Advertisement

ASICS (TSE:7936): Assessing Valuation as Shares Rally Without a Clear Catalyst

Kshitija Bhandaru

Reviewed by Simply Wall St

ASICS (TSE:7936) might just be grabbing your attention lately, especially as its share price has shown strong momentum even without a specific headline event to set things off. Sometimes the shift in a stock’s direction is itself the story, raising questions about how the market is sizing up ASICS’s future. Is this recent activity just routine volatility, or does it reflect a quiet confidence in the company’s fundamentals that is worth a closer look?

Looking back, ASICS’s performance paints a clear trend. The stock has delivered a return of 53% over the past year and more than doubled in value over five years. With shares up 17% in the past month alone and a 34% gain year-to-date, momentum appears to be gathering steam. This comes on top of consistent revenue and net income growth annually, keeping ASICS in focus even without a headline-grabbing event.

With the share price moving up and no obvious announcement to explain the momentum, are investors looking at a bargain or has the market already factored in all the future growth ASICS can deliver?

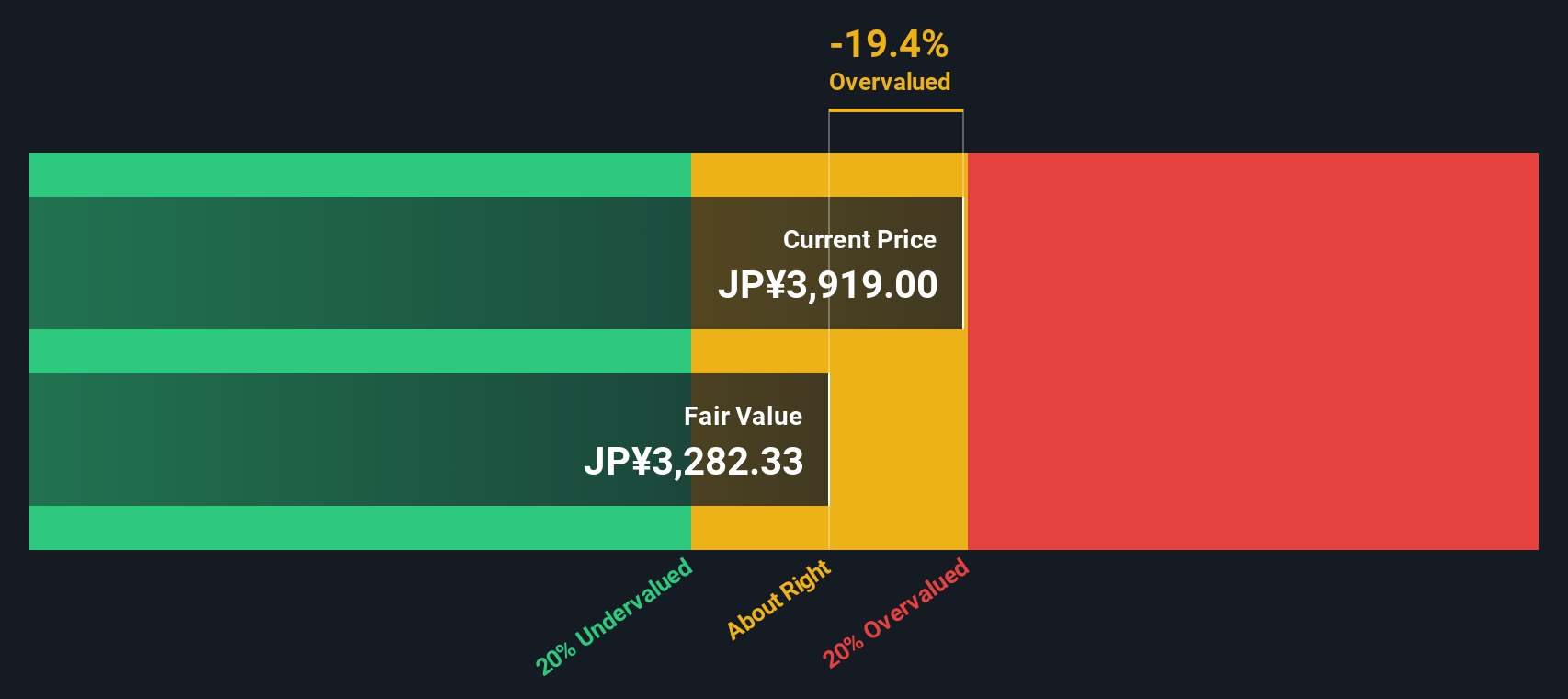

Price-to-Earnings of 38.9x: Is it justified?

ASICS currently trades at a price-to-earnings (P/E) ratio of 38.9x, which is significantly higher than both its industry average and the estimated fair multiple. This suggests that the market may be valuing the company’s future earnings at a premium compared to its peers.

The P/E ratio is a popular metric used to gauge whether a stock is expensive or cheap relative to its actual earnings. For a consumer durables and luxury brand like ASICS, a higher P/E could signal confidence in ongoing growth or profitability. However, it can also reflect overly optimistic expectations that may not be sustainable.

ASICS’s P/E ratio stands well above the JP Luxury industry average and its fair value estimates. This indicates that investors might be overpricing the company’s expected future earnings. Whether this premium is justified will depend on ASICS’s ability to continue delivering strong profit growth and outperforming its sector rivals.

Result: Fair Value of ¥3386.26 (OVERVALUED)

See our latest analysis for ASICS.However, slowing revenue or profit growth could temper current optimism. This could potentially lead to a market reassessment if future earnings fail to meet expectations.

Find out about the key risks to this ASICS narrative.Another View: What Does the SWS DCF Model Suggest?

Taking a step back from earnings multiples, our DCF model arrives at a valuation that also points to ASICS being overvalued, which echoes the warning from the multiples approach. But can both methods be missing something, or is market enthusiasm really running ahead of fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own ASICS Narrative

If you see the numbers differently or want to test your own ideas, it takes just a few minutes to build your own view from the ground up. Do it your way

A great starting point for your ASICS research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for Your Next Opportunity?

Don’t limit yourself to just one stock story. Use Simply Wall Street’s tools to uncover new angles, smart strategies, and investments leading their fields. Every idea could be your next win.

- Amplify your portfolio’s income potential by finding top picks with dividend stocks with yields > 3% that consistently beat the 3% yield mark.

- Catch innovation early and see which pioneers are harnessing artificial intelligence in healthcare with our healthcare AI stocks.

- Uncover value plays hiding in plain sight with our unique approach to undervalued stocks based on cash flows and position yourself ahead of the trend.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About TSE:7936

ASICS

Manufactures and sells sporting goods in Japan and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor