Advertisement

- Japan

- /

- Construction

- /

- TSE:7377

DN HoldingsLtd (TSE:7377) Might Be Having Difficulty Using Its Capital Effectively

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Having said that, from a first glance at DN HoldingsLtd (TSE:7377) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for DN HoldingsLtd:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

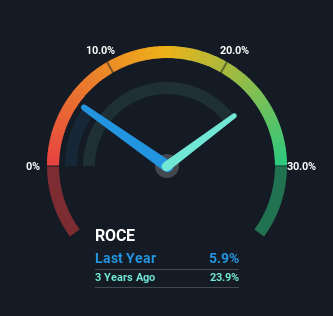

0.059 = JP¥820m ÷ (JP¥29b - JP¥15b) (Based on the trailing twelve months to March 2024).

So, DN HoldingsLtd has an ROCE of 5.9%. Ultimately, that's a low return and it under-performs the Construction industry average of 7.9%.

See our latest analysis for DN HoldingsLtd

Historical performance is a great place to start when researching a stock so above you can see the gauge for DN HoldingsLtd's ROCE against it's prior returns. If you're interested in investigating DN HoldingsLtd's past further, check out this free graph covering DN HoldingsLtd's past earnings, revenue and cash flow.

What Can We Tell From DN HoldingsLtd's ROCE Trend?

On the surface, the trend of ROCE at DN HoldingsLtd doesn't inspire confidence. Over the last five years, returns on capital have decreased to 5.9% from 20% five years ago. However it looks like DN HoldingsLtd might be reinvesting for long term growth because while capital employed has increased, the company's sales haven't changed much in the last 12 months. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

On a related note, DN HoldingsLtd has decreased its current liabilities to 52% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE. Either way, they're still at a pretty high level, so we'd like to see them fall further if possible.

Our Take On DN HoldingsLtd's ROCE

Bringing it all together, while we're somewhat encouraged by DN HoldingsLtd's reinvestment in its own business, we're aware that returns are shrinking. Yet to long term shareholders the stock has gifted them an incredible 174% return in the last five years, so the market appears to be rosy about its future. However, unless these underlying trends turn more positive, we wouldn't get our hopes up too high.

On a final note, we found 5 warning signs for DN HoldingsLtd (1 doesn't sit too well with us) you should be aware of.

While DN HoldingsLtd isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7377

DN HoldingsLtd

Engages in the construction consulting and geological survey businesses in Japan.

Solid track record established dividend payer.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor