Advertisement

- Japan

- /

- Construction

- /

- TSE:1820

Nishimatsu Construction (TSE:1820): Valuation Insights Following Updated FY26 Guidance and Real Estate Profit Boost

Simply Wall St

Reviewed by Simply Wall St

Nishimatsu Construction (TSE:1820) updated its earnings guidance for the year ending March 2026, revealing lower expected net sales because of overseas project delays. At the same time, improved profits from its real estate business are boosting the overall profit outlook.

See our latest analysis for Nishimatsu Construction.

After a generally steady run this year, Nishimatsu Construction’s latest guidance revision has injected some energy into the share price. The stock climbed 2.55% in the past day and 6.35% over the last month. With a robust 17.2% total shareholder return over the past year and an impressive 269.7% total return over five years, momentum has clearly been building. This reflects evolving investor confidence as profit forecasts improve despite overseas headwinds.

If this positive trend has you thinking about what else is gaining ground, it’s a great time to explore fast growing stocks with high insider ownership.

But with stronger profit forecasts helping lift the stock amid sales uncertainty, investors may wonder if Nishimatsu Construction shares are undervalued at today’s price or if the market has already factored in this improved outlook and real estate gains.

Price-to-Earnings of 12.2x: Is it justified?

Nishimatsu Construction is trading at a Price-to-Earnings (P/E) multiple of 12.2x, which makes it appear moderately valued against its most direct peers, based on the last close of ¥5,540.

The P/E multiple reflects how much investors are willing to pay today for ¥1 of the company's current earnings. For construction companies, this is a key benchmark because earnings can swing sharply with project cycles. P/E highlights what the market expects for future profit consistency and growth.

Currently, Nishimatsu’s P/E of 12.2x is above the Japanese Construction industry average of 11.6x. This suggests the market is pricing in stronger prospects than the sector norm. However, compared to the peer group average of 14.7x and an estimated fair Price-to-Earnings ratio of 13.7x, the shares look attractively valued and may have room to rerate higher if the improved profit outlook persists.

Explore the SWS fair ratio for Nishimatsu Construction

Result: Price-to-Earnings of 12.2x (UNDERVALUED)

However, overseas project setbacks or a reversal in real estate profitability could challenge the current momentum and could weigh on future returns.

Find out about the key risks to this Nishimatsu Construction narrative.

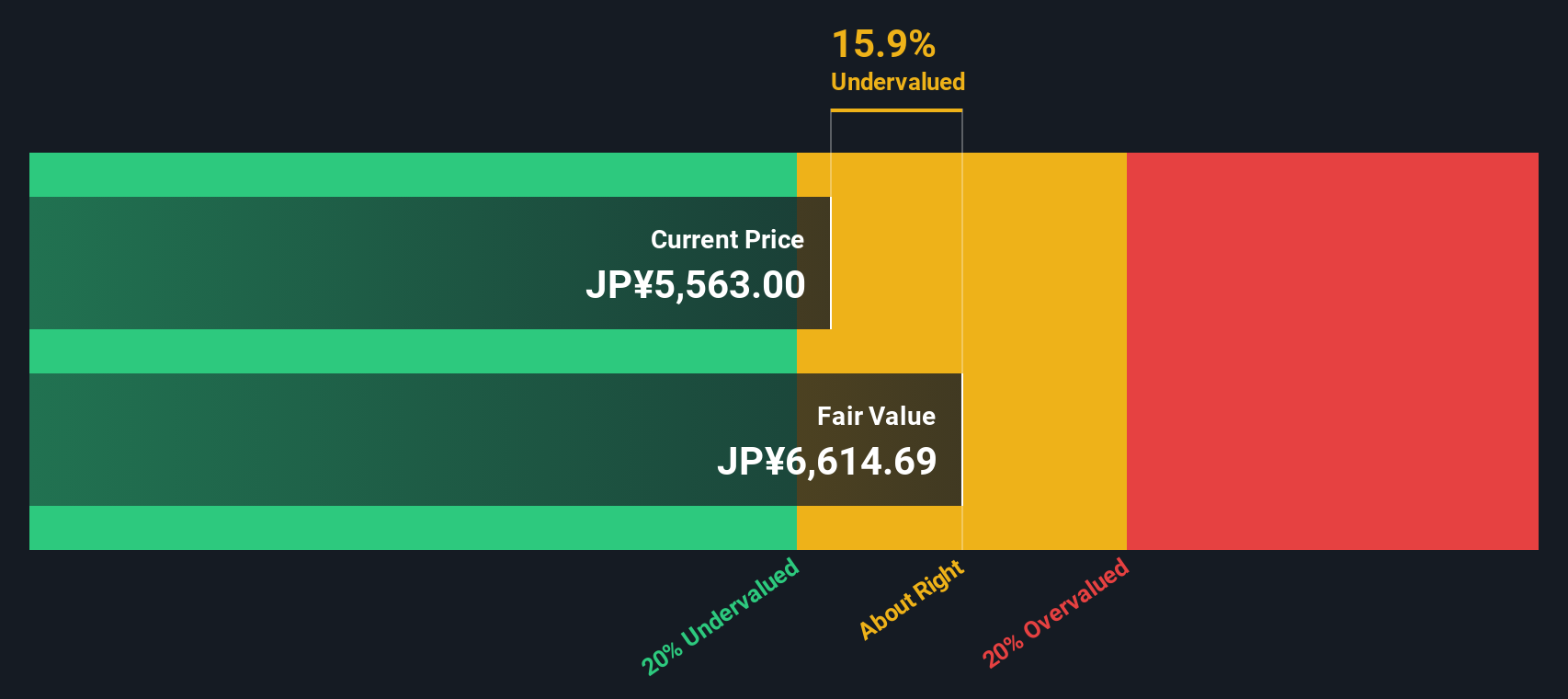

Another View: What Does the SWS DCF Model Say?

While the P/E ratio analysis hints that Nishimatsu Construction may be undervalued, our SWS DCF model provides a different perspective. It estimates a fair value of ¥6,575.61 per share. This suggests the current price is trading about 15.7% below intrinsic value. Is the market underappreciating the company’s long-term cashflows or simply staying cautious?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nishimatsu Construction for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 916 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Nishimatsu Construction Narrative

If you want to check the data on your own terms or find a different angle in the numbers, you can build your own story in just a few minutes, your way with Do it your way.

A great starting point for your Nishimatsu Construction research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Let your next smart move start now. Don’t just stay on the sidelines when you could be uncovering tomorrow’s winning stocks using these powerful SWS tools:

- Spot companies generating strong yields and take action with these 16 dividend stocks with yields > 3% to boost your income strategy.

- Jump on the AI revolution and position yourself for what’s next with these 26 AI penny stocks which are already shaping the future.

- Secure potential bargains and act before the crowd with these 916 undervalued stocks based on cash flows based on high conviction cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nishimatsu Construction might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1820

Nishimatsu Construction

Engages in the construction, development, real estate, and other businesses in Japan and internationally.

Average dividend payer and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor