Advertisement

Yamaha (TSE:7951): Assessing Valuation After Share Buyback Launch and Earnings Upgrade

Simply Wall St

Reviewed by Simply Wall St

Yamaha (TSE:7951) is making headlines as it unveils a substantial share buyback program, along with raising its earnings guidance for the year. These moves underscore management’s focus on shareholder value and future growth.

See our latest analysis for Yamaha.

Following Yamaha’s announcement of a new share buyback and improved earnings guidance, the stock’s momentum has picked up, as reflected in its 1-month share price return of 5.2% and a solid 10.5% gain over the past 90 days, after a more muted start to the year. Despite these positive recent moves, the 1-year total shareholder return stands at just 0.3%, and longer-term investors are still feeling the sting of three- and five-year total returns, which remain deep in negative territory. The shift in direction suggests investors are increasingly optimistic about management’s push for value and growth.

If upbeat management moves have you curious what else is gaining traction, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

With share buybacks and stronger guidance fueling recent momentum, the big question is whether Yamaha’s fundamentals still offer value for new investors, or if the market has already priced in this renewed optimism.

Most Popular Narrative: 5.9% Undervalued

Compared to Yamaha’s last close near ¥1,065, the most widely followed narrative attributes a higher fair value, driven by expectations for new growth levers. This perspective anchors expectations to emerging industry trends and the company’s focus on upmarket digital solutions.

Recent investments in digital transformation, including new product launches (digital pianos, electronic drums, and music tech from the Silicon Valley base), are positioned to capitalize on global growth in digital music creation and music education. These initiatives support higher-margin revenue streams and future earnings growth. Strategic focus on innovation and automation, such as structural reforms in piano manufacturing and new collaborative technologies, is expected to improve long-term operational efficiency and bolster net profit margins.

Wondering what bold projections are hiding under the surface? The narrative’s verdict is built on forecasts for rising profit, higher-margin sales mix, and a leaner cost structure. Get the inside story on how these levers could reshape fair value and spark a re-rating.

Result: Fair Value of ¥1,132.5 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing currency volatility and weaker demand in key audio segments could quickly undermine analysts’ upbeat projections and challenge the current fair value narrative.

Find out about the key risks to this Yamaha narrative.

Another View: A Multiples-Based Cross-Check

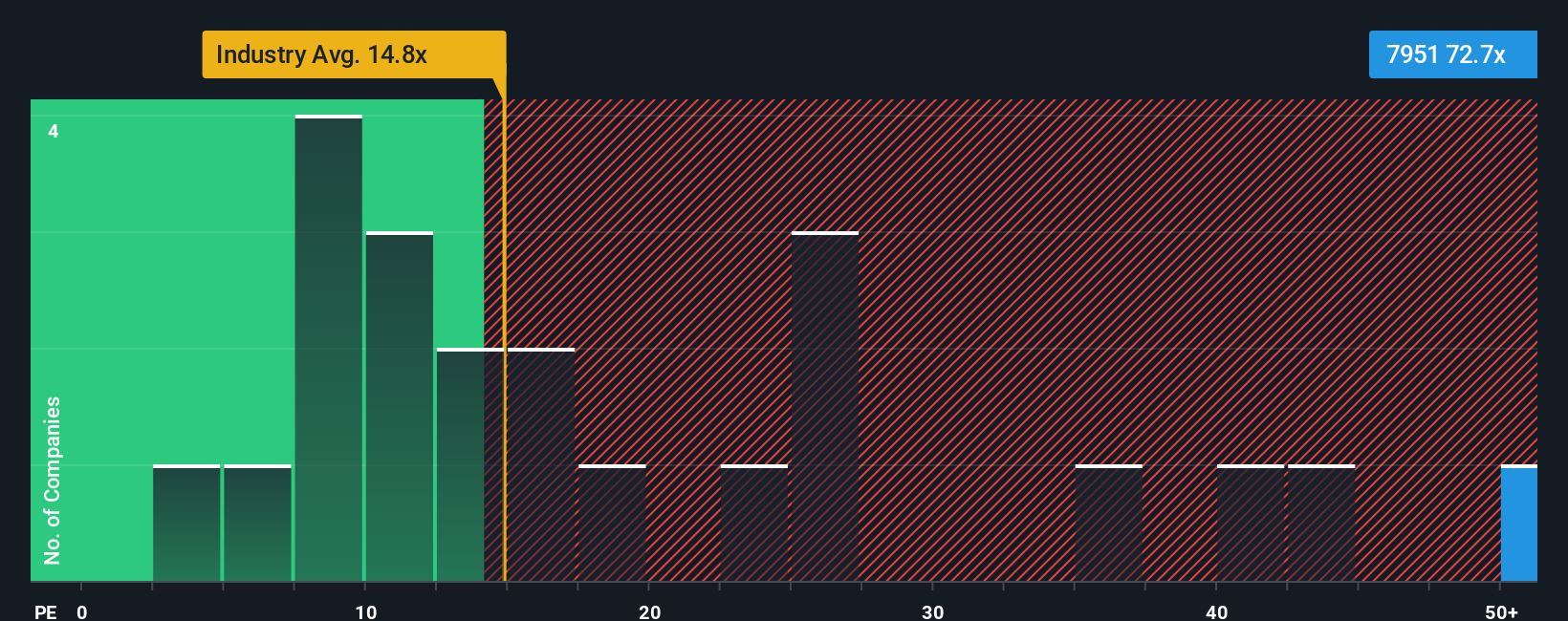

While analysts see Yamaha as undervalued based on future earnings potential, the market tells a different story. The current price sits at 27.1 times earnings, noticeably higher than the industry average of 14.5x, the peer average of 20.8x, and even the fair ratio of 21x. This premium suggests that investor optimism may already be embedded in the stock price, raising questions about how much upside truly remains if future results fall short.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Yamaha Narrative

If these perspectives don’t quite match your outlook, you have all the tools to dig into the data, draw your own conclusions, and share your unique take in just minutes. Do it your way

A great starting point for your Yamaha research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Ready to step up your investing game? Seize these opportunities now with hand-picked ideas that could sharpen your portfolio’s performance and keep you ahead of the curve.

- Uncover hidden value by checking out these 865 undervalued stocks based on cash flows which stand out for their compelling cash flow potential and attractive entry points in today’s market.

- Tap into the next big wave in artificial intelligence by using these 25 AI penny stocks to position yourself for growth as AI reshapes entire industries worldwide.

- Secure steady income by browsing these 14 dividend stocks with yields > 3% that offer yields above 3 percent, ideal for investors seeking reliable returns and long-term stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7951

Yamaha

Engages in the musical instruments, audio equipment, and other businesses in Japan and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor