Advertisement

- Japan

- /

- Food and Staples Retail

- /

- TSE:9823

Even With A 25% Surge, Cautious Investors Are Not Rewarding Mammy Mart Corporation's (TSE:9823) Performance Completely

The Mammy Mart Corporation (TSE:9823) share price has done very well over the last month, posting an excellent gain of 25%. Notwithstanding the latest gain, the annual share price return of 9.2% isn't as impressive.

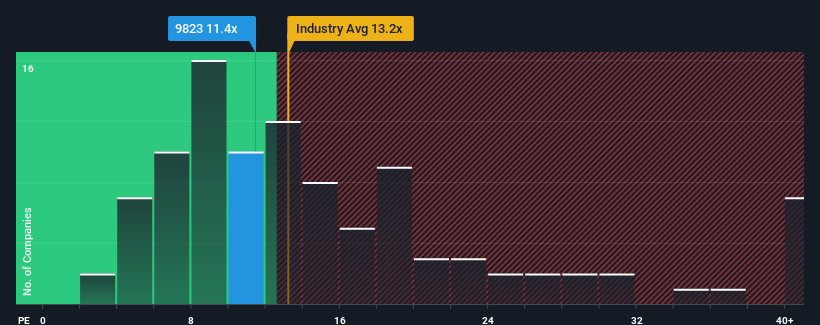

Although its price has surged higher, Mammy Mart may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 11.4x, since almost half of all companies in Japan have P/E ratios greater than 14x and even P/E's higher than 21x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

It looks like earnings growth has deserted Mammy Mart recently, which is not something to boast about. One possibility is that the P/E is low because investors think this benign earnings growth rate will likely underperform the broader market in the near future. If not, then existing shareholders may be feeling optimistic about the future direction of the share price.

View our latest analysis for Mammy Mart

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Mammy Mart's to be considered reasonable.

Taking a look back first, we see that there was hardly any earnings per share growth to speak of for the company over the past year. Fortunately, a few good years before that means that it was still able to grow EPS by 28% in total over the last three years. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 10% shows it's about the same on an annualised basis.

With this information, we find it odd that Mammy Mart is trading at a P/E lower than the market. It may be that most investors are not convinced the company can maintain recent growth rates.

The Key Takeaway

Despite Mammy Mart's shares building up a head of steam, its P/E still lags most other companies. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Mammy Mart currently trades on a lower than expected P/E since its recent three-year growth is in line with the wider market forecast. When we see average earnings with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued if recent medium-term earnings trends continue, but investors seem to think future earnings could see some volatility.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Mammy Mart with six simple checks on some of these key factors.

If you're unsure about the strength of Mammy Mart's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9823

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|10.4% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|12.4% undervalued

AN

Based on Analyst Price Targets