Advertisement

YONEX (TSE:7906): Assessing Valuation Following Recent Share Price Pullback

Simply Wall St

Reviewed by Simply Wall St

YONEX (TSE:7906) has seen its stock take a small dip of over 10% over the past week, despite double-digit annual revenue and net income growth. Investors seem to be weighing this recent move in comparison with the company’s strong long-term returns.

See our latest analysis for YONEX.

Despite the sharp 10% drop in share price this past week, YONEX’s overall momentum remains solid, with a 73% year-to-date share price return and a staggering 77% total shareholder return for the past year. After such a strong run, this recent pullback signals investors are pausing to reassess longer-term upside and potential risks. This comes especially after the company’s exceptional five-year total return, which exceeds 550%.

If you’re interested in finding other companies with powerful growth track records and committed insiders, it might be time to discover fast growing stocks with high insider ownership

The question now is whether the recent pullback is a signal that YONEX is undervalued, presenting a timely entry point, or if the market has already factored in its future growth prospects.

Price-to-Earnings of 27.4x: Is it justified?

YONEX is currently trading at a price-to-earnings (P/E) ratio of 27.4x, which places it well above the sector and market averages. For investors, this signals that the market is attributing a premium to YONEX's future profit potential relative to peer companies.

The price-to-earnings ratio measures the company’s share price relative to its annual earnings per share. It is particularly relevant in the consumer durables and leisure sector, as it reflects how much investors are willing to pay today for expected future earnings growth. A high P/E can mean the market expects strong future performance, but it can also indicate over-optimism if growth does not materialize.

In YONEX’s case, the company’s P/E far exceeds both the peer average of 16.5x and the broader JP Leisure industry average of 13.3x. Even compared to an estimated "fair" P/E of 18.6x, YONEX's current valuation appears expensive. This premium could quickly compress if earnings growth projections fall short or sector sentiment shifts.

Explore the SWS fair ratio for YONEX

Result: Price-to-Earnings of 27.4x (OVERVALUED)

However, future growth may slow if sector sentiment weakens or if YONEX fails to meet high earnings expectations. This could potentially pressure the premium valuation.

Find out about the key risks to this YONEX narrative.

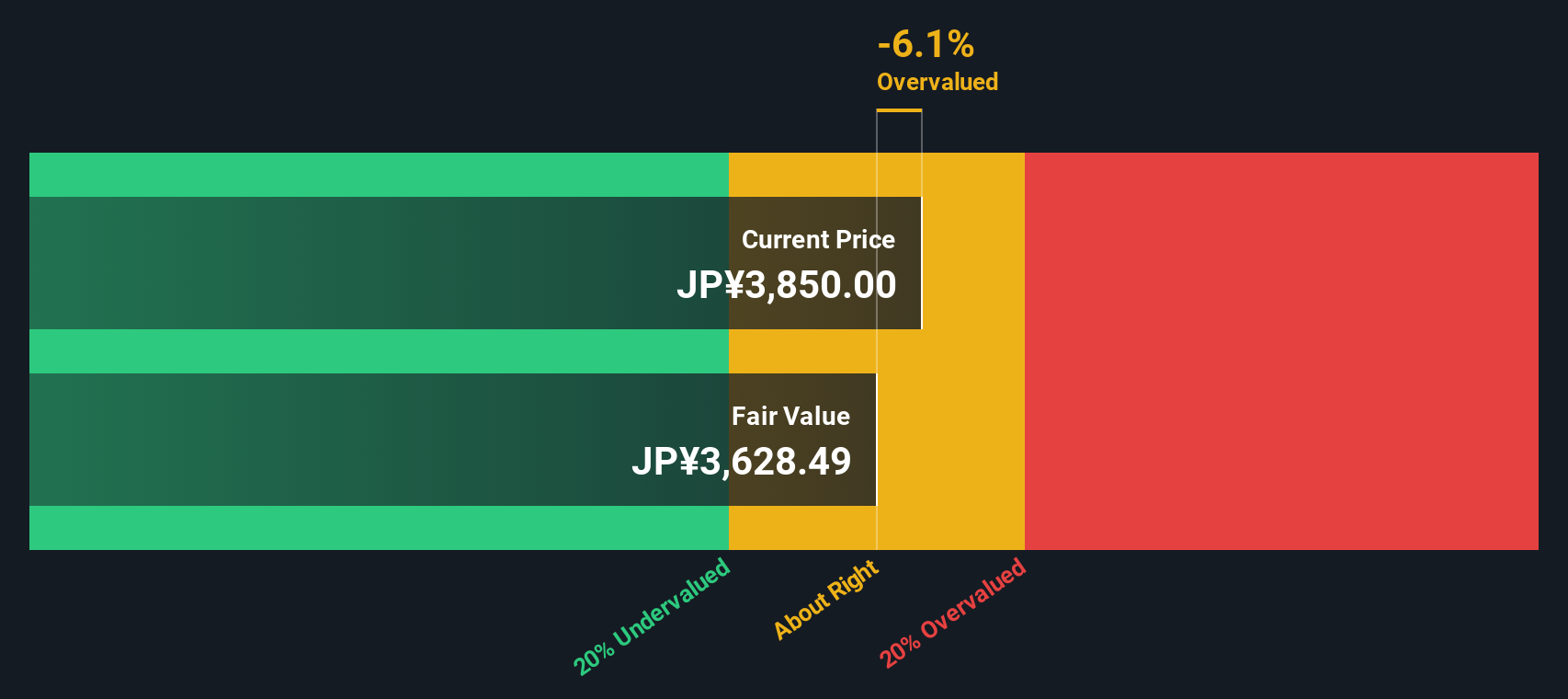

Another View: Discounted Cash Flow Suggests Undervaluation

While YONEX's share price appears expensive based on its price-to-earnings ratio, our DCF model offers a different perspective. By forecasting future cash flows, the SWS DCF model estimates the fair value at ¥3,842.24, which is about 3.8% above the current price. Could this indicate an overlooked opportunity?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out YONEX for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own YONEX Narrative

If you have your own perspective or want to dig into the numbers yourself, building a personal view takes just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding YONEX.

Looking for More Investment Ideas?

Stay ahead of the market by taking advantage of these powerful tools to spot fresh opportunities. Smart money moves start with having the right shortlist.

- Uncover companies leading AI innovation by tapping into these 26 AI penny stocks and see which stocks are driving the next big breakthrough.

- Maximize your income potential by finding market leaders generating attractive yields through these 15 dividend stocks with yields > 3% right now.

- Step into tomorrow with these 26 quantum computing stocks and access revolutionary businesses on the frontlines of quantum computing technology.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7906

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor