Advertisement

Shareholders Will Be Pleased With The Quality of Howa Machinery's (TSE:6203) Earnings

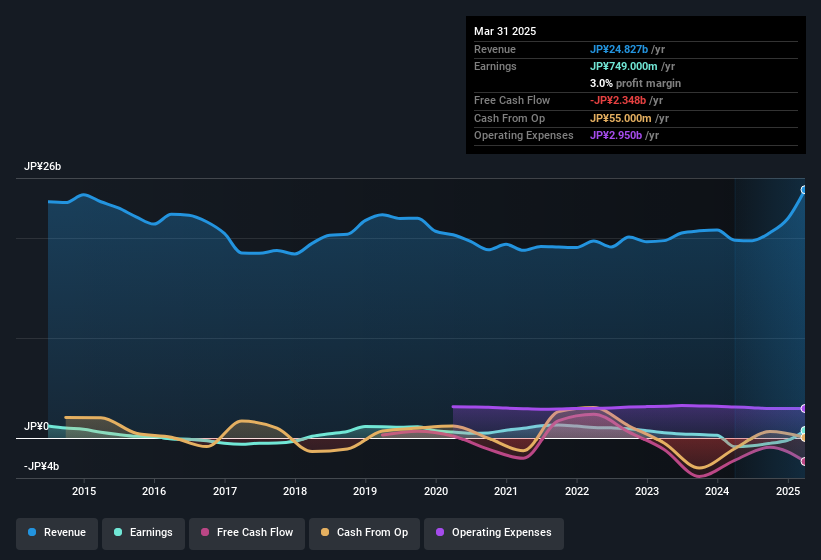

Howa Machinery, Ltd.'s (TSE:6203) earnings announcement last week was disappointing for investors, despite the decent profit numbers. We did some digging and actually think they are being unnecessarily pessimistic.

Our free stock report includes 4 warning signs investors should be aware of before investing in Howa Machinery. Read for free now.

How Do Unusual Items Influence Profit?

For anyone who wants to understand Howa Machinery's profit beyond the statutory numbers, it's important to note that during the last twelve months statutory profit was reduced by JP¥207m due to unusual items. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Howa Machinery to produce a higher profit next year, all else being equal.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Howa Machinery's Profit Performance

Unusual items (expenses) detracted from Howa Machinery's earnings over the last year, but we might see an improvement next year. Because of this, we think Howa Machinery's earnings potential is at least as good as it seems, and maybe even better! And it's also positive that the company showed enough improvement to book a profit this year, after losing money last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Be aware that Howa Machinery is showing 4 warning signs in our investment analysis and 2 of those are a bit concerning...

Today we've zoomed in on a single data point to better understand the nature of Howa Machinery's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Howa Machinery might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6203

Howa Machinery

Engages in the manufacture and sale of machine tools, pneumatic and hydraulic equipment, electronic machines, sweepers, metal joinery fittings, firearms, construction materials, and construction machinery in Japan.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor