Advertisement

3 Asian Stocks That May Be Trading Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by economic uncertainties and shifting investor sentiment, the Asian markets have shown resilience amidst these challenges. With concerns about elevated valuations and cautious monetary policies influencing investment decisions, identifying stocks that may be undervalued can offer potential opportunities for investors seeking value in this environment.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xi'an International Medical Investment (SZSE:000516) | CN¥4.79 | CN¥9.38 | 48.9% |

| WT Microelectronics (TWSE:3036) | NT$134.00 | NT$267.06 | 49.8% |

| Visional (TSE:4194) | ¥9987.00 | ¥19552.71 | 48.9% |

| SK hynix (KOSE:A000660) | ₩571000.00 | ₩1133582.49 | 49.6% |

| Samyang Foods (KOSE:A003230) | ₩1401000.00 | ₩2750940.82 | 49.1% |

| Nippon Thompson (TSE:6480) | ¥706.00 | ¥1406.48 | 49.8% |

| Ningxia Building Materials GroupLtd (SHSE:600449) | CN¥13.21 | CN¥26.19 | 49.6% |

| New Zealand King Salmon Investments (NZSE:NZK) | NZ$0.196 | NZ$0.39 | 49.2% |

| Nanjing COSMOS Chemical (SZSE:300856) | CN¥14.72 | CN¥29.31 | 49.8% |

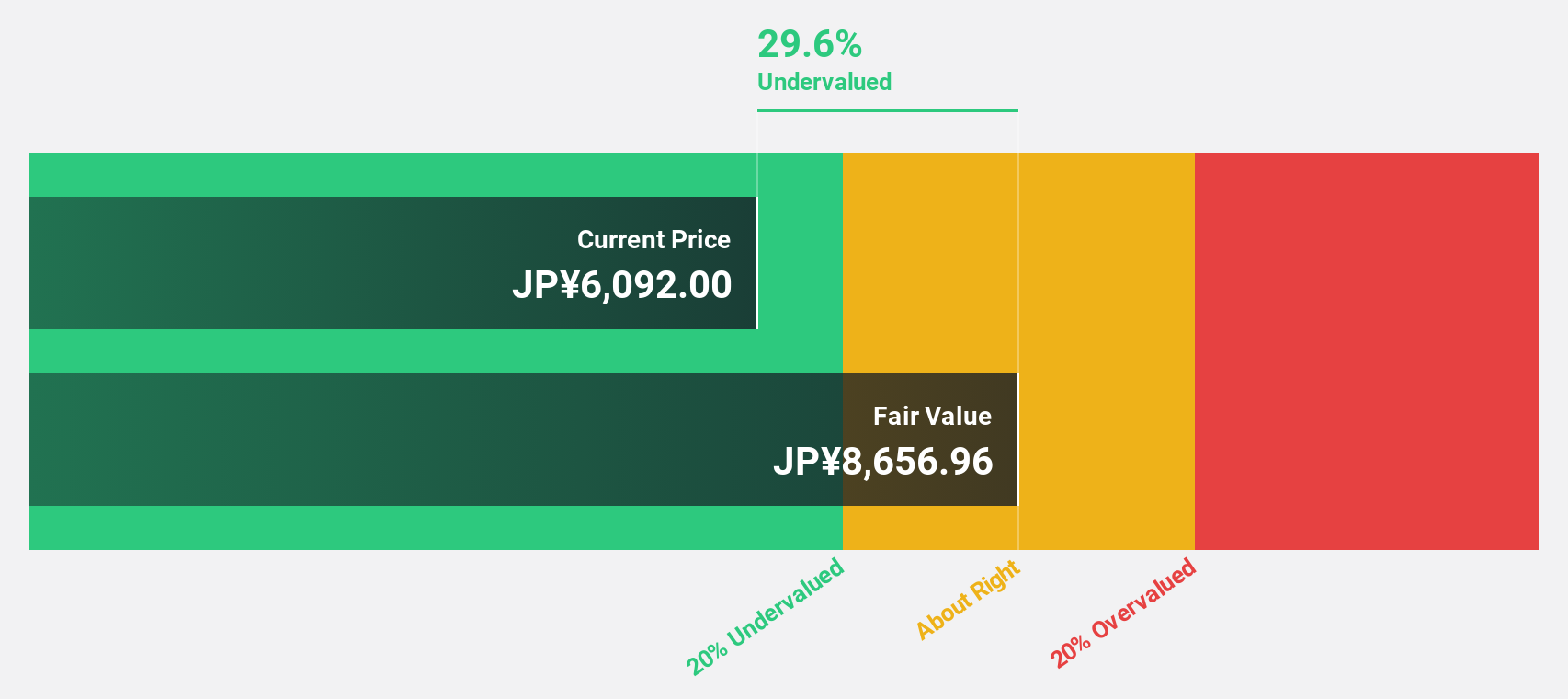

| JINS HOLDINGS (TSE:3046) | ¥6090.00 | ¥12164.26 | 49.9% |

We'll examine a selection from our screener results.

Chugai Pharmaceutical (TSE:4519)

Overview: Chugai Pharmaceutical Co., Ltd. operates in the research, development, manufacture, sale, importation, and exportation of pharmaceuticals both in Japan and globally with a market capitalization of approximately ¥13.62 trillion.

Operations: Chugai Pharmaceutical's revenue primarily stems from its activities in researching, developing, manufacturing, selling, importing, and exporting pharmaceuticals across Japan and international markets.

Estimated Discount To Fair Value: 15.9%

Chugai Pharmaceutical is trading at ¥8,278, below its estimated fair value of ¥9,847.52. The company's revenue is projected to grow at 5.8% annually, outpacing the Japanese market's 4.5%. Recent strategic moves include acquiring Renalys Pharma for exclusive rights in Asia and a collaboration with Rani Therapeutics potentially valued up to $1.085 billion if fully realized. Despite high share price volatility recently, Chugai's earnings are expected to grow faster than the market average at 10.5% per year.

- Upon reviewing our latest growth report, Chugai Pharmaceutical's projected financial performance appears quite optimistic.

- Dive into the specifics of Chugai Pharmaceutical here with our thorough financial health report.

Sega Sammy Holdings (TSE:6460)

Overview: Sega Sammy Holdings Inc. operates in the entertainment contents business through its subsidiaries and has a market cap of approximately ¥547.08 billion.

Operations: The company's revenue primarily comes from its Entertainment Contents segment, generating ¥329.25 billion, followed by Pachislot & Pachinko Machines at ¥74.41 billion and the Gaming Business contributing ¥12.22 billion.

Estimated Discount To Fair Value: 31.8%

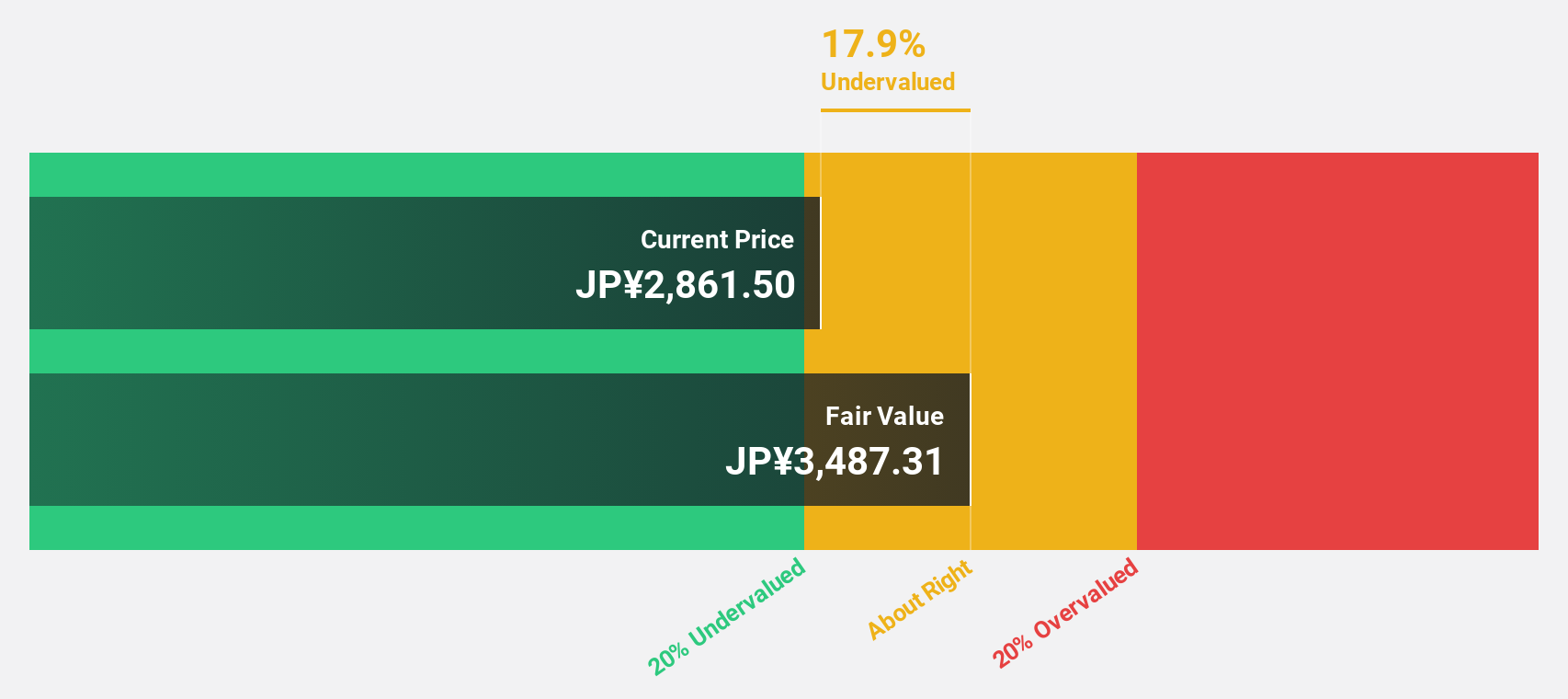

Sega Sammy Holdings is trading at ¥2,602, significantly below its estimated fair value of ¥3,813.16. Analysts anticipate a 43.9% price increase, supported by strong projected earnings growth of 23.74% annually over the next three years, outpacing the Japanese market's 8%. Although recent profit margins have decreased from 8.8% to 4.2%, revenue growth is expected to surpass the market average at 6.5% per year. The dividend increased to ¥27 per share despite being poorly covered by free cash flows.

- Our earnings growth report unveils the potential for significant increases in Sega Sammy Holdings' future results.

- Navigate through the intricacies of Sega Sammy Holdings with our comprehensive financial health report here.

Andes Technology (TWSE:6533)

Overview: Andes Technology Corporation provides embedded system application solutions and has a market cap of NT$13.42 billion.

Operations: The company generates revenue primarily from the design and sales of silicon intellectual property, amounting to NT$1.48 billion.

Estimated Discount To Fair Value: 45.5%

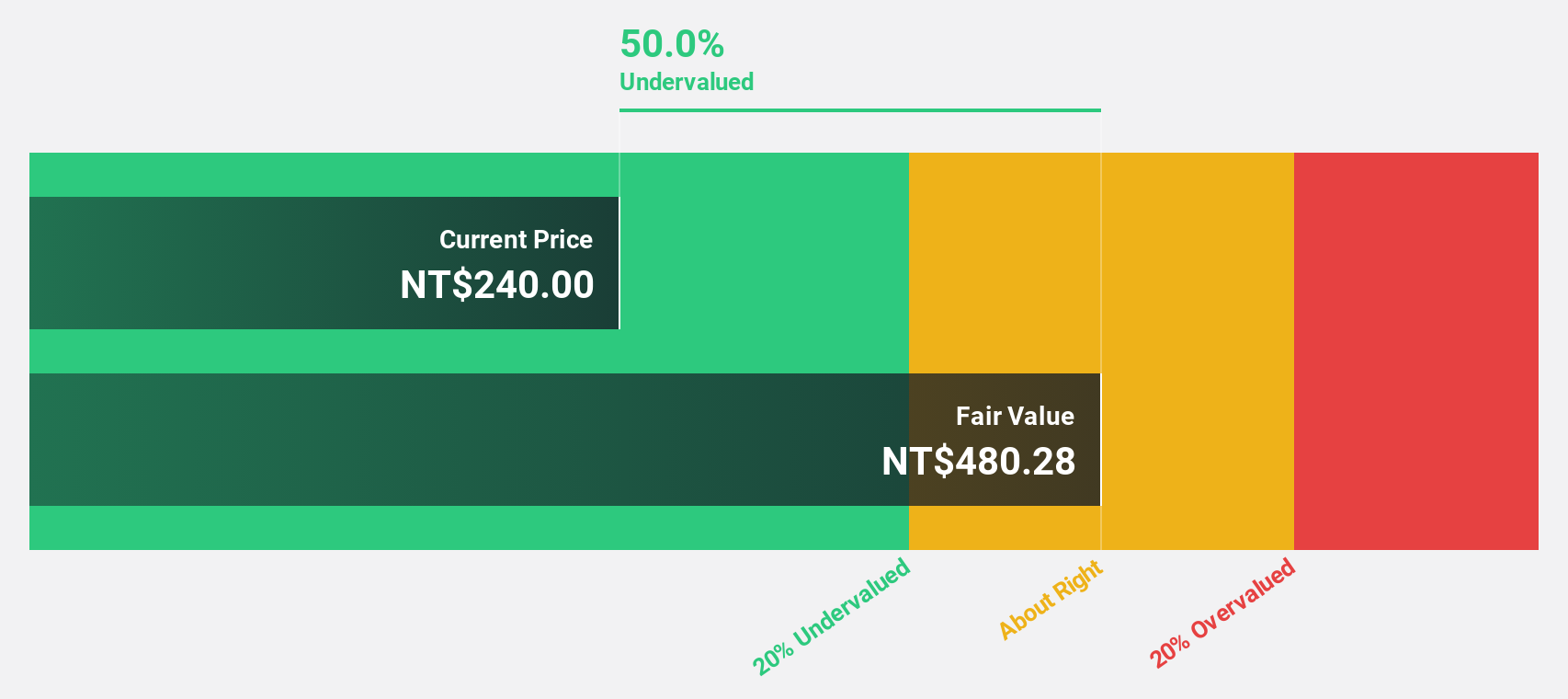

Andes Technology, trading at NT$265, is significantly undervalued with a fair value estimate of NT$485.92. Revenue growth is projected at 29.1% annually, outpacing the Taiwan market's average of 13.3%. Despite a low forecasted return on equity of 13.4%, Andes anticipates profitability within three years, bolstered by its collaboration with d-Matrix on AI inference technology and recent earnings improvement from a net loss to TWD 8.46 million in Q3 2025.

- The analysis detailed in our Andes Technology growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Andes Technology.

Summing It All Up

- Delve into our full catalog of 272 Undervalued Asian Stocks Based On Cash Flows here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6460

Sega Sammy Holdings

Through its subsidiaries, engages in the entertainment contents business.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor