Advertisement

- Japan

- /

- Hospitality

- /

- TSE:3082

Impressive Earnings May Not Tell The Whole Story For KICHIRI HOLDINGSLtd (TSE:3082)

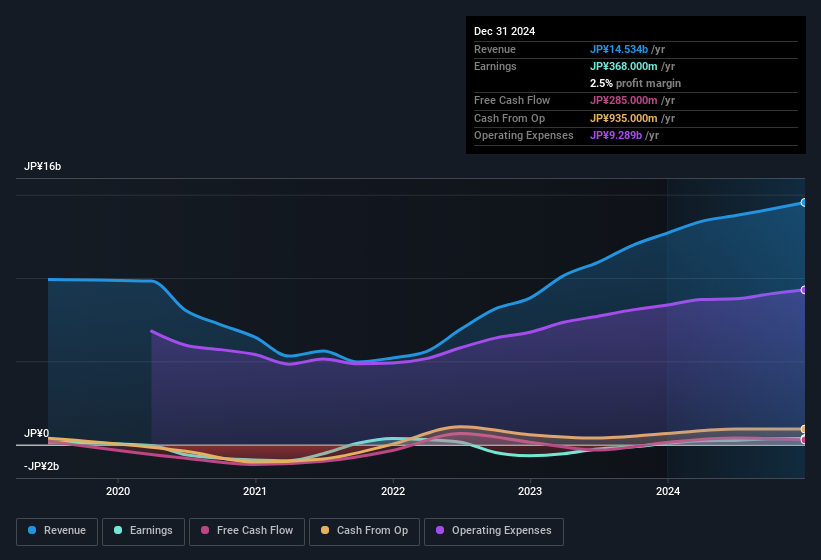

KICHIRI HOLDINGS & Co.,Ltd.'s (TSE:3082) robust earnings report didn't manage to move the market for its stock. Our analysis suggests that this might be because shareholders have noticed some concerning underlying factors.

View our latest analysis for KICHIRI HOLDINGSLtd

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, KICHIRI HOLDINGSLtd increased the number of shares on issue by 12% over the last twelve months by issuing new shares. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out KICHIRI HOLDINGSLtd's historical EPS growth by clicking on this link.

A Look At The Impact Of KICHIRI HOLDINGSLtd's Dilution On Its Earnings Per Share (EPS)

We don't have any data on the company's profits from three years ago. On the bright side, in the last twelve months it grew profit by 354%. On the other hand, earnings per share are only up 314% over the same period. So you can see that the dilution has had a bit of an impact on shareholders.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if KICHIRI HOLDINGSLtd can grow EPS persistently. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of KICHIRI HOLDINGSLtd.

How Do Unusual Items Influence Profit?

On top of the dilution, we should also consider the JP¥89m impact of unusual items in the last year, which had the effect of suppressing profit. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect KICHIRI HOLDINGSLtd to produce a higher profit next year, all else being equal.

Our Take On KICHIRI HOLDINGSLtd's Profit Performance

KICHIRI HOLDINGSLtd suffered from unusual items which depressed its profit in its last report; if that is not repeated then profit should be higher, all else being equal. But unfortunately the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). That will weigh on earnings per share, even if it is not reflected in net income. Based on these factors, it's hard to tell if KICHIRI HOLDINGSLtd's profits are a reasonable reflection of its underlying profitability. If you'd like to know more about KICHIRI HOLDINGSLtd as a business, it's important to be aware of any risks it's facing. You'd be interested to know, that we found 1 warning sign for KICHIRI HOLDINGSLtd and you'll want to know about it.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if KICHIRI HOLDINGSLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3082

KICHIRI HOLDINGSLtd

A food service company, operates and manages restaurants in Japan.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor