Advertisement

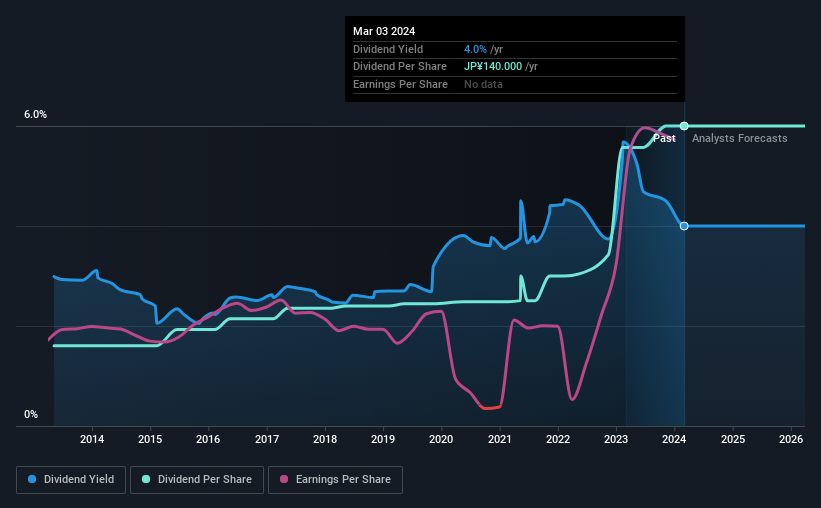

The board of Sangetsu Corporation (TSE:8130) has announced that it will be paying its dividend of ¥75.00 on the 24th of June, an increased payment from last year's comparable dividend. This takes the dividend yield to 4.0%, which shareholders will be pleased with.

View our latest analysis for Sangetsu

Sangetsu's Payment Has Solid Earnings Coverage

If the payments aren't sustainable, a high yield for a few years won't matter that much. However, prior to this announcement, Sangetsu was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. The business is earning enough to make the dividend feasible, but the cash payout ratio of 81% shows that most of the cash is going back to the shareholders, which could constrain growth prospects going forward.

The next year is set to see EPS grow by 4.7%. If the dividend continues along recent trends, we estimate the payout ratio will be 59%, which is in the range that makes us comfortable with the sustainability of the dividend.

Sangetsu Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. The dividend has gone from an annual total of ¥37.50 in 2014 to the most recent total annual payment of ¥140.00. This implies that the company grew its distributions at a yearly rate of about 14% over that duration. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Sangetsu has impressed us by growing EPS at 29% per year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

In Summary

Overall, this is a reasonable dividend, and it being raised is an added bonus. On the plus side, the dividend looks sustainable by most measures but it is let down by the lack of cash flows. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Are management backing themselves to deliver performance? Check their shareholdings in Sangetsu in our latest insider ownership analysis. Is Sangetsu not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8130

Sangetsu

Engages in the planning, development, manufacture, sale, and installation of interior decorating products in Japan and internationally.

Flawless balance sheet 6 star dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor