Advertisement

Keiyo Bank (TSE:8544): Assessing Valuation After Dividend Hike and Share Buyback Announcement

Simply Wall St

Reviewed by Simply Wall St

Keiyo Bank (TSE:8544) held a board meeting on November 10 to approve a share buyback and boost its dividend forecast. Investors are watching these moves as signals of management’s confidence in the bank’s outlook.

See our latest analysis for Keiyo Bank.

Keiyo Bank’s recent rally has grabbed attention, with the share price up 13.7% over the past month and 82.2% year-to-date. Momentum has clearly accelerated as the bank’s strong financial results and shareholder-focused moves, such as a higher dividend and planned buyback, have fueled renewed optimism. This is underscored by an impressive 89.3% total shareholder return over the past year. Long-term investors have also seen standout gains, with the three- and five-year total returns reaching 216% and 259% respectively.

If Keiyo Bank’s bold moves have you interested in what else is out there, now’s the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With shares rallying and management making bold moves, the key question is whether Keiyo Bank remains undervalued or if the recent surge means the market has already priced in all the future growth potential.

Price-to-Earnings of 12.7x: Is it justified?

Keiyo Bank’s shares are currently trading at a Price-to-Earnings (P/E) ratio of 12.7x, which is above both the Japanese banks industry average of 11.3x and the peer group average of 11.1x. This suggests that the market is pricing in stronger growth or profitability than peers, despite the recent rally.

The P/E ratio measures how much investors are willing to pay for each yen of the bank’s earnings. In banking, it is a common yardstick as it captures profitability against peers and sector expectations.

Paying a premium often signals confidence in future results. However, with earnings growth of 3.9% over the past year, which is below both its own five-year average and the industry’s performance, the higher multiple appears optimistic. Since there is insufficient data to calculate Keiyo Bank’s fair P/E ratio, there is uncertainty about whether this valuation will hold or adjust.

Compared to its industry, Keiyo Bank appears expensive based on commonly tracked earnings multiples, and its premium may not be completely justified by recent profit trends. With no fair multiple available as a guide, investors face uncertainty about how long this premium might last in a competitive market.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 12.7x (OVERVALUED)

However, factors like shifts in investor sentiment or weaker profit trends could quickly challenge the current valuation premium at Keiyo Bank.

Find out about the key risks to this Keiyo Bank narrative.

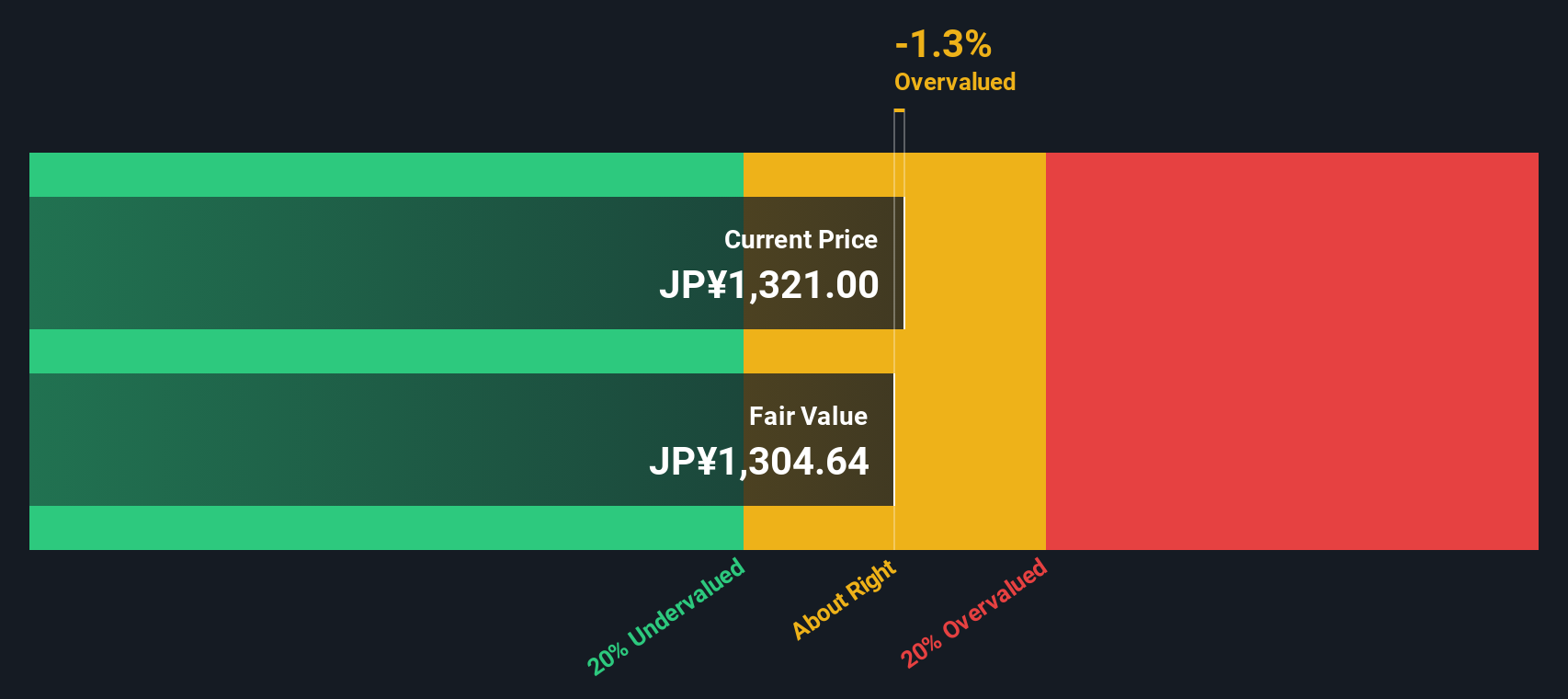

Another View: What Does Our DCF Model Say?

Taking a different approach, our DCF model estimates Keiyo Bank's fair value at ¥1,397.79 per share. The stock currently trades above this level at ¥1,430, which suggests shares may be modestly overvalued based on projected cash flows. Does this mean recent optimism is running ahead of fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Keiyo Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 878 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Keiyo Bank Narrative

If you have a different perspective or want to dig deeper into the numbers yourself, you can shape your own take in just a few minutes, and Do it your way.

A great starting point for your Keiyo Bank research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Be one step ahead by expanding your strategy and tapping into handpicked opportunities across sectors with the Simply Wall Street Screener to gain an investing edge.

- Maximize your portfolio’s growth potential by targeting undervalued companies. Scan these 878 undervalued stocks based on cash flows with strong underlying fundamentals and upside that the market may be missing.

- Enhance your returns with robust income streams by focusing on reliable payers. Use these 16 dividend stocks with yields > 3% to pinpoint stocks with attractive yields exceeding 3%.

- Explore innovation at its earliest stages by identifying promising ventures among these 3593 penny stocks with strong financials, offering bold opportunities with solid financial credentials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keiyo Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8544

Keiyo Bank

Offers various banking products and services to individual, corporate, and business customers in Japan.

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor