Advertisement

- Japan

- /

- Trade Distributors

- /

- TSE:8078

Hanwa (TSE:8078): Assessing Valuation Following Share Buyback Announcement

Simply Wall St

Reviewed by Simply Wall St

Hanwa (TSE:8078) just unveiled plans for a share repurchase program, aiming to buy back 1,000,000 shares, or about 3% of its share capital, by September 2026. This move highlights a clear focus on boosting shareholder value and improving capital efficiency.

See our latest analysis for Hanwa.

Hanwa's stock has been steadily gaining momentum, with a 37.7% share price return year-to-date, capped off by the company’s buyback announcement, which has likely boosted confidence among investors. Even more impressive, the total shareholder return over the past year sits at nearly 46%, and over five years shareholders have enjoyed a 239% gain. These are clear signs that both sentiment and long-term value creation are trending higher.

If Hanwa's latest move got you thinking about other promising opportunities, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

But with momentum running high, does Hanwa's recent buyback mean the stock remains undervalued, or is the market already pricing in the company's growth potential? Could there still be a buying opportunity here?

Price-to-Earnings of 6.4x: Is it justified?

Hanwa currently trades at a price-to-earnings (P/E) ratio of 6.4x, which signals the stock is valued at a significant discount compared with both its peers and the broader industry. The last close was ¥6,770, highlighting the gap between its market value and what typical multiples might suggest.

The P/E ratio measures how much investors are willing to pay today for a company’s earnings. This is particularly relevant for Hanwa given its solid profitability and role within the trade distributors sector, where P/E multiples are a key yardstick for valuation.

Compared to the Japanese Trade Distributors industry average P/E of 10.1x and a peer group average of 12x, Hanwa’s lower multiple stands out. The company’s P/E is also significantly below the estimated fair P/E ratio of 13.9x, pointing to the potential for a market revaluation if conditions align more closely with sector norms.

Explore the SWS fair ratio for Hanwa

Result: Price-to-Earnings of 6.4x (UNDERVALUED)

However, slowing revenue and modest profit growth could challenge expectations, particularly if broader industry or economic headwinds emerge in the coming quarters.

Find out about the key risks to this Hanwa narrative.

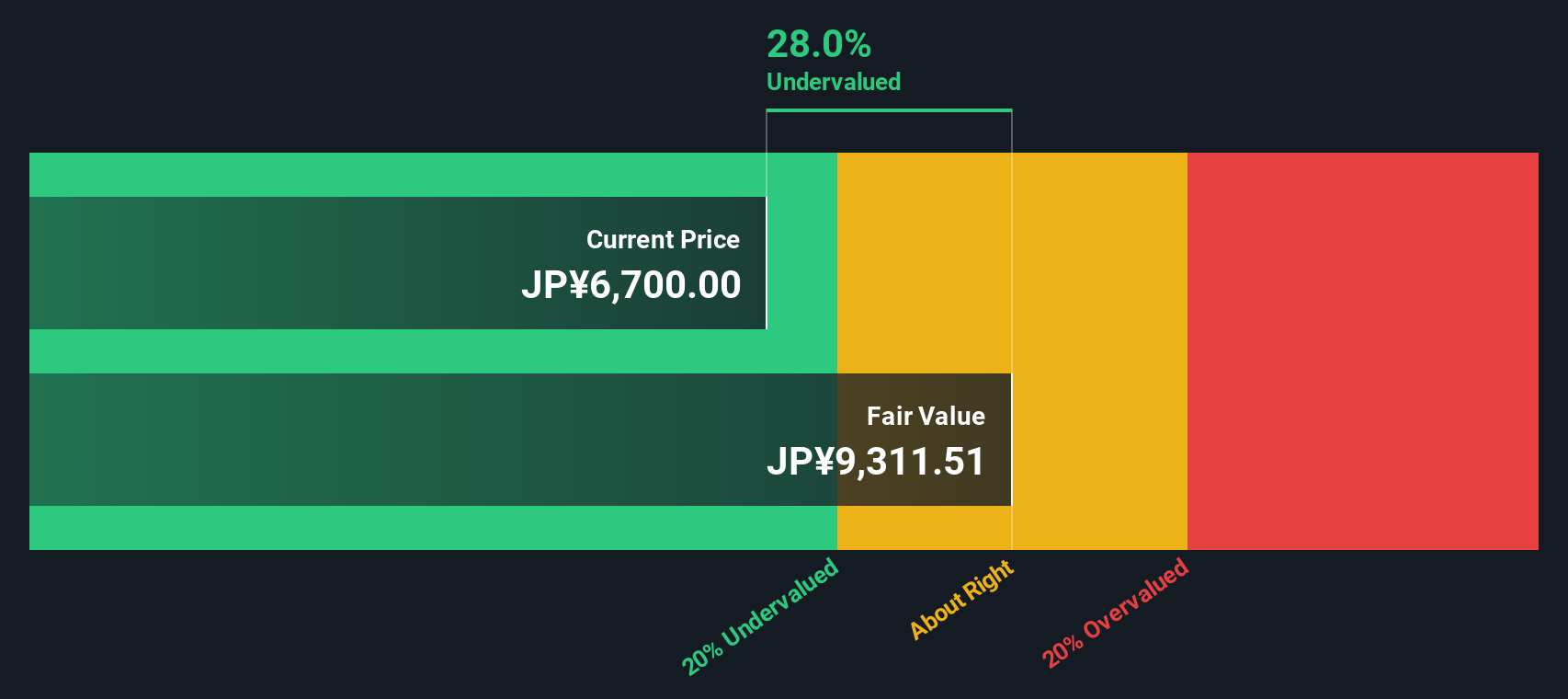

Another View: SWS DCF Model Suggests Even Greater Undervaluation

While Hanwa’s price-to-earnings ratio looks attractive, our DCF model takes a more holistic approach by estimating the company’s future cash flows. According to this method, Hanwa trades 27.1% below its estimated fair value. This hints at a potentially deeper undervaluation. Could traditional multiples be missing something?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hanwa for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hanwa Narrative

If you see things differently or want to dive into the details yourself, you can shape your own view of Hanwa’s outlook in just a few minutes: Do it your way

A great starting point for your Hanwa research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for one opportunity. Take charge of your next move and tap into new trends that could transform your portfolio with these handpicked selections:

- Target dependable returns and consistent income by exploring these 14 dividend stocks with yields > 3% that offer yields above 3% and support sturdy portfolio growth.

- Catch the surge in healthcare innovation by reviewing these 32 healthcare AI stocks, which are at the forefront of medical technology powered by artificial intelligence.

- Spot emerging tech trailblazers by starting with these 3589 penny stocks with strong financials known for strong financials and high-growth potential before they hit the mainstream.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanwa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8078

Hanwa

Trades in steel bars, construction works, steel plates, special steel, wire rods, steel pipes, and other products in Japan and internationally.

Undervalued established dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor