Advertisement

- Japan

- /

- Construction

- /

- TSE:1812

Kajima (TSE:1812): Assessing Valuation Following Major Offshore Wind Contract Win

Simply Wall St

Reviewed by Simply Wall St

Kajima (TSE:1812) has landed a major contract to provide foundation work for a 315-megawatt offshore wind project in Japan. This marks a milestone in the company’s efforts to expand its renewable energy portfolio.

See our latest analysis for Kajima.

This fresh contract appears to have energized sentiment around Kajima, with the share price climbing 13.8% over the past month and an impressive 37.8% in the last 90 days. Momentum has continued to build throughout the year, pushing Kajima’s year-to-date share price return to nearly 77%. The total shareholder return over the past year sits at a remarkable 101%. This surge highlights renewed investor confidence as Kajima cements its standing in the renewable energy arena.

If you’re interested in surfacing more opportunities like this, consider seeing what’s ahead for the sector with our fast growing stocks with high insider ownership

With shares on a tear and optimism high after the latest contract win, the question now is whether Kajima’s valuation still offers upside for investors or if the market is already pricing in future growth.

Price-to-Earnings of 17.5x: Is it justified?

Kajima is currently trading at a price-to-earnings (P/E) ratio of 17.5x, putting it above both the Japan Construction industry average of 12.6x and its peer average of 17x. At its last close price of ¥5,063, the stock’s multiple implies a premium is being paid for its growth or stability.

The P/E ratio compares a company’s share price to its per-share earnings, helping investors gauge whether the market has high expectations for future profit growth. For established construction firms like Kajima, a higher P/E can signal strong earnings momentum, operational consistency or market confidence in future project pipelines.

This premium valuation is notable, especially since Kajima’s earnings growth outpaced the industry last year, while revenue growth expectations remain modest. However, when measured against our estimated fair price-to-earnings ratio of 19.8x, Kajima’s current valuation still offers some headroom for re-rating if its performance continues to impress.

Explore the SWS fair ratio for Kajima

Result: Price-to-Earnings of 17.5x (OVERVALUED)

However, ongoing reliance on project wins and modest revenue growth may challenge Kajima’s ability to sustain its premium valuation in the future.

Find out about the key risks to this Kajima narrative.

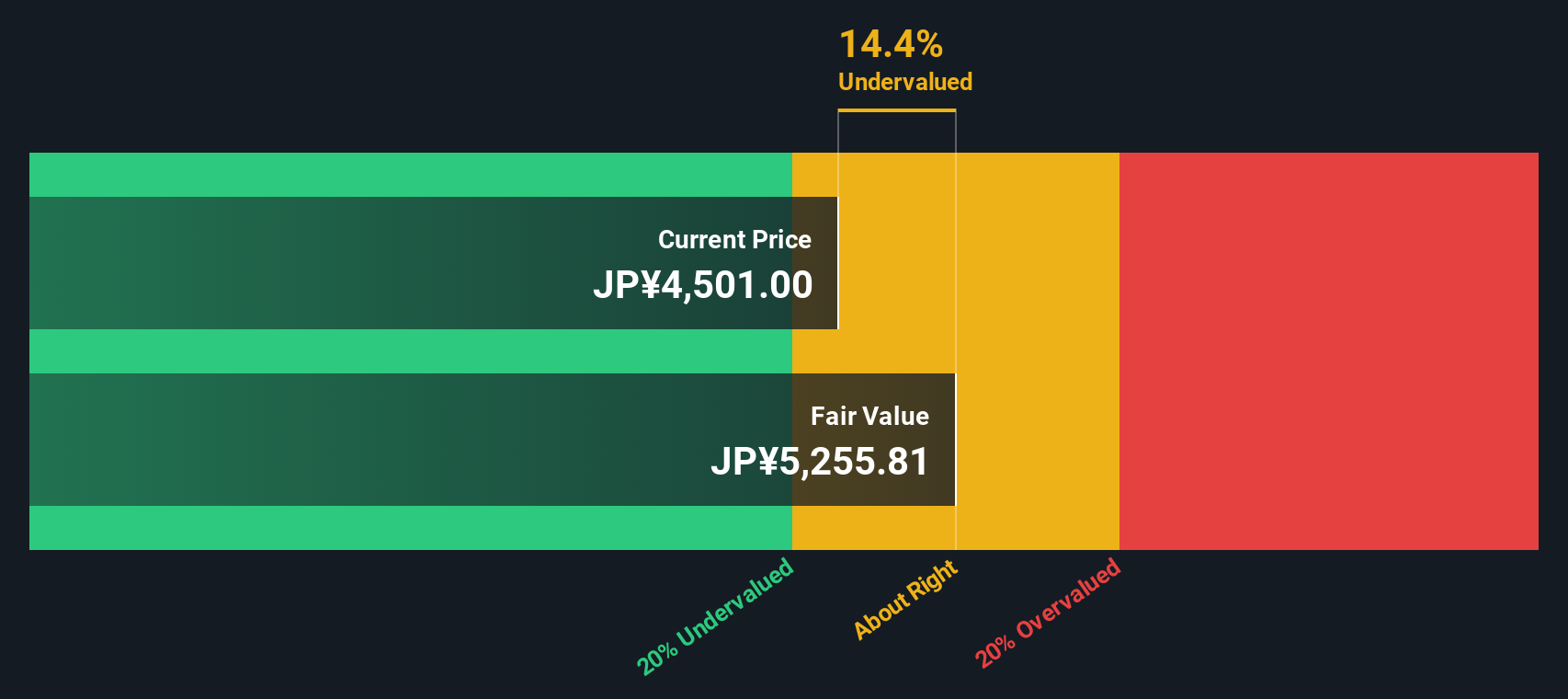

Another View: SWS DCF Model Suggests Undervaluation

A different valuation method, the SWS DCF model, paints a somewhat more optimistic picture. According to this approach, Kajima shares are trading about 4.6% below their calculated fair value. This suggests the stock may be undervalued despite its recent run. Can this possibility of further upside be trusted, or is the market’s optimism already reflected in the price?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kajima for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Kajima Narrative

If you’d rather dig into the numbers yourself and reach your own conclusions, it’s quick and simple to build a custom narrative in just minutes. Do it your way

A great starting point for your Kajima research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors move fast when opportunity knocks. Use the Simply Wall St Screener to spot tomorrow’s potential winners and keep your portfolio a step ahead.

- Capture rapid growth and volatility potential by checking out these 3556 penny stocks with strong financials with strong financial health and room to run.

- Position yourself at the center of healthcare innovation with these 33 healthcare AI stocks which is shaping advances in diagnostics, patient care, and medical data analytics.

- Seize steady returns and compound your wealth through these 17 dividend stocks with yields > 3% that offer attractive yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kajima might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1812

Kajima

Engages in civil engineering, building construction, real estate development, architectural and civil design, and other businesses.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor