Advertisement

ASICS (TSE:7936): Assessing Valuation Following Strong Share Price Performance

Simply Wall St

Reviewed by Simply Wall St

ASICS (TSE:7936) shares have caught the attention of investors following recent movement in its stock price. Many are looking at its performance, along with broader trends in the sportswear industry, to gauge potential future value.

See our latest analysis for ASICS.

ASICS has been steadily building momentum after a strong showing this year, with its share price currently at ¥3,960. The stock’s year-to-date price return sits at an impressive 29.45 percent, while its one-year total shareholder return has soared to 52.55 percent. Looking further back, long-term holders have seen significant rewards, with total returns of more than 600 percent over three years and well over 1,000 percent over five years. This points to sustained confidence in the company’s growth story.

If you’re looking to broaden your search beyond the sportswear sector, now is a great time to explore fast growing stocks with high insider ownership.

With ASICS hitting new highs and the business showing impressive growth, the key question for investors is whether the recent run-up has left the stock undervalued or if all future upside is already reflected in the price.

Price-to-Earnings of 37.7x: Is it justified?

ASICS is currently valued at a price-to-earnings (P/E) ratio of 37.7x, which places it well above both the industry average and peer comparisons. The current share price of ¥3,960 reflects these high expectations.

The P/E ratio measures how much investors are willing to pay for each yen of ASICS’s earnings. In consumer durables and specifically luxury goods, this metric often captures views on future growth, margins, and brand power. A higher ratio typically means the market expects rapid or sustained profit improvement.

At 37.7x, ASICS trades at nearly three times the JP Luxury sector average of 13.3x and the peer average of 13.7x. This signals investors are pricing in much stronger growth potential or profitability than the broader market expects. However, when compared to the estimated fair P/E ratio of 23x, ASICS still stands considerably above the level the market may move toward if sentiment changes or growth falls short.

Explore the SWS fair ratio for ASICS

Result: Price-to-Earnings of 37.7x (OVERVALUED)

However, slowing revenue growth or unexpected shifts in consumer demand could challenge the current optimism surrounding ASICS’s high valuation.

Find out about the key risks to this ASICS narrative.

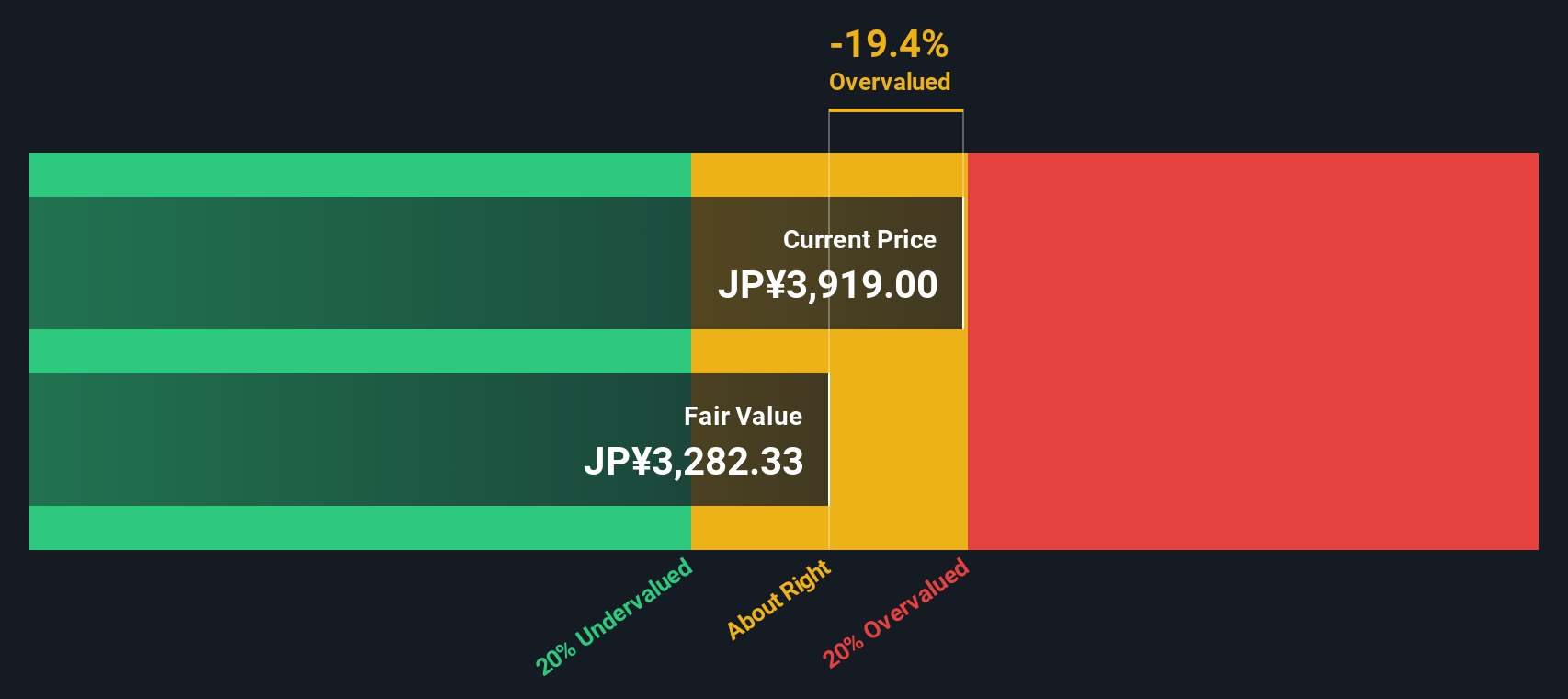

Another View: What Does the SWS DCF Model Say?

While the P/E ratio points to ASICS being overvalued compared to its peers and the market, our SWS DCF model offers a different perspective for investors. According to the DCF estimate, ASICS is trading above its fair value, suggesting that the current price may already reflect much of the anticipated growth. The key question is whether future earnings can increase quickly enough to justify this premium.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASICS for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 831 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ASICS Narrative

If you find yourself looking for deeper insight or prefer to draw your own conclusions from the numbers, you can put together your perspective in just a few minutes. Do it your way.

A great starting point for your ASICS research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready to Find Your Next Winning Opportunity?

Don’t overlook the power of a well-timed strategy. Level up your investing now by tapping into high-potential stocks other investors are already watching. Here are three hand-picked ways you can expand your portfolio today:

- Grow your income and safeguard your capital by targeting stable companies with above-average yields when you start with these 24 dividend stocks with yields > 3%.

- Ride the AI wave and position yourself for growth by seeking out the most exciting innovations through these 26 AI penny stocks.

- Capitalize on untapped opportunities and value stocks flying under the radar. Jump in with these 831 undervalued stocks based on cash flows and stay ahead of the market crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7936

ASICS

Manufactures and sells sporting goods in Japan and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor