payment to 3.5% of the current stock price, which is about average for the industry.

Tokyo Century's Projected Earnings Seem Likely To Cover Future Distributions

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue. Prior to this announcement, Tokyo Century's dividend was only 36% of earnings, however it was paying out 99% of free cash flows. The business might be trying to strike a balance between returning cash to shareholders and reinvesting back into the business, but this high of a payout ratio could definitely force the dividend to be cut if the company runs into a bit of a tough spot.

Over the next year, EPS is forecast to expand by 7.5%. If the dividend continues on this path, the payout ratio could be 40% by next year, which we think can be pretty sustainable going forward.

Check out our latest analysis for Tokyo Century

Tokyo Century Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ¥16.00 in 2015 to the most recent total annual payment of ¥68.00. This means that it has been growing its distributions at 16% per annum over that time. It is good to see that there has been strong dividend growth, and that there haven't been any cuts for a long time.

The Dividend Has Growth Potential

Investors could be attracted to the stock based on the quality of its payment history. Tokyo Century has impressed us by growing EPS at 6.0% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Tokyo Century will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 2 warning signs for Tokyo Century (of which 1 makes us a bit uncomfortable!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Tokyo Century might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8439

Tokyo Century

Provides equipment leasing, automobility, specialty financing, environmental infrastructure, and international businesses in Japan and internationally.

6 star dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.0% undervalued

22 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BI

BinocularMan on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

128 followersusers have followed this narrative

5 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

79 followersusers have followed this narrative

10 commentsusers have commented on this narrative

16 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

915 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative