Fanuc (TSE:6954) shares just ended the week slightly lower, dipping 1% over the past day. This move follows ongoing market conversations around the industrial automation sector, with investors reassessing recent performance trends for the company.

Fanuc's share price has seen some ups and downs lately, with a 1.2% dip today following a steeper fall earlier in the week. However, the bigger picture remains positive as the stock has delivered a 17.4% share price return year-to-date and a solid 1-year total shareholder return of 20.6%. This combination of short bursts of volatility and resilient long-term gains suggests investor sentiment is generally constructive but sensitive to shifts in the automation sector outlook.

If this renewed momentum in automation stocks has you rethinking what’s next, it might be the perfect moment to explore See the full list for free.

With Fanuc’s shares hovering around recent highs and fundamentals pointing to steady gains, the question becomes clear: is there more value to unlock here, or is the current price already factoring in the next stage of growth?

Advertisement

Price-to-Earnings of 28.4x: Is it justified?

Fanuc is trading at a price-to-earnings (P/E) ratio of 28.4x, indicating that the market is pricing in significant growth or premium quality compared to its peers. For context, the last close price was ¥4,797, while both industry and peer group average P/Es are notably lower.

The price-to-earnings ratio measures how much investors are willing to pay per yen of earnings and serves as a gauge of future expectations and perceived company strength. In the capital goods sector, a higher P/E often reflects confidence in earnings durability and market leadership.

Fanuc’s P/E of 28.4x is more than double the Japanese machinery industry average of just 12.4x and is also higher than peer firms at 22.6x. The estimated fair P/E for Fanuc is 25x, which means the current multiple exceeds the level justified by fundamentals and peer comparables. If the market consensus moves toward the fair ratio, Fanuc’s valuation could face reversion pressure.

However, slower revenue growth and limited upside to analyst price targets could challenge the bullish case if sector momentum fades or if expectations reset.

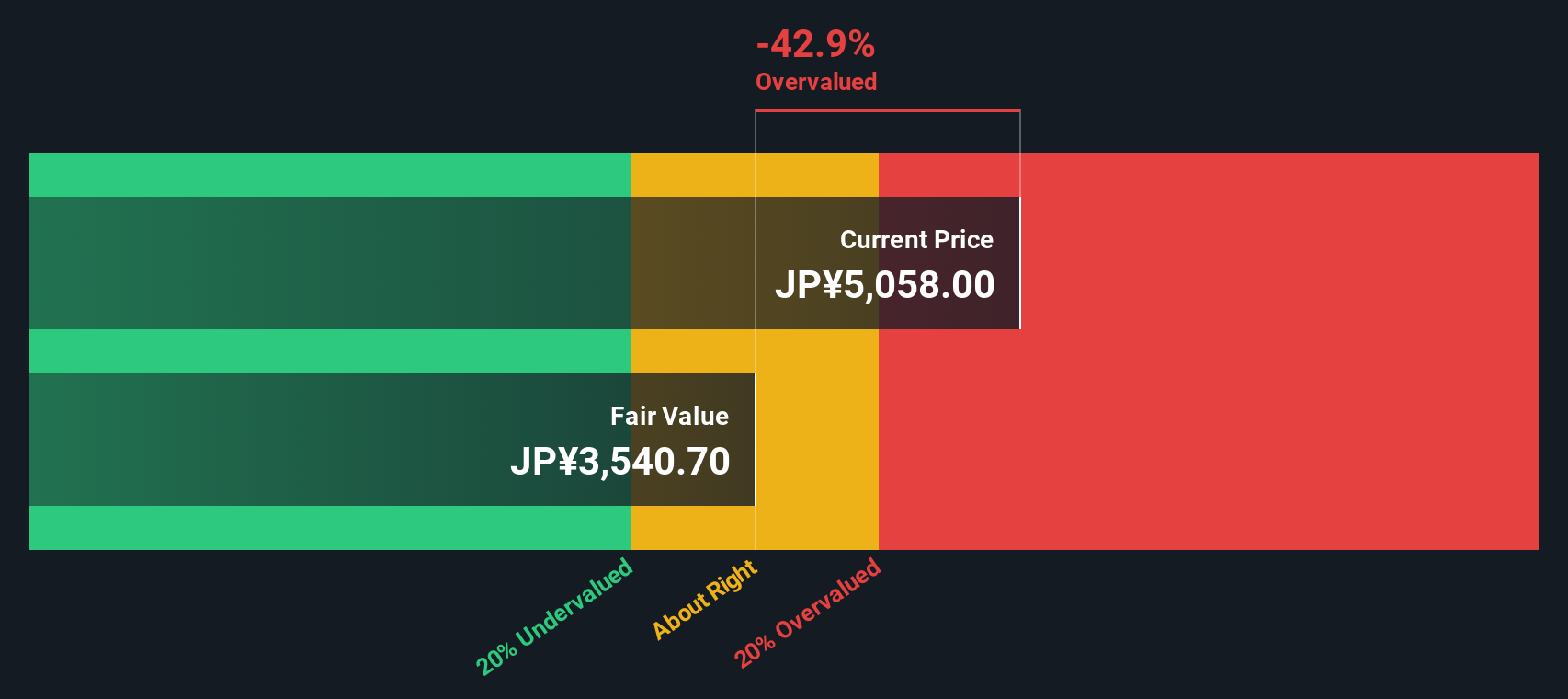

Looking from a different perspective, our SWS DCF model suggests Fanuc may be trading well above its estimated intrinsic value. Shares are at ¥4,797, compared to a fair value estimate of ¥3,609. This indicates a substantial premium, challenging the optimism priced into the current share price.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Fanuc for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 900 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Fanuc Narrative

If you want to reach your own conclusion or think a different angle deserves attention, you can craft your own view quickly with Do it your way

If you want to keep your edge, look beyond Fanuc. The market is loaded with standout opportunities, and missing them could cost you big gains. Here are three powerful ways to get ahead:

Tap into unstoppable income streams as you scan these 18 dividend stocks with yields > 3%, featuring stocks with yields greater than 3% to boost your returns with minimal effort.

Step into tomorrow’s tech leaders today by uncovering winners among these 27 AI penny stocks, shaping our digital future across every sector.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Engages in the development, manufacture, sale and maintenance services of products used in automated production systems in Japan, the United States, Europe, China, the rest of Asia, and internationally.