Advertisement

Okuma (TSE:6103): Assessing Valuation After Fresh Earnings and Recent Share Price Pullback

Simply Wall St

Reviewed by Simply Wall St

Okuma (TSE:6103) shares are seeing fresh interest after the company posted annual results showing revenue growth and a jump in net income. Investors are now weighing these figures alongside the stock’s total return over the past several months.

See our latest analysis for Okuma.

Okuma’s share price has dipped nearly 6% over the past month, even as the company’s annual total shareholder return stands at a healthy 12%. That kind of longer-term performance, paired with recent upbeat earnings, suggests investors see solid growth potential but may be taking a brief pause to reassess after the latest rally.

If you’re interested in spotting momentum and ownership trends in other parts of the market, now is a great time to explore fast growing stocks with high insider ownership.

The next question is whether Okuma’s current price reflects its improved fundamentals, or if the recent pullback means there is still room for upside. Is this a buying opportunity, or has the market already priced in growth?

Price-to-Earnings of 19.4x: Is it justified?

Okuma trades at a price-to-earnings (P/E) ratio of 19.4x, a figure that is notably higher than both its industry and peer averages. With a last closing price of ¥3,390 and strong net income growth behind it, investors need to consider whether the market is pricing in sustained earnings momentum or simply running ahead of underlying fundamentals.

The price-to-earnings ratio shows how much investors are willing to pay per yen of current earnings. For machinery sector companies like Okuma, this multiple reflects expectations about the durability of profit growth, capital intensity, and competitive positioning in a cyclical industry.

Despite recent performance gains, Okuma's P/E is substantially more expensive than the Japanese Machinery industry average of 12.3x and the peer average of 13.7x. However, when compared to an estimated fair P/E of 20x, it is trading at a modest discount to what regression trends suggest could be justified if the company's positive earnings trajectory continues.

Explore the SWS fair ratio for Okuma

Result: Price-to-Earnings of 19.4x (ABOUT RIGHT)

However, softer revenue growth or a slowdown in net income acceleration could quickly alter the positive outlook that investors are pricing in right now.

Find out about the key risks to this Okuma narrative.

Another View: Discounted Cash Flow Model

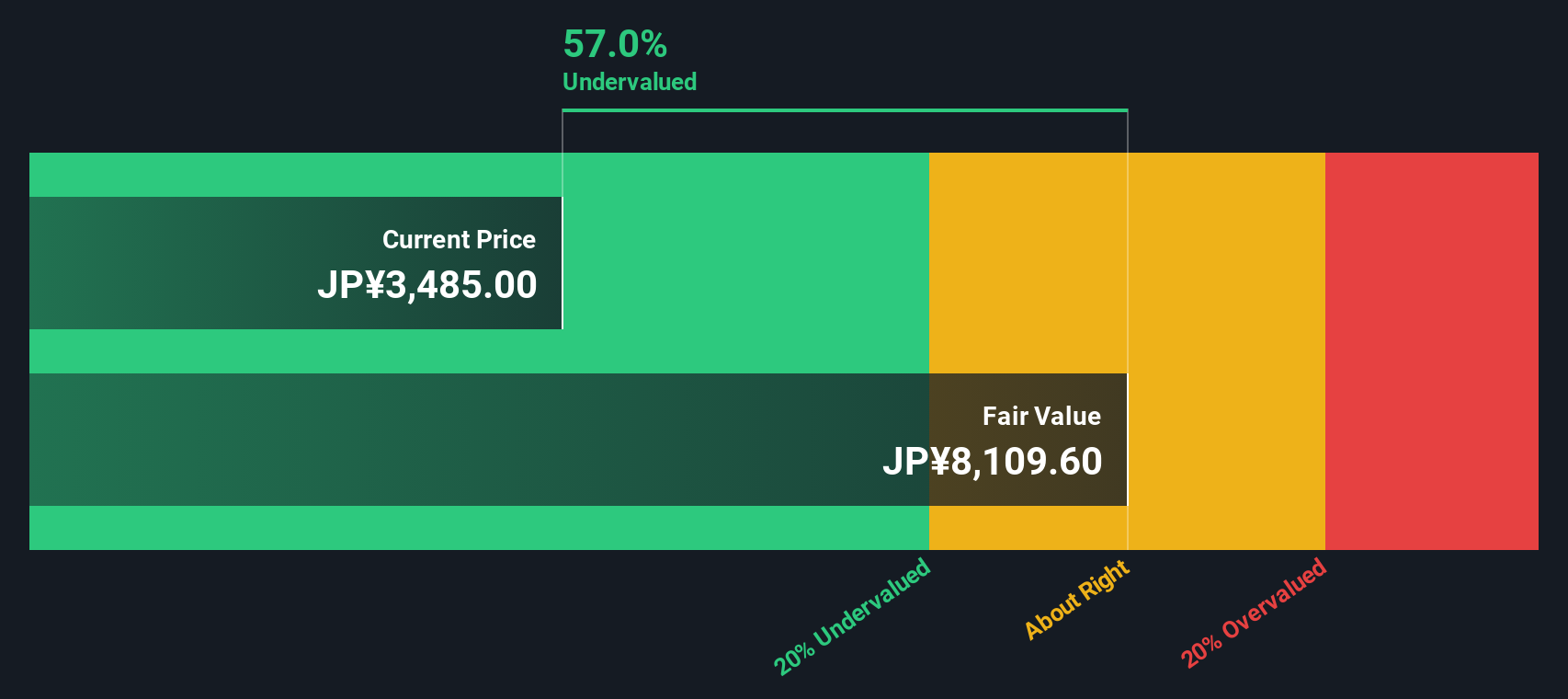

While the price-to-earnings ratio presents Okuma as fairly valued based on near-term earnings power, our SWS DCF model offers a notably different perspective. By estimating future cash flows, it suggests Okuma’s shares are trading at a 57.6% discount to fair value, implying significant undervaluation if those projections are realized. Which lens tells the fuller story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Okuma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 927 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Okuma Narrative

If you see the story differently or want to dig deeper into the numbers, you can easily build your own narrative in just a few minutes. Plus, Do it your way.

A great starting point for your Okuma research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t limit your strategy to just one company. Take your investing game further and tap into new opportunities that might be the next breakout winners.

- Capture income potential by checking out these 16 dividend stocks with yields > 3% with impressive yields above 3% in today's market.

- Accelerate your portfolio's edge by exploring these 26 AI penny stocks that are disrupting industries with cutting-edge artificial intelligence.

- Strengthen your long-term returns by targeting value with these 927 undervalued stocks based on cash flows chosen for their attractive pricing based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6103

Okuma

Manufactures and sells machine tools in Japan, the United States, Europe, and Asia/Pacific.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor