Advertisement

- Taiwan

- /

- Construction

- /

- TPEX:7783

Discovering Hidden Gems with Potential In December 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by rate cuts from the ECB and SNB, and with the U.S. Federal Reserve poised for another potential cut, small-cap stocks have faced challenges, evidenced by the Russell 2000's recent underperformance compared to larger indices. Amidst these dynamics, investors often seek hidden gems—stocks that may be undervalued or overlooked but possess strong fundamentals or growth potential—to capitalize on opportunities in a shifting economic environment.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Cita Mineral Investindo | NA | -3.08% | 16.56% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Mandiri Herindo Adiperkasa | NA | 20.72% | 11.08% | ★★★★★★ |

| Citra Tubindo | NA | 11.06% | 31.01% | ★★★★★★ |

| Sure Global Tech | NA | 10.25% | 20.35% | ★★★★★★ |

| Nofoth Food Products | NA | 14.41% | 31.88% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| ShareHope Medicine | 38.07% | 3.80% | -7.16% | ★★★★★☆ |

| Standard Chartered Bank Kenya | 9.32% | 12.22% | 22.08% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Acter Group (TPEX:5536)

Simply Wall St Value Rating: ★★★★★☆

Overview: Acter Group Corporation Limited offers engineering services across Taiwan, Mainland China, and other Asian countries with a market capitalization of NT$44.23 billion.

Operations: The company's revenue is primarily derived from its operations in Mainland China (NT$12.95 billion) and Taiwan (NT$11.97 billion), with additional contributions from other Asian regions (NT$3.09 billion).

Acter Group, a promising player in the construction industry, has shown notable financial strides. Recent earnings reveal a net income of TWD 628 million for Q3 2024, up from TWD 508 million the previous year. Revenue also increased to TWD 7.62 billion from TWD 6.46 billion year-on-year, indicating strong growth momentum. The company is trading at an attractive valuation, about 51% below its estimated fair value, and boasts high-quality past earnings with a recent growth rate of 7%. Additionally, Acter has secured a significant contract worth TWD 517 million with SPIL for facility engineering services through December 2025.

- Navigate through the intricacies of Acter Group with our comprehensive health report here.

Gain insights into Acter Group's past trends and performance with our Past report.

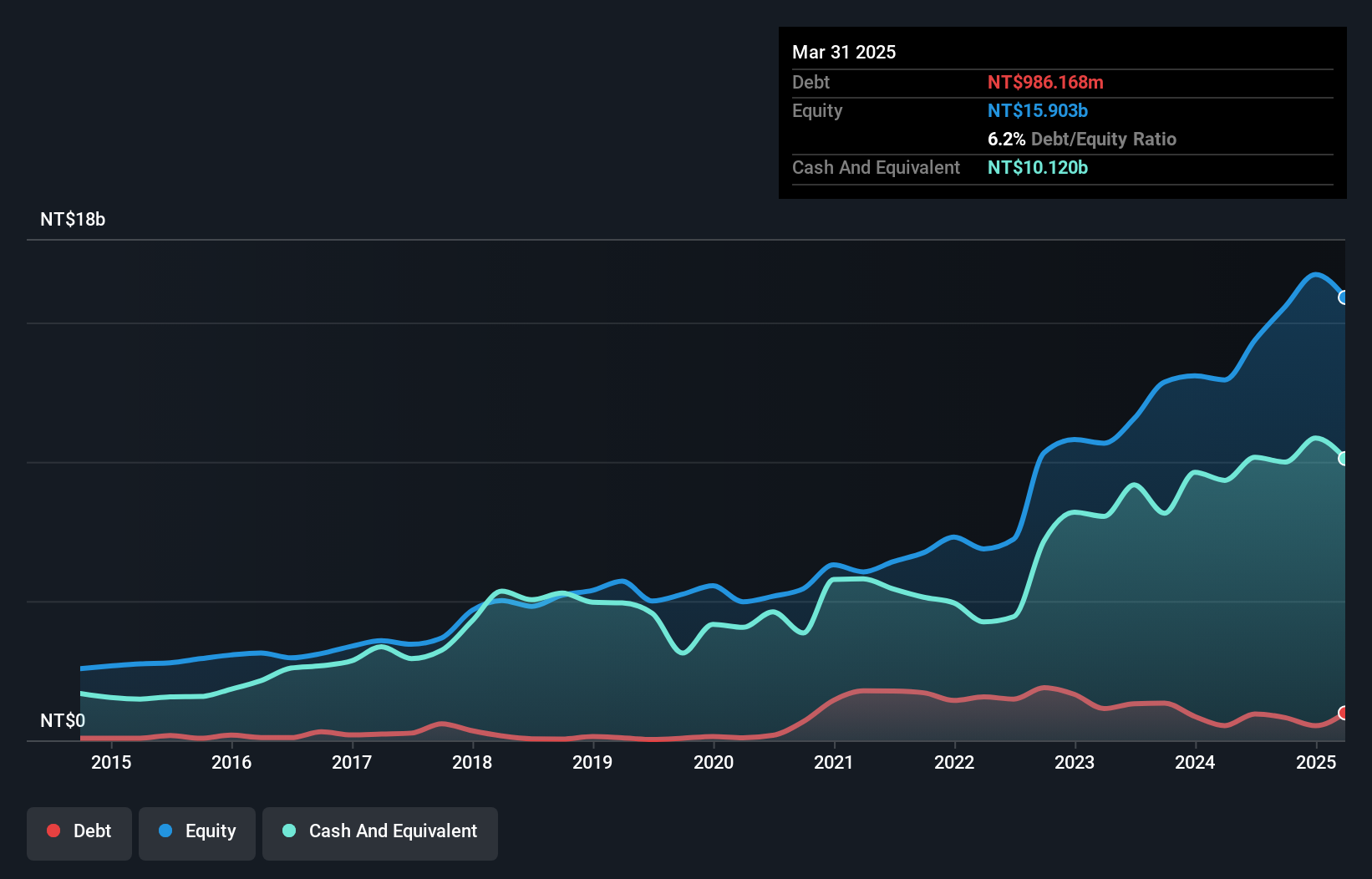

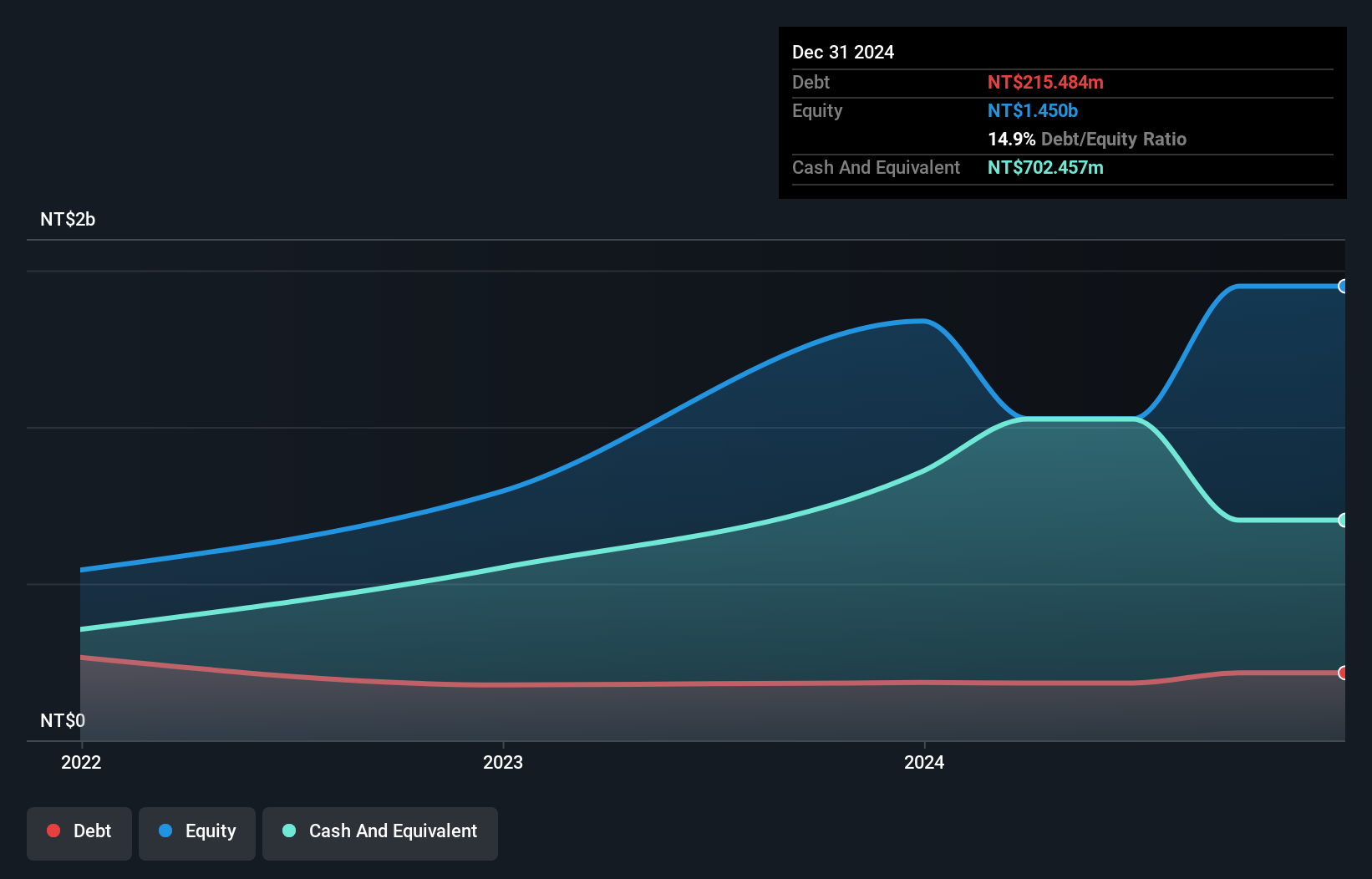

Giant Heavy Machinery Service (TPEX:7783)

Simply Wall St Value Rating: ★★★★★☆

Overview: Giant Heavy Machinery Service Corporation offers transportation equipment contracting services in Taiwan and has a market capitalization of NT$13.30 billion.

Operations: The primary revenue stream for Giant Heavy Machinery Service Corporation is from transportation and lifting services, generating NT$1.48 billion.

Giant Heavy Machinery Service, a nimble player in its industry, is trading at 46.7% below its estimated fair value, suggesting potential undervaluation. The company's earnings have surged by 48.8% over the past year, outpacing the construction sector's -4.6%. Its interest payments are comfortably covered by EBIT at an impressive 471 times coverage. Despite having more cash than total debt, share price volatility has been notable recently. With high-quality earnings and positive free cash flow reported as of June 2024 (A$440 million), it seems positioned for potential growth amidst market fluctuations and industry challenges.

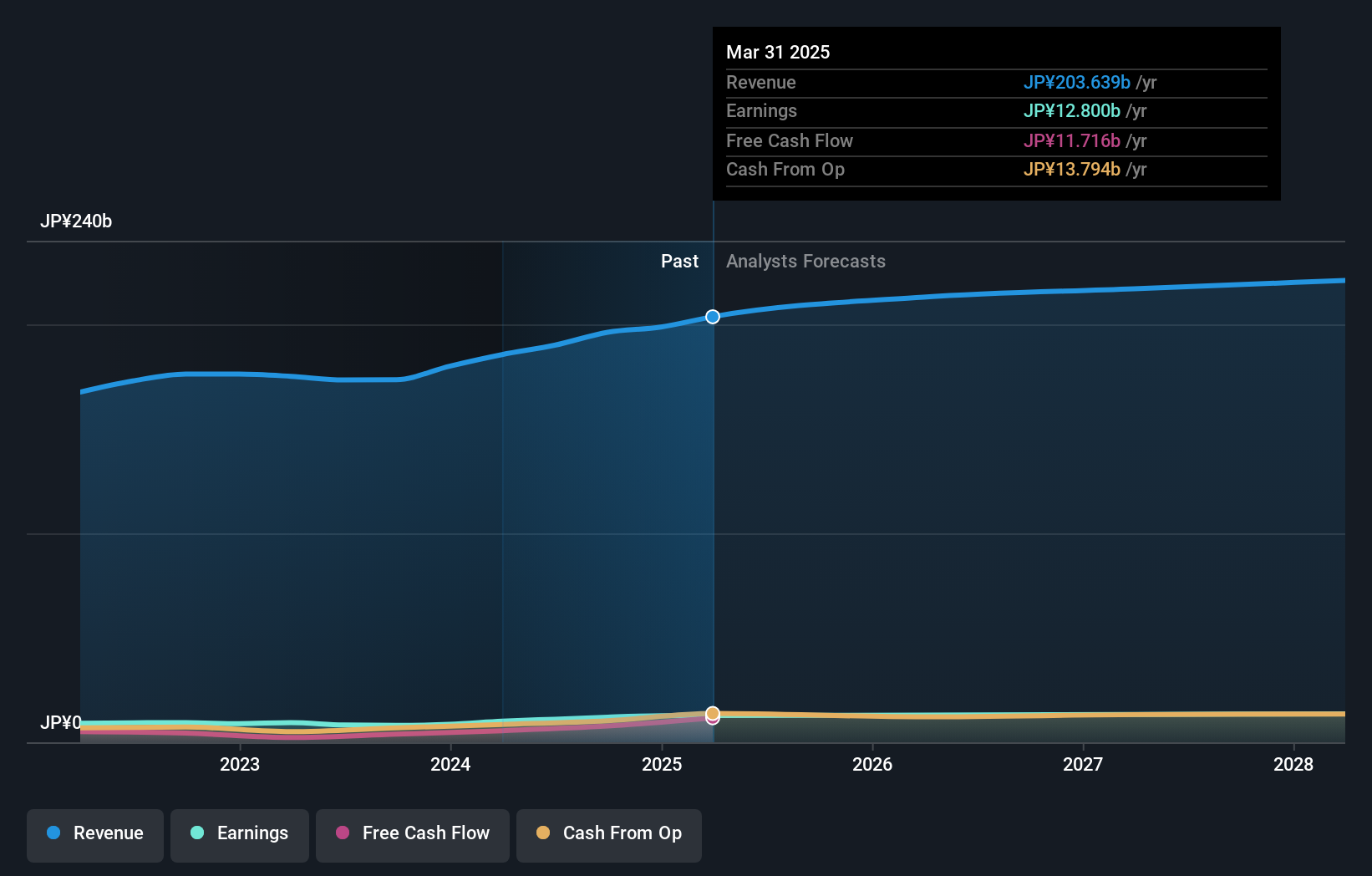

Sumitomo DensetsuLtd (TSE:1949)

Simply Wall St Value Rating: ★★★★★★

Overview: Sumitomo Densetsu Co., Ltd., with a market cap of ¥168.67 billion, operates as a construction company through its subsidiaries in Japan and several countries across Southeast Asia, including Indonesia, Thailand, Cambodia, Myanmar, the Philippines, China, and Malaysia.

Operations: Sumitomo Densetsu generates revenue primarily from its Utilities Engineering Service segment, which accounted for ¥189.22 billion. The company's market cap stands at ¥168.67 billion.

Sumitomo Densetsu, a player in the construction industry, has shown impressive earnings growth of 49% over the past year, outpacing the industry's 20%. The company boasts high-quality earnings and a debt-to-equity ratio that has improved from 4% to 2.1% over five years. With more cash than total debt, its financial health seems robust. Recent guidance anticipates net sales of ¥200 billion and an operating profit of ¥15.5 billion for fiscal year ending March 2025. Additionally, dividends increased to ¥60 per share this quarter from last year's ¥47, indicating shareholder-friendly policies amidst stable performance projections.

- Delve into the full analysis health report here for a deeper understanding of Sumitomo DensetsuLtd.

Explore historical data to track Sumitomo DensetsuLtd's performance over time in our Past section.

Summing It All Up

- Click here to access our complete index of 4622 Undiscovered Gems With Strong Fundamentals.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:7783

Giant Heavy Machinery Service

Provides transportation equipment contracting services in Taiwan.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor