Glory (TSE:6457) stock has quietly climbed 5% in the past month, building on nearly 50% returns over the past year. Investors have noticed its consistent annual revenue and net income growth, which has added some curiosity to the recent price moves.

Glory's share price momentum has certainly caught attention lately, with a robust 1-year total shareholder return of 49%, supported by recent steady gains and a solid run-up so far this year. All signs point to positive sentiment gathering pace as investors continue to reward consistent growth and improved performance.

With shares just shy of analyst targets but still trading at a notable intrinsic discount, the real question is whether Glory remains undervalued or if recent gains mean the market has already priced in future growth potential.

Advertisement

Price-to-Earnings of 17.7x: Is it justified?

Glory trades at a price-to-earnings (P/E) ratio of 17.7, making its valuation higher than the average for its peers, despite recent price appreciation. With shares recently closing at ¥3815, investors face a clear decision: does this higher earnings multiple still represent fair value in light of the firm’s growth profile?

The price-to-earnings ratio measures how much investors are willing to pay for each yen of net profit from Glory. This is important for capital goods companies because it factors in both past performance and expectations for future earnings quality and growth potential.

In Glory's case, the market appears to price in improving profitability, but possibly at a premium. Compared to its peers, which have an average P/E of 12.5, and the broader JP Machinery industry average of 13.6, Glory’s multiple looks elevated. However, when judged against its fair P/E estimate of 17.8, the market is currently valuing Glory right in line with fundamentals, suggesting price moves could follow further shifts in earnings.

However, slower revenue growth or an unexpected decline in net income could challenge the current positive outlook and affect Glory’s valuation trajectory.

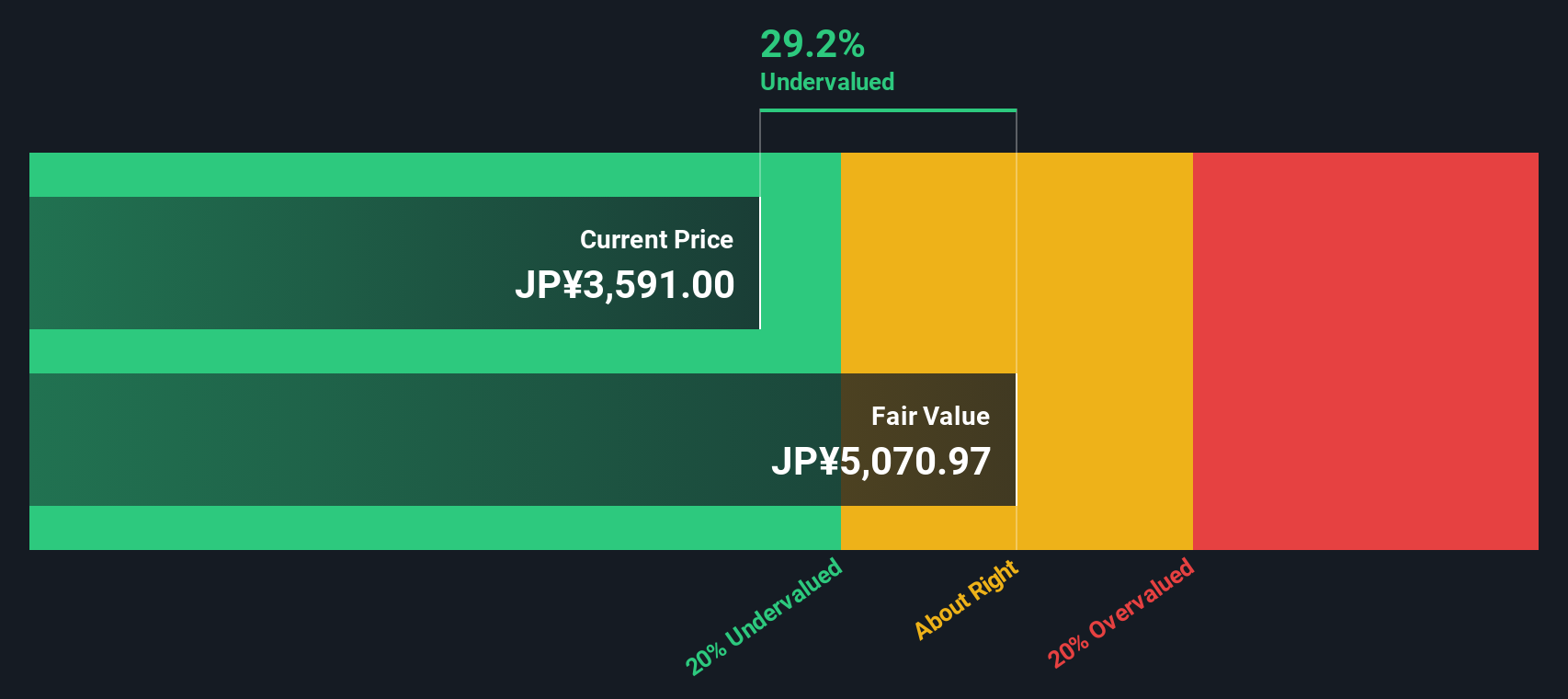

Taking a different approach, our DCF model suggests that Glory's shares are trading about 24% below its estimated fair value. This method weighs future cash flows instead of earnings multiples, pointing to a possible undervaluation from a fundamental perspective. Does this present a real opportunity, or is the market missing something?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Glory for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 874 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Glory Narrative

If you see things differently or want to dig deeper with your own research, you can put together your own story about Glory in just a few minutes with Do it your way.

Don’t leave your next portfolio win to chance. Uncover hidden opportunities and get ahead of market trends with Simply Wall Street’s expert-powered screeners.

Be among the first to tap breakthrough tech trends with these 24 AI penny stocks, where innovative companies are setting the pace for tomorrow’s success stories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks