Advertisement

- Japan

- /

- Construction

- /

- TSE:1961

Exploring Undiscovered Gems With Potential In December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by mixed performances in major indexes and economic indicators, the spotlight has turned to small-cap stocks, particularly with the Russell 2000 Index experiencing a recent decline after outperforming larger-cap peers. In this environment, identifying undiscovered gems requires focusing on companies that demonstrate resilience and potential for growth amid diverse sector performances and evolving economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| SHL Consolidated Bhd | NA | 16.14% | 19.01% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Industrias del Cobre Sociedad Anónima | NA | 19.08% | 22.33% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| MAPFRE Middlesea | NA | 14.56% | 1.77% | ★★★★★☆ |

| Inverfal PerúA | 31.20% | 10.56% | 17.83% | ★★★★★☆ |

| Procimmo Group | 157.49% | 0.65% | 4.94% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| BOSQAR d.d | 94.35% | 39.99% | 23.94% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Johnson Electric Holdings (SEHK:179)

Simply Wall St Value Rating: ★★★★★★

Overview: Johnson Electric Holdings Limited is an investment holding company that manufactures and sells motion systems globally, with a market capitalization of HK$10.13 billion.

Operations: The primary revenue stream for Johnson Electric Holdings comes from its Auto Parts & Accessories segment, generating $3.73 billion. The company's net profit margin reflects its financial efficiency in managing costs relative to its revenue.

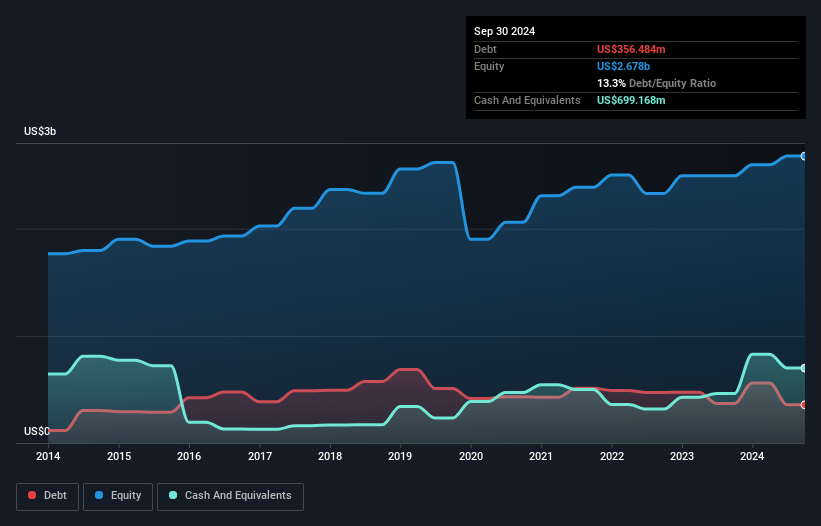

Johnson Electric, a smaller player in the auto components sector, showcases resilience with earnings growth of 7.5% over the past year, outpacing the industry's -19.9%. Its debt-to-equity ratio improved to 13.3% from 19.4% over five years, highlighting prudent financial management. Trading at a significant discount of 72% below its estimated fair value suggests potential upside for investors seeking undervalued opportunities. The company reported net income of US$129 million for H1 2024, up from US$120 million last year, while announcing an interim dividend of HKD0.17 per share payable in January 2025—demonstrating robust earnings quality and shareholder returns.

Qingdao Copton Technology (SHSE:603798)

Simply Wall St Value Rating: ★★★★★☆

Overview: Qingdao Copton Technology Company Limited focuses on the production and sale of lubricants and car care products in China, with a market capitalization of approximately CN¥2.45 billion.

Operations: The company's revenue primarily stems from its petrochemical segment, generating CN¥1.14 billion.

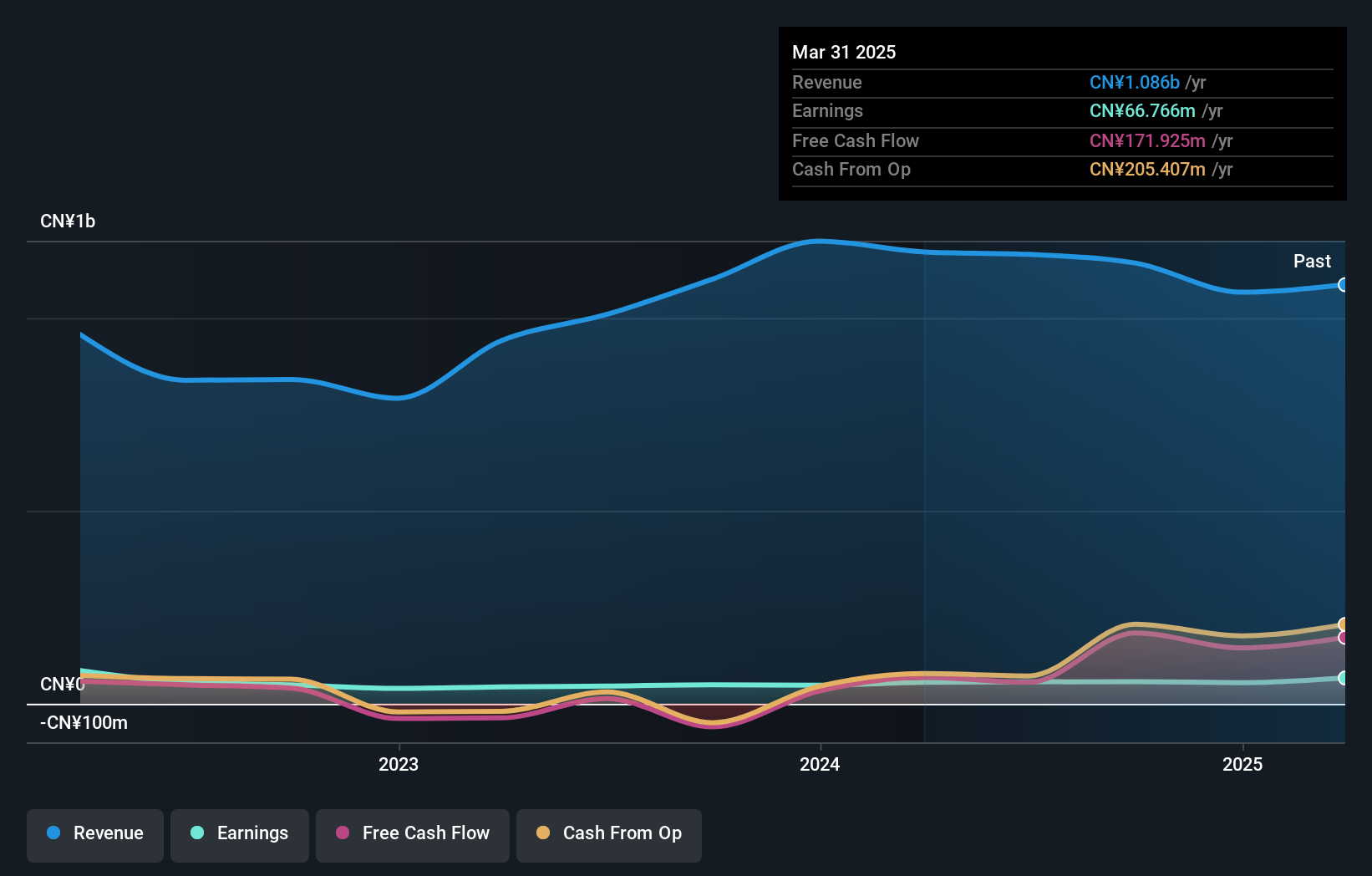

Qingdao Copton Technology, a nimble player in the chemicals industry, has shown resilience with a 16.9% earnings growth over the past year, outpacing the industry's -5%. Despite a drop in sales to CN¥844.46 million from CN¥901.29 million last year, net income rose to CN¥57.51 million compared to CN¥48.11 million previously, indicating efficient cost management or other factors at play. The company trades at an attractive valuation, being 81.7% below its estimated fair value and maintains more cash than total debt despite an increased debt-to-equity ratio of 2.5% over five years due to strategic investments or expansions likely impacting performance positively.

Sanki Engineering (TSE:1961)

Simply Wall St Value Rating: ★★★★★★

Overview: Sanki Engineering Co., Ltd. offers a range of social infrastructure services both in Japan and internationally, with a market capitalization of ¥152.67 billion.

Operations: Sanki Engineering generates revenue primarily from its Building Equipment Business, which accounts for ¥196.54 billion, followed by the Environmental Systems Business at ¥28.64 billion and the Machine System Business at ¥11.01 billion. The Real Estate Business contributes a smaller portion with ¥2.53 billion in revenue.

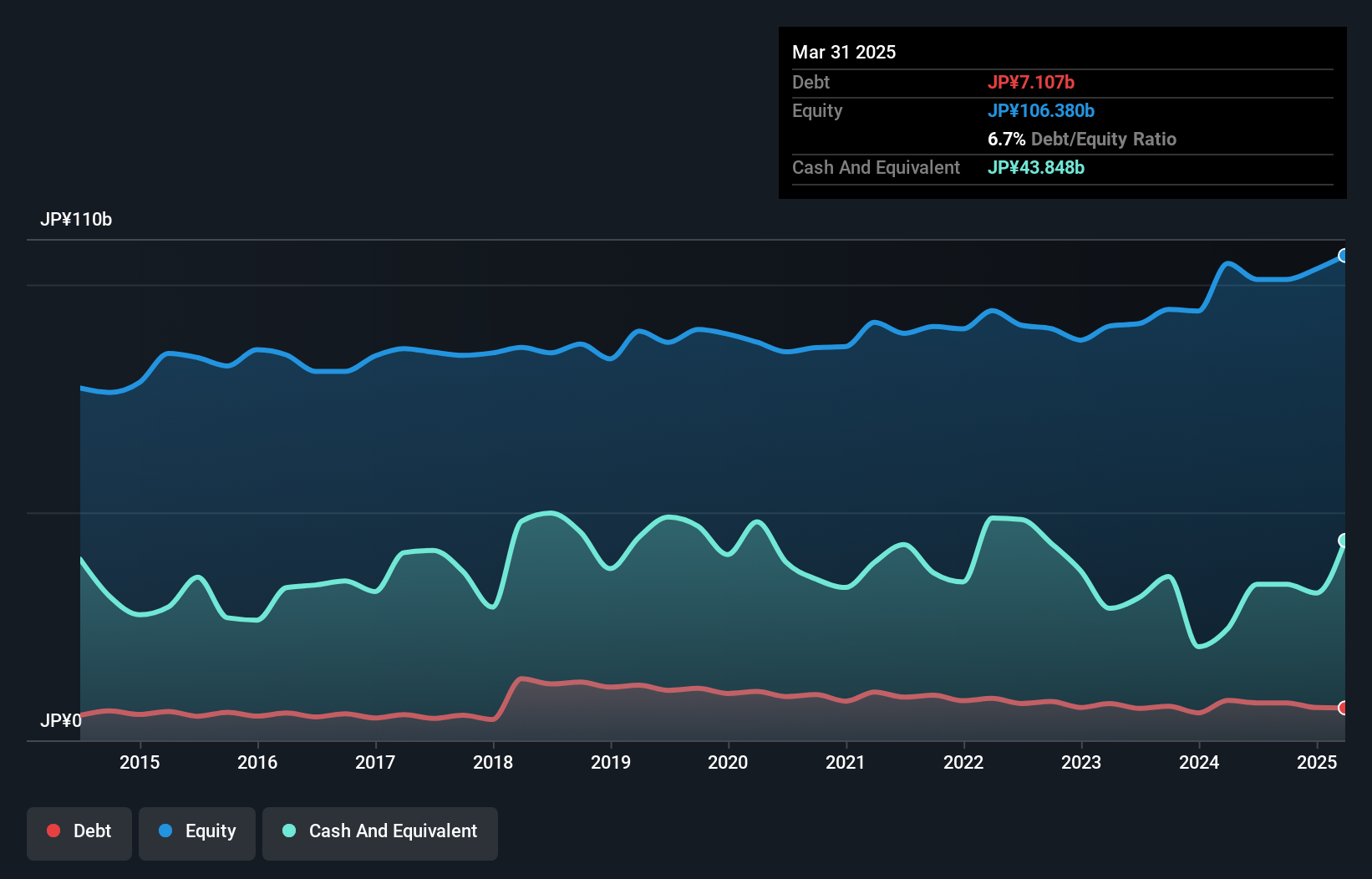

Sanki Engineering, a nimble player in its field, has been making waves with impressive earnings growth of 73% last year, outpacing the broader construction sector's 20%. Trading at nearly 26% below estimated fair value, it seems to offer potential upside. The company's debt profile is reassuring; cash exceeds total debt and the debt-to-equity ratio improved from 13% to 8% over five years. Recently, Sanki repurchased 118,000 shares for ¥263 million (US$1.8 million), indicating confidence in its valuation. With high-quality past earnings and projected annual growth of around 7%, Sanki appears poised for steady progress.

- Take a closer look at Sanki Engineering's potential here in our health report.

Assess Sanki Engineering's past performance with our detailed historical performance reports.

Make It Happen

- Explore the 4648 names from our Undiscovered Gems With Strong Fundamentals screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1961

Sanki Engineering

Provides various social infrastructure services in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor