- Japan

- /

- Commercial Services

- /

- TSE:4384

3 Japanese Growth Companies With High Insider Ownership Growing Revenues Up To 15%

Reviewed by Simply Wall St

As Japan's stock markets experience a decline, with the Nikkei 225 and TOPIX indices both posting losses, investors are closely monitoring economic indicators such as easing domestic inflation and export trends. In this environment, companies with high insider ownership and robust revenue growth can be appealing to investors seeking stability and potential upside in uncertain times.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 31.5% |

| Hottolink (TSE:3680) | 26.1% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 40.2% |

| Medley (TSE:4480) | 34% | 30.4% |

| Inforich (TSE:9338) | 19.1% | 29.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 71.3% |

| AeroEdge (TSE:7409) | 10.7% | 25.3% |

| freee K.K (TSE:4478) | 23.9% | 74.1% |

Let's review some notable picks from our screened stocks.

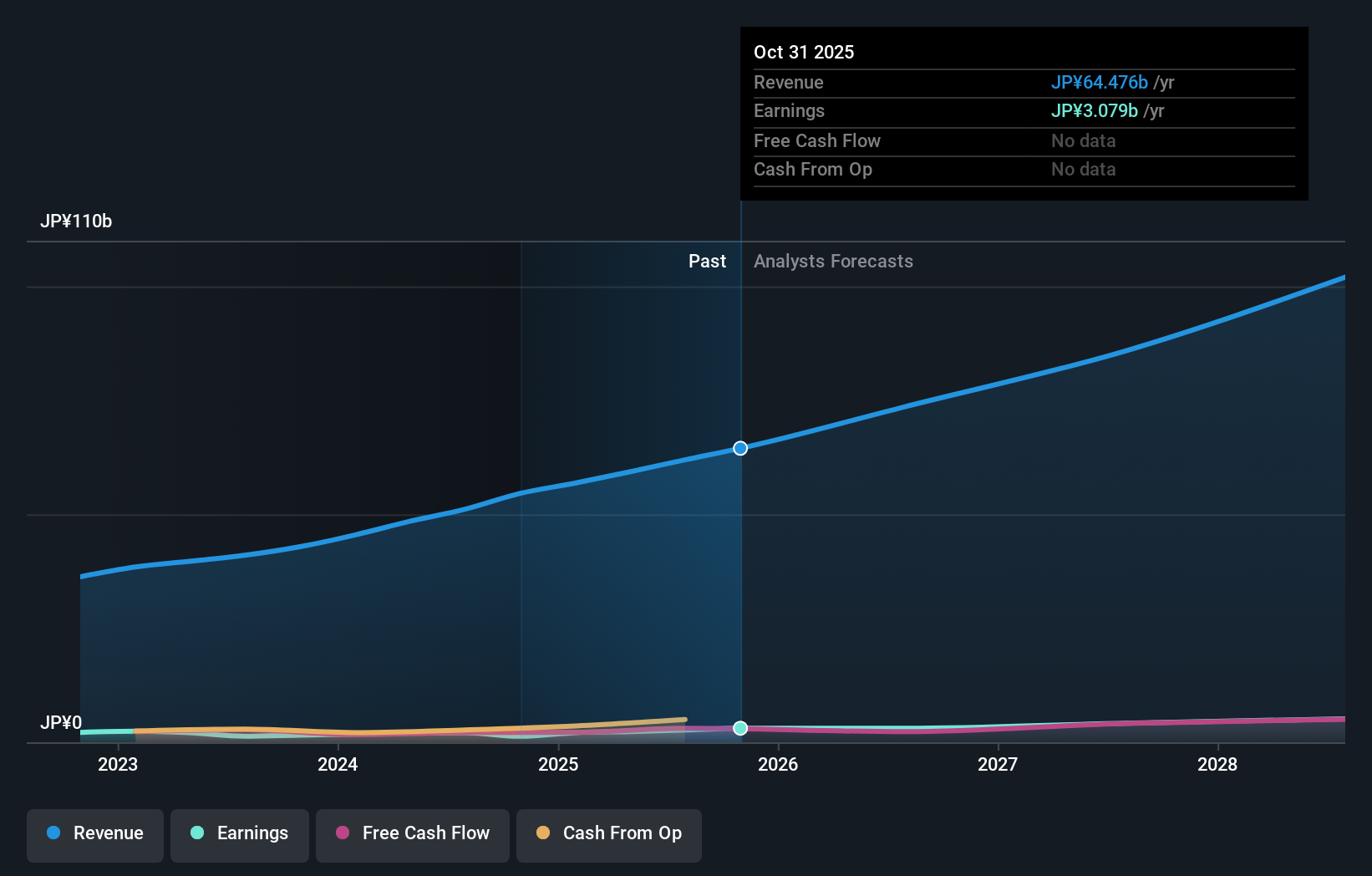

Raksul (TSE:4384)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Raksul Inc. operates in Japan, offering printing services, with a market capitalization of ¥74.56 billion.

Operations: The company's revenue is primarily derived from its Raxul segment at ¥47.11 billion and Novacell segment at ¥2.50 billion.

Insider Ownership: 14.2%

Revenue Growth Forecast: 13.5% p.a.

Raksul, a Japanese growth company, shows promising potential with earnings forecasted to grow significantly at 20.5% annually, outpacing the Japanese market average. Despite past shareholder dilution and recent share price volatility, Raksul's revenue is expected to rise faster than the market at 13.5% per year. The company announced a dividend increase to ¥1.70 per share from zero last year, reflecting confidence in its financial health and future prospects amidst ongoing corporate governance changes.

- Unlock comprehensive insights into our analysis of Raksul stock in this growth report.

- Upon reviewing our latest valuation report, Raksul's share price might be too optimistic.

Shima Seiki Mfg.Ltd (TSE:6222)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shima Seiki Mfg., Ltd., with a market cap of ¥39.77 billion, develops, manufactures, sells, markets, and services computerized flat knitting machines, automatic fabric cutting machines, glove and sock knitting machines, and design systems across Japan and globally.

Operations: The company's revenue segments include the development, production, sales, marketing, and servicing of computerized flat knitting machines, automatic fabric cutting machines, glove and sock knitting machines, and design systems across various regions including Japan, Europe, the Middle East, Asia, and other international markets.

Insider Ownership: 10.4%

Revenue Growth Forecast: 15.9% p.a.

Shima Seiki Mfg. Ltd. demonstrates growth potential with earnings forecasted to grow significantly at 65.6% annually, surpassing the Japanese market average of 4.2%. The company is expected to become profitable within three years, which is above average for the market. Despite a low forecasted return on equity of 2.5%, insider ownership remains stable with no substantial selling or buying activity reported recently, indicating confidence in its long-term prospects amidst moderate revenue growth expectations.

- Take a closer look at Shima Seiki Mfg.Ltd's potential here in our earnings growth report.

- Our valuation report here indicates Shima Seiki Mfg.Ltd may be overvalued.

Japan Elevator Service HoldingsLtd (TSE:6544)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Japan Elevator Service Holdings Co., Ltd. operates in Japan, offering repair, maintenance, and modernization services for elevators and escalators, with a market cap of ¥277.41 billion.

Operations: The company generates revenue primarily from its Maintenance Business, which accounts for ¥44.27 billion.

Insider Ownership: 22.4%

Revenue Growth Forecast: 11.8% p.a.

Japan Elevator Service Holdings Ltd. is poised for growth with earnings forecasted to increase by 18.5% annually, outpacing the Japanese market's average growth rate of 8.7%. Revenue is also expected to grow at 11.8% per year, above the market average of 4.2%. Despite not having significant insider trading activity recently, the company has expanded its domestic presence with new branches and service offices, enhancing its customer service capabilities and potentially supporting future growth initiatives.

- Click here and access our complete growth analysis report to understand the dynamics of Japan Elevator Service HoldingsLtd.

- The analysis detailed in our Japan Elevator Service HoldingsLtd valuation report hints at an inflated share price compared to its estimated value.

Summing It All Up

- Dive into all 102 of the Fast Growing Japanese Companies With High Insider Ownership we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4384

Reasonable growth potential with adequate balance sheet.