Advertisement

- Japan

- /

- Construction

- /

- TSE:1833

A Look at Okumura (TSE:1833) Valuation Following Upgraded Earnings Outlook and Dividend Boost

Simply Wall St

Reviewed by Simply Wall St

Okumura (TSE:1833) just raised its full-year earnings outlook, citing stronger operating results from the construction business and improved plans for selling investment securities. The company also announced a higher full-year dividend projection.

See our latest analysis for Okumura.

Okumura’s upbeat profit revision appears to have caught the market’s attention, with the stock surging 17.9% over the past month and posting a total shareholder return of 55.8% in the last year. With several positive developments, including higher dividend projections and an earnings upgrade, recent momentum suggests growing optimism about the company’s growth outlook and financial resilience.

If you’re looking to sharpen your watchlist with stocks showing similar momentum, now might be a great time to discover fast growing stocks with high insider ownership.

But with shares up nearly 18% in the past month and the outlook recently upgraded, the big question remains: is Okumura still undervalued, or has the market already priced in its expected growth?

Price-to-Earnings of 16.2x: Is it justified?

Okumura is currently trading at a price-to-earnings (P/E) ratio of 16.2, notably higher than both its direct competitors and the sector average. With the last close at ¥5,860, this multiple signals the market's willingness to pay a premium for Okumura's recent momentum. However, it puts its valuation above peers.

The price-to-earnings ratio is one of the most widely used tools for valuing stocks, especially in the construction sector where consistent profits are key. A higher P/E can sometimes reflect expected future growth or resilience, but it can also indicate that investors are paying up for performance that may not be sustained.

Currently, Okumura's P/E (16.2x) is above the peer average (13.2x) and well above the construction industry average in Japan (11.7x). This sharp difference suggests investor optimism and also signals higher expectations built into the share price compared to comparable companies.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 16.2x (OVERVALUED)

However, risks such as future profit margins failing to meet high expectations, or broader sector pressures, could quickly reduce current investor enthusiasm.

Find out about the key risks to this Okumura narrative.

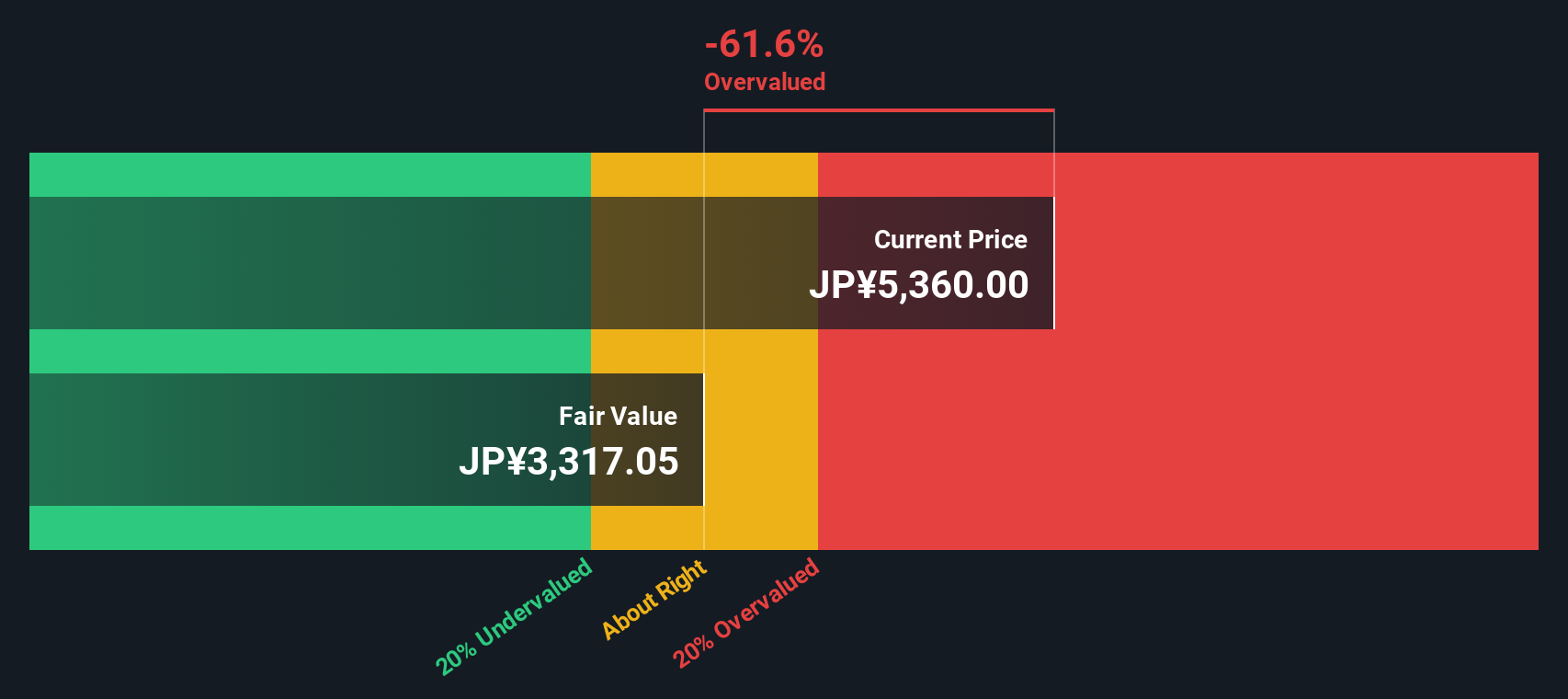

Another View: Discounted Cash Flow Points to Big Upside

While Okumura's current share price looks high compared to earnings-based multiples, our DCF model tells a different story. According to this method, the company may be trading well below its estimated fair value. Could market momentum be overlooking deeper value, or is the risk factored in for a reason?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Okumura for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Okumura Narrative

If you have a different perspective or want to dig deeper into Okumura's numbers, you can build your own narrative in just a few minutes. Do it your way.

A great starting point for your Okumura research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let opportunity pass you by. Equip yourself with fresh investment options that go beyond the headlines and fit your own strategy today.

- Secure long-term income and stability by considering these 17 dividend stocks with yields > 3% offering yields above 3% from established businesses.

- Unlock the potential of emerging technology by scanning these 25 AI penny stocks powering artificial intelligence innovation and transformative breakthroughs.

- Capitalize on market optimism and strong fundamentals with these 917 undervalued stocks based on cash flows currently trading below their estimated values based on future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1833

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor