Advertisement

- Japan

- /

- Food and Staples Retail

- /

- TSE:8242

H2O Retailing's (TSE:8242) Attractive Earnings Are Not All Good News For Shareholders

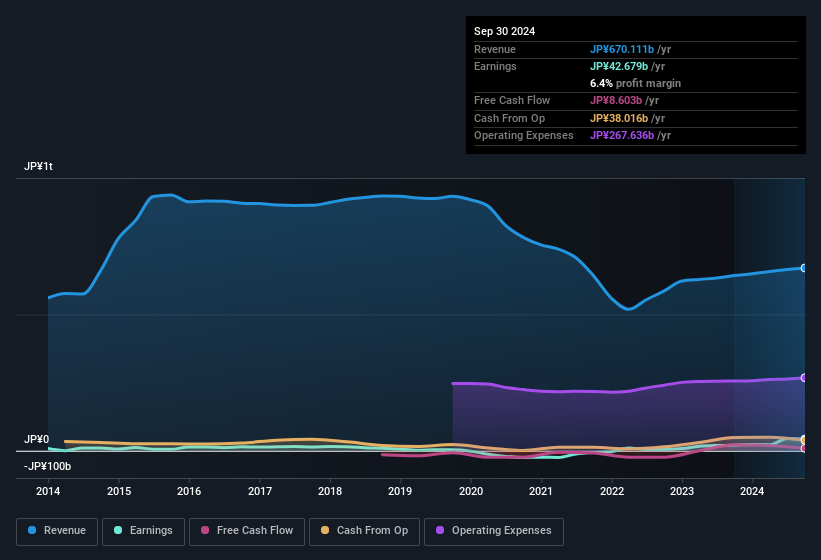

Even though H2O Retailing Corporation (TSE:8242) posted strong earnings recently, the stock hasn't reacted in a large way. We looked deeper into the numbers and found that shareholders might be concerned with some underlying weaknesses.

Check out our latest analysis for H2O Retailing

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, H2O Retailing increased the number of shares on issue by 6.2% over the last twelve months by issuing new shares. As a result, its net income is now split between a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of H2O Retailing's EPS by clicking here.

How Is Dilution Impacting H2O Retailing's Earnings Per Share (EPS)?

Three years ago, H2O Retailing lost money. On the bright side, in the last twelve months it grew profit by 115%. But EPS was less impressive, up only 118% in that time. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if H2O Retailing can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Finally, we should also consider the fact that unusual items boosted H2O Retailing's net profit by JP¥19b over the last year. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. We can see that H2O Retailing's positive unusual items were quite significant relative to its profit in the year to September 2024. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On H2O Retailing's Profit Performance

In its last report H2O Retailing benefitted from unusual items which boosted its profit, which could make the profit seem better than it really is on a sustainable basis. On top of that, the dilution means that its earnings per share performance is worse than its profit performance. Considering all this we'd argue H2O Retailing's profits probably give an overly generous impression of its sustainable level of profitability. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. To that end, you should learn about the 4 warning signs we've spotted with H2O Retailing (including 1 which is significant).

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if H2O Retailing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8242

H2O Retailing

Engages in the development, operation, and management of commercial facilities in Japan.

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor