- Japan

- /

- Professional Services

- /

- TSE:6532

Sumitomo Chemical Company And 2 Other Japanese Stocks Estimated To Be Undervalued

Reviewed by Simply Wall St

Japan’s stock markets have seen modest gains recently, with the Nikkei 225 Index rising 0.8% and the broader TOPIX Index up 0.2%. Amid speculation about potential interest rate hikes by the Bank of Japan, investors are keenly observing market movements and economic indicators to identify undervalued opportunities. In this context, finding stocks that are trading below their intrinsic value can be particularly rewarding for investors looking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Japan

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Funai Soken Holdings (TSE:9757) | ¥2321.00 | ¥4639.80 | 50% |

| Hagiwara Electric Holdings (TSE:7467) | ¥3540.00 | ¥6768.43 | 47.7% |

| Kotobuki Spirits (TSE:2222) | ¥1729.00 | ¥3434.73 | 49.7% |

| Densan System Holdings (TSE:4072) | ¥2787.00 | ¥5355.04 | 48% |

| BayCurrent Consulting (TSE:6532) | ¥4564.00 | ¥8597.45 | 46.9% |

| EnomotoLtd (TSE:6928) | ¥1495.00 | ¥2948.54 | 49.3% |

| Adventure (TSE:6030) | ¥3815.00 | ¥7430.44 | 48.7% |

| Visional (TSE:4194) | ¥8890.00 | ¥17141.03 | 48.1% |

| TORIDOLL Holdings (TSE:3397) | ¥3726.00 | ¥7370.81 | 49.4% |

| SBI ARUHI (TSE:7198) | ¥860.00 | ¥1705.03 | 49.6% |

Let's take a closer look at a couple of our picks from the screened companies.

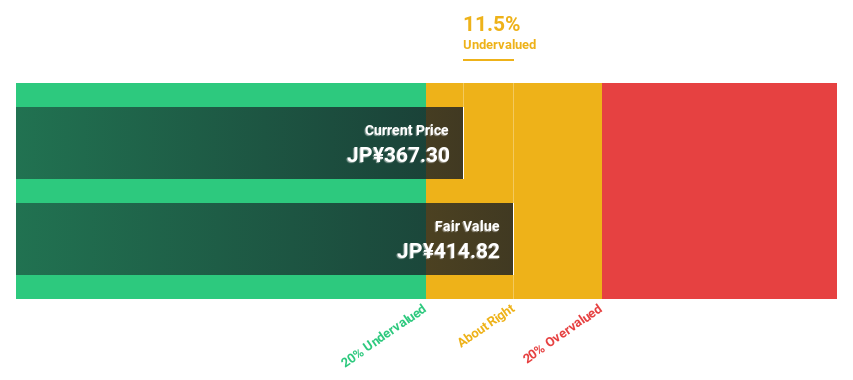

Sumitomo Chemical Company (TSE:4005)

Overview: Sumitomo Chemical Company, Limited operates globally in chemicals and plastics, energy and functional materials, IT-related chemicals, health and crop sciences, pharmaceuticals, among other sectors with a market cap of ¥678.09 billion.

Operations: Sumitomo Chemical's revenue segments include Essential Chemicals (¥789.13 billion), IT-Related Chemicals (¥431.63 billion), Health and Agriculture Related Business (¥562.22 billion), Energy & Functional Materials (¥310.76 billion), and Pharmaceuticals (¥357.67 billion).

Estimated Discount To Fair Value: 41.3%

Sumitomo Chemical Company is trading at ¥414.3, significantly below its estimated fair value of ¥705.76, indicating it may be undervalued based on discounted cash flow analysis. Despite a forecasted revenue growth of 4.5% per year and expected profitability within three years, its debt coverage by operating cash flow is weak and the dividend yield of 2.17% isn't well supported by earnings or free cash flows. Recent events include being added to the S&P Japan Mid Cap 100 index but dropped from several international indices in June 2024.

- Upon reviewing our latest growth report, Sumitomo Chemical Company's projected financial performance appears quite optimistic.

- Delve into the full analysis health report here for a deeper understanding of Sumitomo Chemical Company.

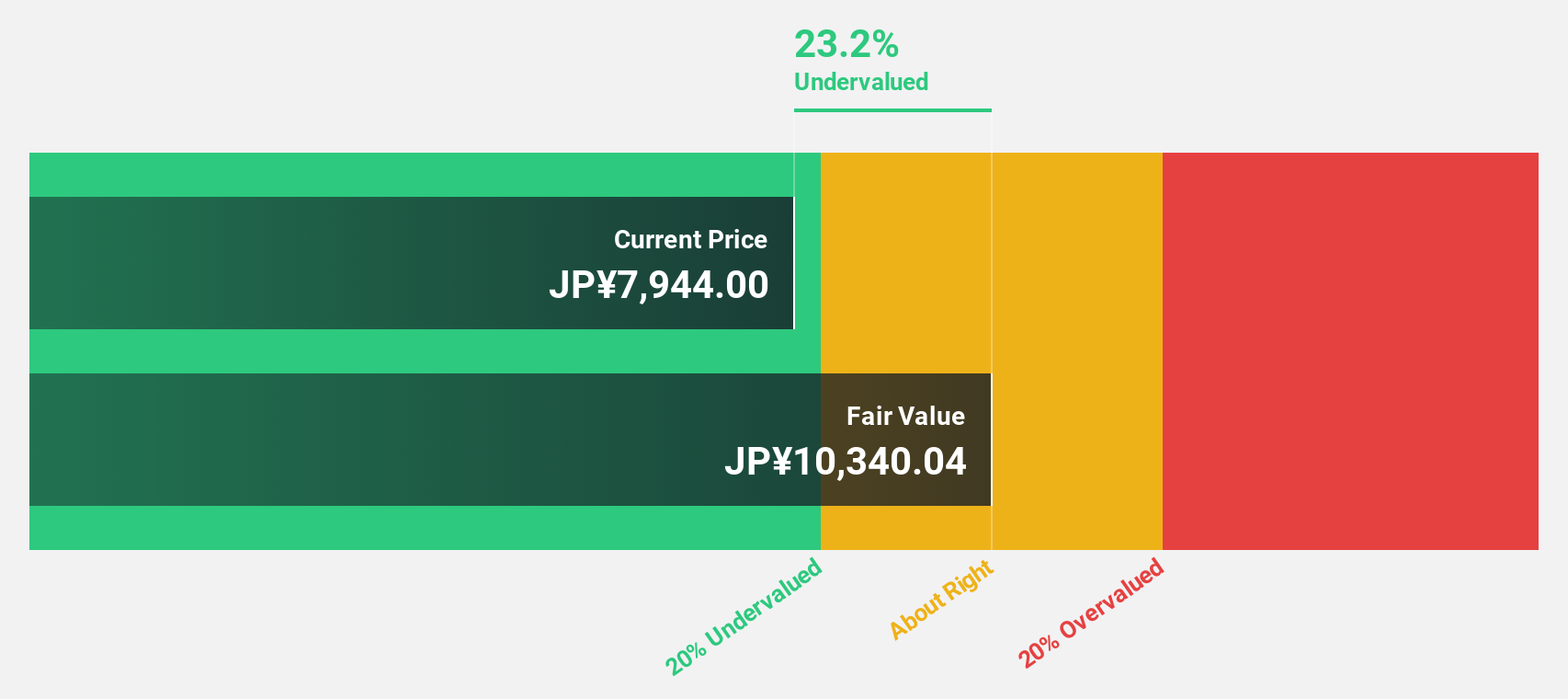

BayCurrent Consulting (TSE:6532)

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market cap of ¥692.46 billion.

Operations: BayCurrent Consulting, Inc. generates revenue through its consulting services in Japan.

Estimated Discount To Fair Value: 46.9%

BayCurrent Consulting is trading at ¥4564, well below its estimated fair value of ¥8597.45, suggesting it is undervalued based on discounted cash flow analysis. The company's earnings grew by 17.4% over the past year and are forecast to grow 18.52% annually, outpacing the JP market's average growth rates in both revenue and earnings. However, its share price has been highly volatile recently, which may pose a risk for investors seeking stability.

- The analysis detailed in our BayCurrent Consulting growth report hints at robust future financial performance.

- Unlock comprehensive insights into our analysis of BayCurrent Consulting stock in this financial health report.

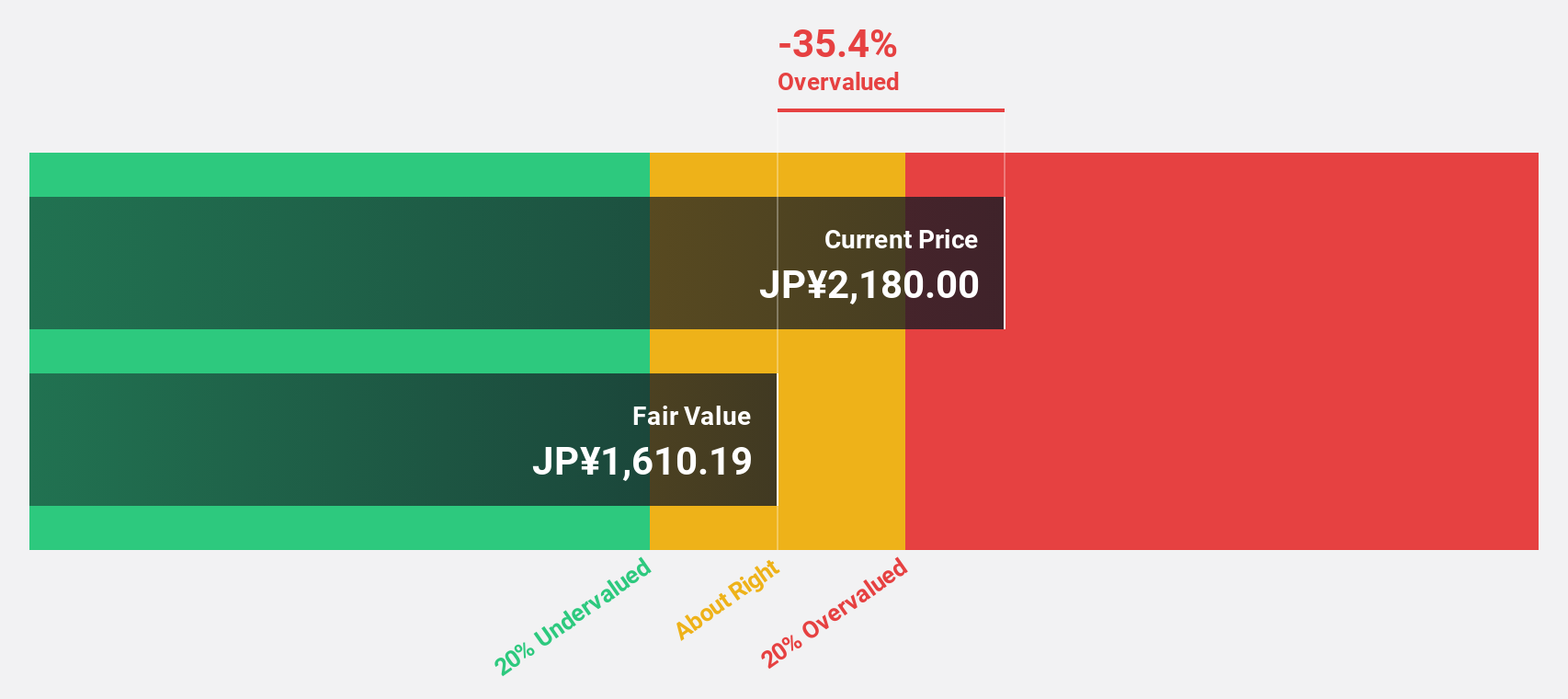

Premium Group (TSE:7199)

Overview: Premium Group Co., Ltd. provides financing and services worldwide, with a market cap of ¥78.61 billion.

Operations: The company's revenue segments include Finance at ¥19.20 billion, Failure Warranty at ¥8.15 billion, and Auto Mobility Service (including Car Premium Business) at ¥7.51 billion.

Estimated Discount To Fair Value: 38.4%

Premium Group, trading at ¥2075, is significantly undervalued with an estimated fair value of ¥3367.91 based on discounted cash flow analysis. Despite debt not being well-covered by operating cash flow, the company's earnings are expected to grow 19.46% annually, outpacing the JP market's 8.5%. Recent board decisions to dispose of treasury shares as restricted stock remuneration could impact future valuations but highlight strategic financial maneuvering aimed at long-term growth.

- The growth report we've compiled suggests that Premium Group's future prospects could be on the up.

- Get an in-depth perspective on Premium Group's balance sheet by reading our health report here.

Next Steps

- Gain an insight into the universe of 80 Undervalued Japanese Stocks Based On Cash Flows by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BayCurrent Consulting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6532

Flawless balance sheet with reasonable growth potential.