Advertisement

Analyst Estimates: Here's What Brokers Think Of THK Co., Ltd. (TSE:6481) After Its First-Quarter Report

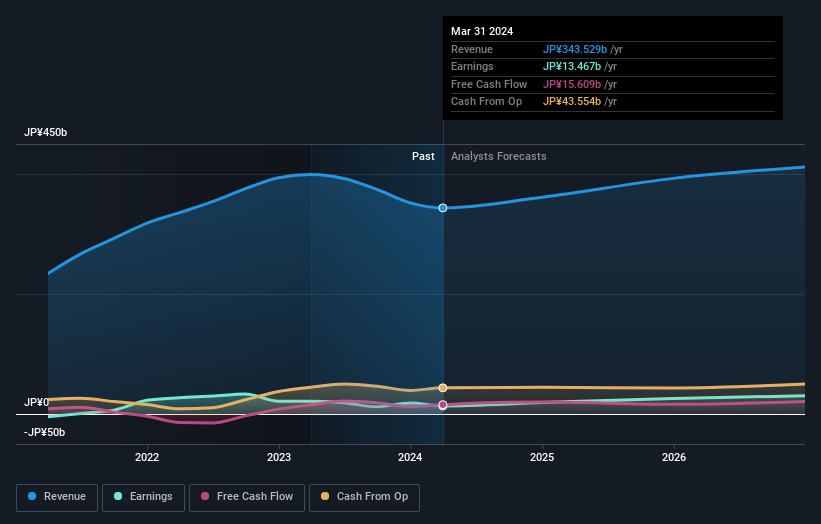

THK Co., Ltd. (TSE:6481) last week reported its latest quarterly results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. Results overall were respectable, with statutory earnings of JP¥150 per share roughly in line with what the analysts had forecast. Revenues of JP¥85b came in 4.2% ahead of analyst predictions. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for THK

Taking into account the latest results, the consensus forecast from THK's twelve analysts is for revenues of JP¥361.3b in 2024. This reflects a satisfactory 5.2% improvement in revenue compared to the last 12 months. Per-share earnings are expected to bounce 42% to JP¥156. Before this earnings report, the analysts had been forecasting revenues of JP¥359.6b and earnings per share (EPS) of JP¥156 in 2024. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

There were no changes to revenue or earnings estimates or the price target of JP¥3,644, suggesting that the company has met expectations in its recent result. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic THK analyst has a price target of JP¥4,200 per share, while the most pessimistic values it at JP¥2,400. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the THK's past performance and to peers in the same industry. The period to the end of 2024 brings more of the same, according to the analysts, with revenue forecast to display 6.9% growth on an annualised basis. That is in line with its 7.7% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 4.7% per year. So it's pretty clear that THK is forecast to grow substantially faster than its industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple THK analysts - going out to 2026, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 1 warning sign for THK that you need to be mindful of.

Valuation is complex, but we're here to simplify it.

Discover if THK might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6481

THK

Engages in the manufacture and sale of mechanical components worldwide.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor